The top news on Tuesday was Yellen’s speech delivered to the National Association for Business Economics in Cleveland. The topic of conversation was how badly the Fed has miscalculated inflation. It’s surprising to see this coming up so soon after the Fed’s decision on rates because the Fed was hawkish and this was a dovish speech. At the same time, it’s also surprising that it took so long for the Fed to realize it made a mistake. The reason it took so long is because it’s a closely held belief among Fed officials that low unemployment means inflation is coming. They couldn’t change a belief like this until there was unrelenting evidence to go against it. The Fed saved face by admitting they were wrong after a better than expected inflation report.

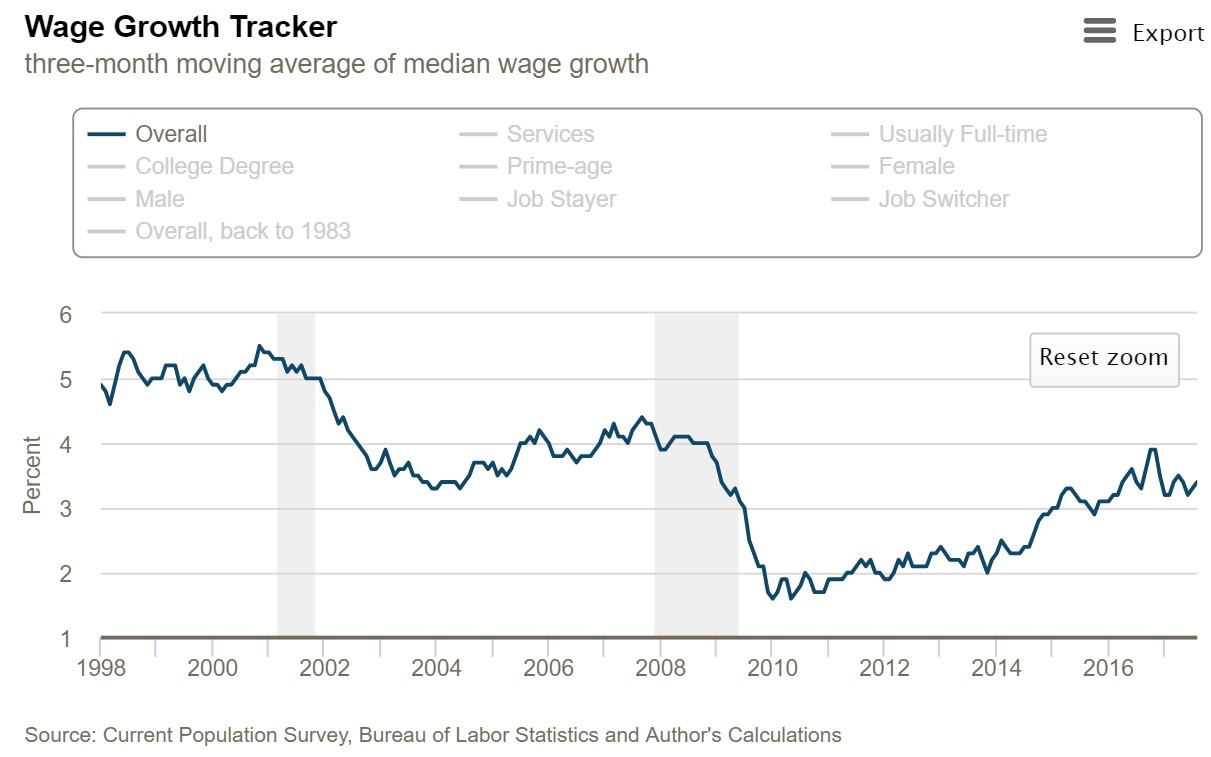

Specifically, Yellen said: "My colleagues and I may have misjudged the strength of the labor market, the degree to which longer-run inflation expectations are consistent with our inflation objective, or even the fundamental forces driving inflation." The chart below is what Yellen is referring to. As you can see, after hitting 3.9% at the end of last year, the wage growth has fallen, stagnating in the mid 3% range. That’s about 1% lower than the last cycle peak which was about 1% below the previous cycle. At this pace, the next cycle might only see 2% wage growth. It’s important to see that the Fed’s miscalculation is massive because they don’t understand why there hasn’t been higher wage growth or inflation in the past 15 years.

