More information is coming out on how hurricane Harvey effected the economy. The chart below shows how retail sales ex-autos were affected by the storm. As you can see, there was a boost in sales in Texas prior to the storm because people were buying supplies such as necessities as well as storm protection gear. Then when the hurricane hit, retail sales plummeted about 30% for two days before starting to recover. It’s surprising to see how quick the recovery was given the fact that the storm lingered for a few days. There may have been a dip in sales in Louisiana afterward as that was Harvey’s next target. This chart gives us a quick summary of how long the storm effected the Texas economy. Some of the increased spending to cleanup hurricane Harvey’s damage and replenish supplies will be mixed with the weakness which came from Irma in early September. To make matters worse, there’s another hurricane in the Caribbean named Maria which will impact Puerto Rico soon and possibly America next week.

harveyretail CHART

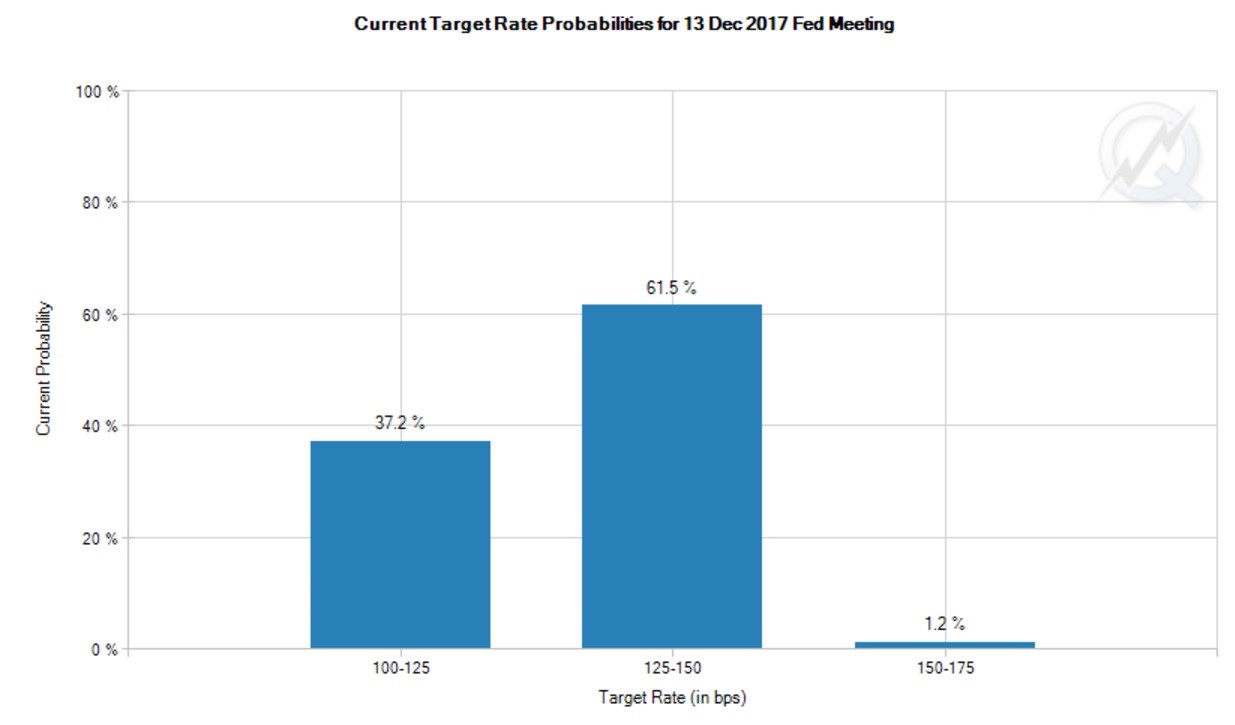

Hurricane Harvey impacted most of the economic data. The increased demand could have pushed inflation slightly higher. That’s why I’m shocked that one better than expected CPI report could push rate hike expectations so much higher. As you can see, now there is a 62.7% chance of a rate hike. We are very close to the 70% threshold necessary for a hike. That’s a big switch as we were near 40% a few days ago. The possibility I discussed last week where hurricanes boosting inflation slightly could catalyze a rate hike in December, looks more likely to occur. It’s weird that the market ignores any weakness caused by the hurricane, such as in the jobless claims, yet it changes rate expectations even though the hurricanes could be impacting the inflation data. It’s a very positive sign that the equity market is rallying even with one more rate hike this year being baked in. It’s probably not a huge factor one way or the other. I still think if a hawk was appointed as Fed chair there will be a sharp draw down in response.

