Dallas Fed Shows The Impact From Harvey

Let’s look at some of the other points from the Dallas Fed survey to get a complete look at what’s happening in Texas after hurricane Harvey. A transportation equipment manufacturing firm said “Fortunately, we only had minor issues due to Hurricane Harvey, and those were mostly related to some employees not being able to make it in to work as the floodwaters receded. We did experience some material delays due to shipping issues. We also narrowly avoided a major component issue as one of our key suppliers was right in the path of Hurricane Irma. They also only had minor issues and were able to get product out to us shortly after the storm passed. Our expectation that tax receipts would begin to increase and flow through to us as new orders is coming to fruition slightly earlier than we anticipated—thus, the improved outlook for this month over last and for the foreseeable future.”

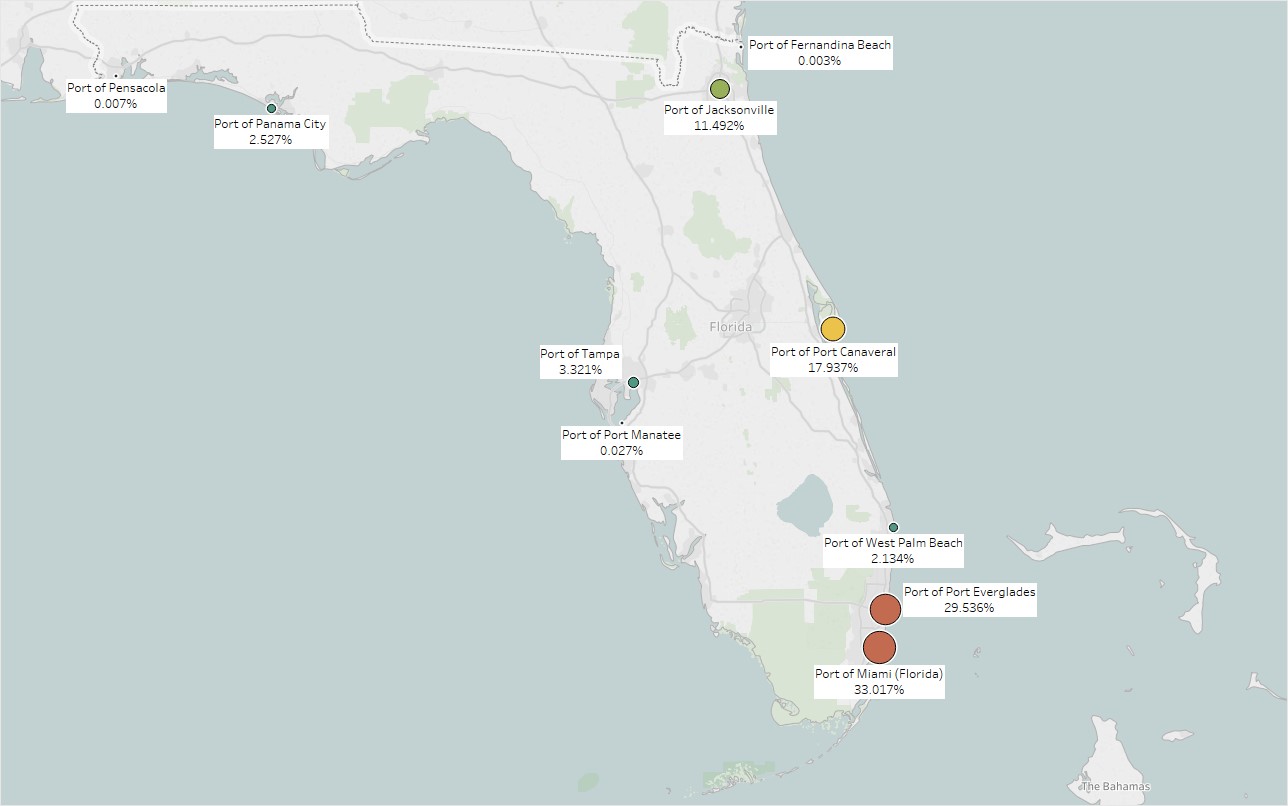

Hurricane Irma impacted the ports in Florida. The map below labels the percentage each port represents in shipping traffic. 151 companies in the S&P 500 receive shipments from one of these top 10 ports in Florida. Miami, Everglades, and Canaveral were closed from September 9th to the 12th. This firm was lucky to narrowly avoid a component issue, but many firms may not have been so lucky. The good news is new orders after the storm came quicker than expected.