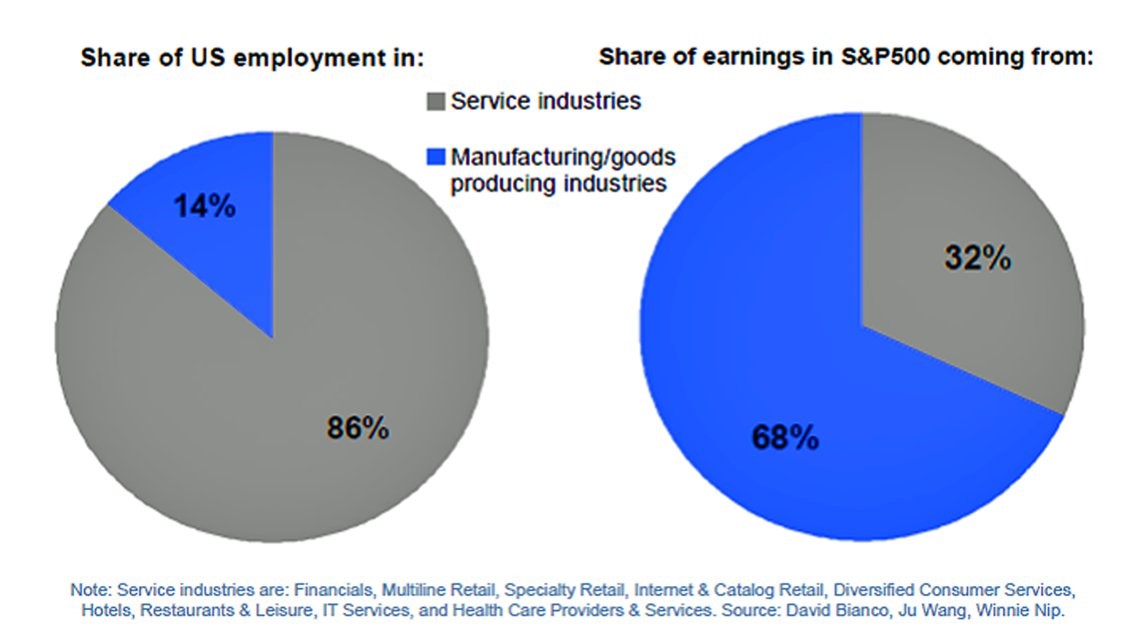

The key point the Fed missed out on in the past 15 years is the influx of workers from Asia and eastern Europe. This caused labor to be outsourced, lowering wages for developed world workers. This demographic trend caused an increase in income inequality in America, but decreased inequality between America and the emerging markets. The chart below shows the hollowing out of the American labor force as the service industries now employ 86% of workers. This is while the manufacturing firms still make a majority of the profits. The trend of the workforce increasing appears to be stabilizing, but the next trend that needs to be weighed is robots taking jobs from Americans.

Robots taking jobs is the trend over the next 20 years that will affect interest rates, inflation, and wage growth. If the population effect is removed then wages for millennials will increase as the baby boom finally retires. If wage growth accelerates in the next 10 years, there will be a big surge in private fixed investment which will push towards robotics. That will eventually decrease the number of workers in the service sector. These are the puts and takes involved in the labor force. It’s just like when the government raised the minimum wage, the restaurant companies replaced them with computers allowing you to order with a touch screen.

The question which needs to be asked is if the corporations will ever accept declining margins again. The emerging market workers subsidized businesses for the past 2 decades. Now that businesses can take the labor situation into their own hands, they may make huge investments so they don’t need to employ more workers. The ironic part of the situation in the past few months is that the manufacturing sector is seeing a labor shortage as many firms say they can’t fine entry level employees.

The takeaway from Yellen’s speech is that the Fed may start to be more gradual with its rate hikes and possibly slow the balance sheet unwind. It’s amazing to see Yellen step back from the last hawkish statements so quickly. You’d think she’d only step back from her hawkishness if the market fell in response to the unwind. It hasn’t even started yet. I might be overanalyzing this. She might be talking about the economic theory about why the Fed was wrong opposed to applying it to current policy or 2018 policy. Usually I look at Yellen’s comments in the context of the chances of future rate hikes, but rate hike odds in 2018 are immaterial. Now what’s more important is how Yellen’s comments and various media reports effect the Fed chair pick in February 2018. The pick could change the odds for rate hikes in 2018 and beyond immediately.