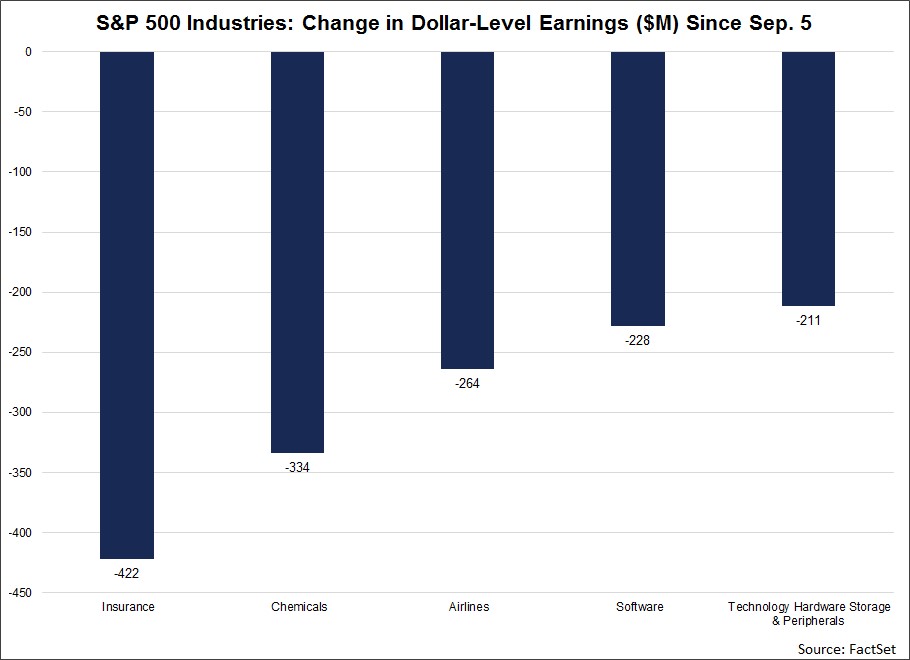

FactSet decided to look at the industry level effect of the hurricanes because S&P 500 estimated year over year earnings growth for Q3 has fallen from 5.1% to 4.5%. There has been a $1.6 billion decline in Q3 expected earnings. The chart below highlights the industries with the largest declines since September 5th. It’s notable how insurance companies, chemicals, and airlines were the sectors which were impacted by the storms. Progressive had a 35.2% decline in mean EPS expectations for Q3 and Travelers saw a 32.4% decline. Travelers was part of the hurricane trade I mentioned which was to short Travelers and go long Home Depot. The chemicals industry impact was mainly because of DuPont which was effected by Harvey. It had its mean EPS fall 22%. The $264 million impact the airlines felt was caused by increases in cancellations and fuel prices. This picture FactSet paints is incomplete because it doesn’t discuss some of the firms which may have benefited from the storm such as Home Depot. That’s not to say I don’t think the storm had a negative impact on Q3 S&P 500 earnings, but I think some of the declines may have been mitigated.