There were special survey results because of hurricane Harvey that we’ll look at now. 77% of gulf coast firms said they were negatively impacted and 31% of the rest of Texas firms said they were negatively impacted. Only 16% of gulf coast firms said there will be a significant decrease in revenue and production in the next 6 months; 8% of all firms in Texas said this. 10% of all Texas firms said it would be significantly more difficult to hire workers in the next 6 months because of Harvey. As we’ve discussed, raw material prices were boosted because of scarcity and demand and wage inflation is coming to certain sectors like manufacturing and construction because of the increased demand for workers. The worst case scenario is that businesses simply can’t find any workers to do the jobs. That’s an issue that could affect more sectors as the labor market gets tighter. It negatively effects the capacity to utilization rate.

The overall biggest issues were disruptions to personnel, transportation and supply chain issues, and loss of the customer base. The average number of days all firms were shut down was 3.9. The average number of days gulf coast firms were shut down was 6.1. The manufacturing firm that was shut down 7 days that we discussed previously must’ve been from the gulf coast. When asked about how much of the losses were covered by insurance, 68% said the physical capital losses weren’t covered and 81% said revenue and production losses weren’t covered. That makes sense because a lot of areas that were hard hit weren’t flood zones. This hurricane wasn’t anticipated to flood the areas it flooded.

Leading Index Shows 1H 2018 Weakness Possible

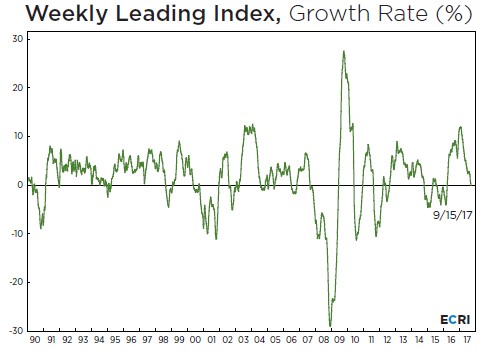

In other economic news, the weekly leading index put out by ECRI fell to 0%. That is a 78 week low in growth. This weakness coordinates with the credit pulse which is showing signs of weakness. There’s nothing close to indicating a recession, but I think there will be some economic weakness in Q1 of next year. The indicator correctly showed in advance that Q2 2017 GDP growth would be one of the fastest in this economic recovery. Part of this chart is reflective of base effects. That’s why the growth rate fell sharply in 2010, rebounded in 2011, fell in 2012, and rebounded in 2013. The late 2016/early 2017 strength came from lapping the weakness in 2015. Now the next bout of weakness will come from the 2017 strength. The key is to determine if the slowdown in rate of change terms will lead to another recession. There’s nothing that tells me there will be a recession in the next 6 months.

Tax Reform Coming?

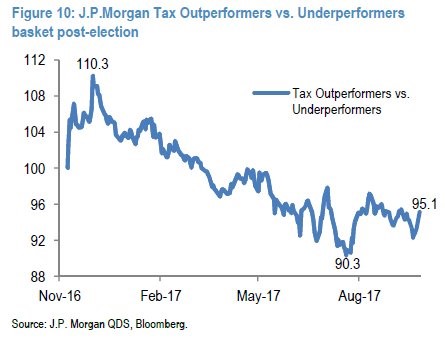

The chart below shows the amount of optimism for tax reform being passed by comparing the firms that would do better because of tax reforms with those that would do worse. As you can see, the index had an initial pop after the election, but fell into a downtrend as week after week passed without anything getting done. It’s interesting to see that the index bottomed in late July. That’s probably because the failure of the healthcare bill by one vote being changed at the last minute was the worst it could get. Congress challenged that bottom by failing again in September. That might be why the index fell in September and bounced back. As this point, few think healthcare reform will pass in the next few months. The quicker the Congress fails, the faster it can get on with tax reform which should also be messy, but get closer to passing at the least.

Apple - AAPL

On Monday, I said to buy AAPL because it could have a few percentage points rebound after investors start to realize that weak preorders from the iPhone 8 isn’t a death knell for this cycle’s sales. The stock rebounded 1.72% because of these hopes on Tuesday. I think the stock can get to $160 before the iPhone X release in November. At that point whether you hold it depends on if you think the iPhone X will be a success. I’m not confident enough to say it will be a success, but I think it won’t disappoint as badly as the iPhone 8.

AAPL was able to push the S&P 500 and the Nasdaq positive, but the Dow was down for the 4th straight day. The Russell 2000 has continued its rampage higher as it was up 0.34% reaching a new record high. It’s up 7.37% since August 21st. It’s tough to say for sure why the small caps are rallying, but one possibility is they had underperformed for too long. The other point, which I made earlier is that the financials are carrying it higher, spurred by a hawkish Fed.