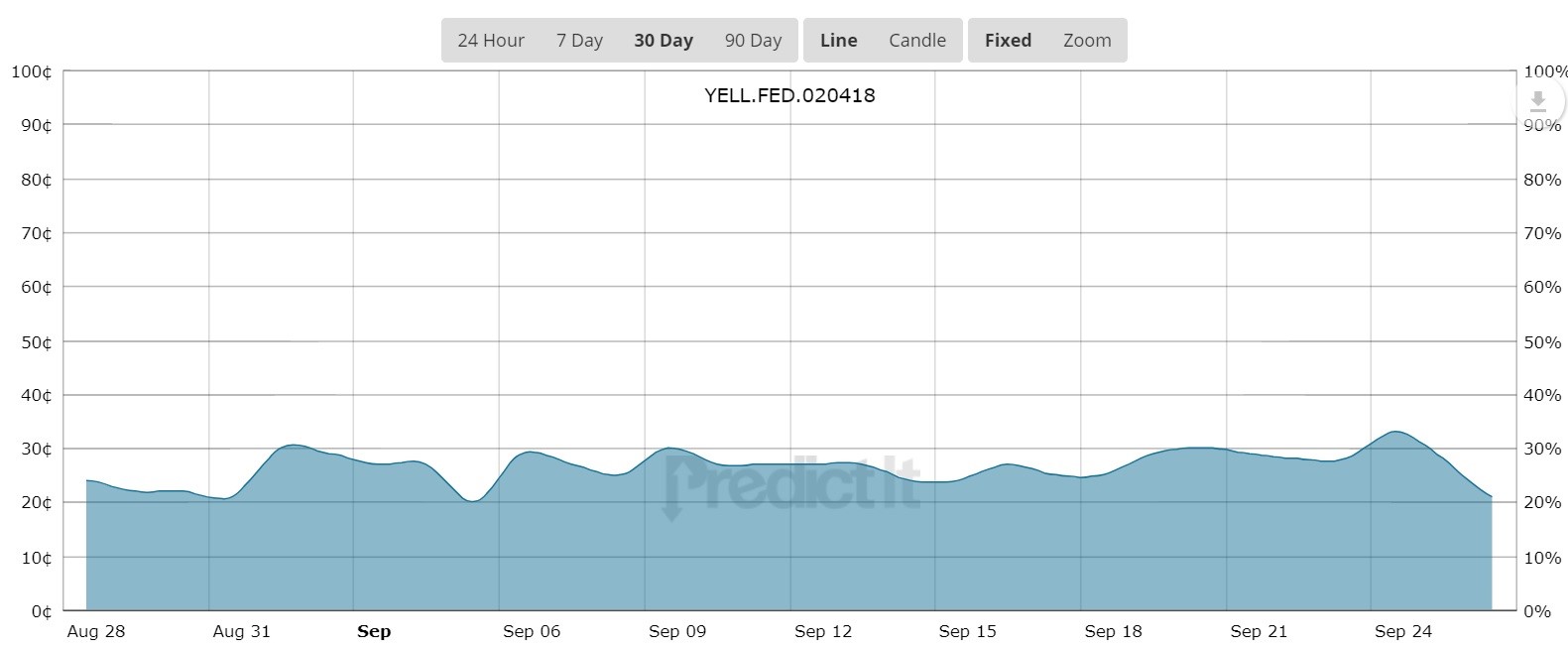

The chart below shows Yellen’s chances have fallen to 21% and Warsh’s chances increased to 40%. I’ve been on the Warsh bandwagon for the past few weeks. The pick will likely be made in the next 6 weeks, so these odds are becoming more important. Yellen’s dovishness doesn’t matter if Warsh is picked since he disagrees with her on most topics. Since 3 rate hikes have been floated in 2018, I don’t think Warsh will hike much more than that since inflation is so low, but the key difference is I expect the unwind to be accelerated and elongated. Warsh won’t want a $2.5 trillion balance sheet in perpetuity. He’ll want the balance sheet cut down to what it was before the 2008 financial crisis which was below $1 trillion.

The final point Yellen made was she said, "sustained low inflation such as this is undesirable because, among other things, it generally leads to low settings of the federal funds rate in normal times, thereby providing less scope to ease monetary policy to fight recessions." I disagree with this point because the Fed can cut interest rates below zero and do QE. There’s no reason to force rates higher and cause a recession just to get them higher so they can be cut again. That being said, I think rates should be at 2.75% which is what the Taylor Rule suggests. Rates at 2.75% would be lower than the last cycle peak, but still leave the Fed room to cut. The point is that if Yellen is worried about not being able to cut rates during the next recession, she should put the Fed funds rate closer to what the economy could take. 1% is much lower than necessary. 1% only makes sense if she expects inflation to fall further; that would be different from the recent reports.