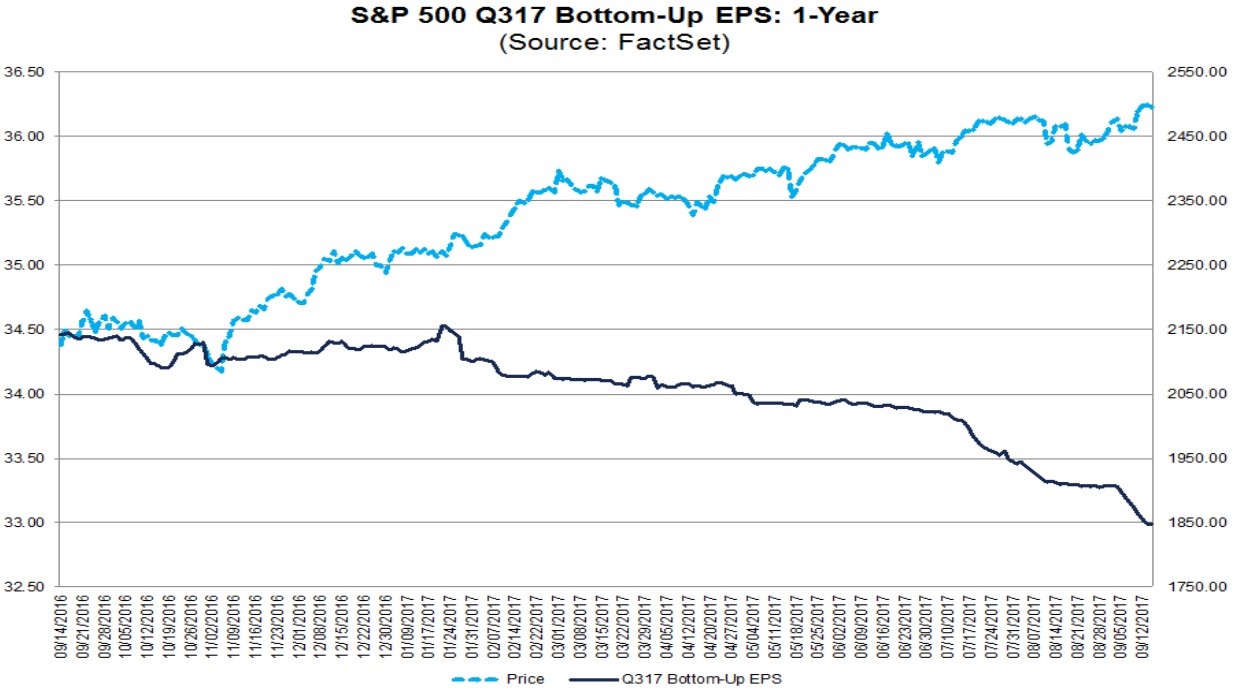

As I mentioned, there continues to be a sharp decline in Q3 earnings estimates while stocks continue to reach record highs. That’s been a common trend this bull market, but it was reversed in Q1 and Q2. The chart below shows the sharp change in expectations. Either earnings estimates will be beat by a large margin because the bar has been lowered or this will be the worst quarter of the year despite the tailwind of the weak dollar. One interplay I have been watching is the relationship between the 2017 earnings expectations and the Q3 earnings expectations. 2017 expectations are still above the troughs of April and July. The reason why the 2017 estimates haven’t dropped below those troughs is because Q3 is looking like a one-time event according to the estimates. I can’t tell why Q3 will be especially bad while the next few quarters are projected to be great again. It has been a steady decline in estimates. The hurricane impact doesn’t help, but it’s not the main reason for the dip.

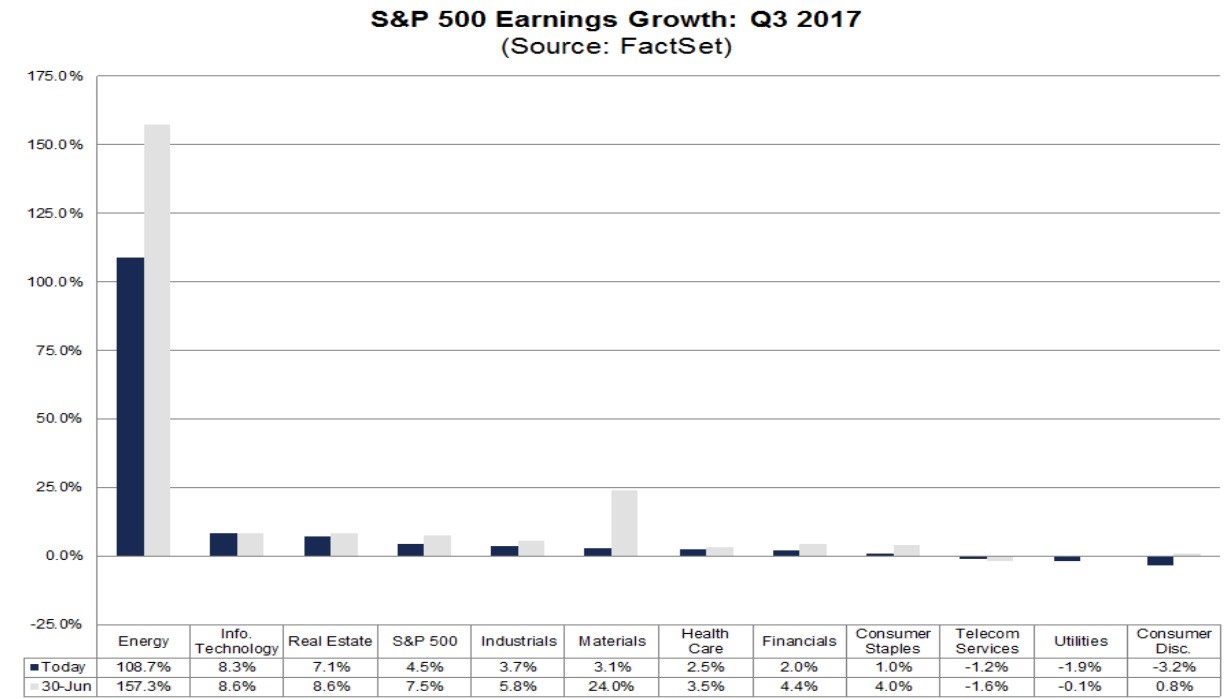

The chart below reviews the changes to Q3 estimates since June 30th. As you can see, every single sector has had a drop in earnings estimates except telecom. The two most important questions which will answered when most earnings start to be reported in a few weeks are what the catalyst was for this quarter being so weak and why/if earnings growth will improve in Q4. Earnings growth is expected to be 11.2% in Q4 and double digits for the next two quarters after that even though there will be very tough results being lapped in the first half of 2018. Because Q3 and Q4 are the only quarters left in the year to be reported, the 2017 estimates can be used to extrapolate how Q4 is shaping up since June 30th. Financials, technology, industrials, real estate, health care, utilities, and telecom have seen estimates improve which shows optimism is growing for Q4. The financials could be helped by hawkishness from the Fed, though the impact of a December rate hike will be felt more so in Q1 than Q4

Conclusion

The effect of retail sales from hurricane Harvey is a snapshot of the Texas economy in late August. This doesn’t mean there weren’t other parts of the Texas economy which were hurt for longer. The retail sales impact also helps us understand how Irma may have impacted Florida’s economy. The hurricane’s impact will definitely be short lived for most people and businesses, but what may not be short lived is the weakness in earnings. Q3 guidance will tell us if first half earnings were a mirage or if Q3 is going to be a one-off event. If Q3 guidance causes Q4 estimates to fall, stocks will correct. Stocks are at their record highs because investors don’t anticipate that happening