European Junk Bonds Are Expensive

There is a noticeable difference between the European high yield debt market and U.S. treasuries. High yield debt no longer has a high yield in Europe and America as European junk bond yields are close to the AAA rated U.S. debt. That’s because of relentless ECB corporate bond buying which has made it the central bank with the largest balance sheet. Barclays did an analysis of European junk debt versus American junk debt which you can see in the chart below. As you can see, the Pan European high yield market ex-financials has a historically high yield compared to the U.S. high yield market ex-financials. That difference is partially because of the difference in the ratings breakdown between the two markets. The U.S. has more CCC rated bonds which are the worst rated bonds and less BB rated bonds which are the best rated junk bonds. The low rated U.S. bonds are mainly in the energy sector. That ratings difference means you’d expect U.S. bonds to have higher yields. However, adjusting for that, there is still a 12 basis point spread between the two markets. That is in the 60th percentile looking back at the past 2-3 years of data. As you’d expect, while the ECB bond buying program pushes junk bond yields lower, the liquidity of the capital markets means some of the money flows to U.S. to get the arbitrage between the two markets. That’s why the difference isn’t more substantial.

The difference between the European junk debt market and the U.S. treasury market is still historically low because the difference between the American junk bond market and treasuries is low. It’s also worth noting that the chart I used in a previous article comparing European junk to treasuries only looked at BB rated bonds, so it adjusted for the fact that Europe has 67% of its junk bonds rated BB. Central bank bond buying is suppressing yields across the board, making it tough to determine how expensive assets are relatively speaking. If you’re looking for more yield than treasuries, buying U.S. junk debt makes sense over European junk debt. I would argue you’re picking up dimes in front of an oncoming train because when default risks rise, you will be in a lot of pain. I don’t think default rates will rise in the next few months, yet I still find the risk tough to stomach. It’s a matter of risk tolerance and capital allocation.

The point here is explaining why certain assets are priced the way they are. There’s almost always an explanation for why something is valued the way it is. Don’t confuse an explanation for a defense. For example, Apple is valued at over $800 billion because of certain sales projections for the new phones. The consensus is made up of intelligent analysts, but it can still be wrong if there’s production delays or software bugs which ruin the customers’ experience.

The Fed’s Response To Hurricanes

Investors and economists are interested to hear what the Fed says at its September 20th FOMC meeting. Specifically, it will be notable what the Fed says about the economy in relation to the hurricane related effects. We are just getting information about how the economy was effected by hurricane Harvey. By September 20th, the Fed will have more data to work with. We probably won’t know the effects of hurricane Irma by then because it’s still ongoing this week.

We got a glimpse of what the Fed will say in response to the hurricanes when NY Fed President Bill Dudley spoke with Steve Liesman. He said the hurricanes are a short run negative, but a long run positive for the economy. He also said the hurricanes will make it difficult to look at what the economic data would have been without the storms. This implies to me the Fed won’t be making any policy changes at the meeting. The Fed will go along with the plan to start the unwind of the balance sheet in October. The Fed is lucky the September meeting isn’t the last chance to raise rates by the end of the year. There still appears to be some rhetoric that one more hike will occur this year. By the December, meeting the hurricane effects will be gone. I still don’t think there will be a rate hike, but at least the situation will be clear.

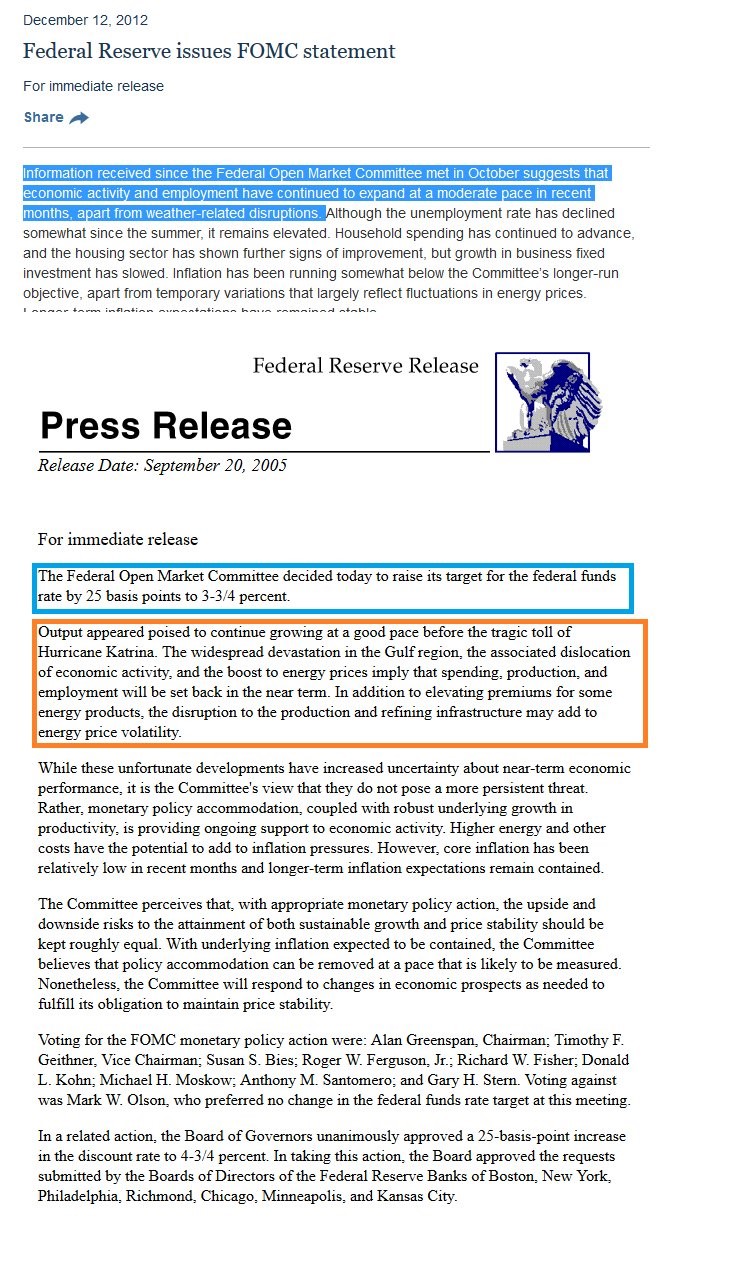

The image below is a screenshot from the prior two Fed statements after hurricanes hit. The December 2012 meeting was after hurricane Sandy which impacted the NYC tri-state area with intense flooding in late October and early November. As you can see, the Fed called it weather related disruptions. The key word in the September 2017 meeting will be that the hurricanes’ effect on the economy will be “transitory.” In September 2005, the Fed raised rates despite hurricane Katrina because the Committee said “it does not pose a more persistent threat.” In that case, raising the Fed funds rate wasn’t a big deal because of hurricane Katrina. It was a big deal because it helped lead to the collapse of the housing bubble.

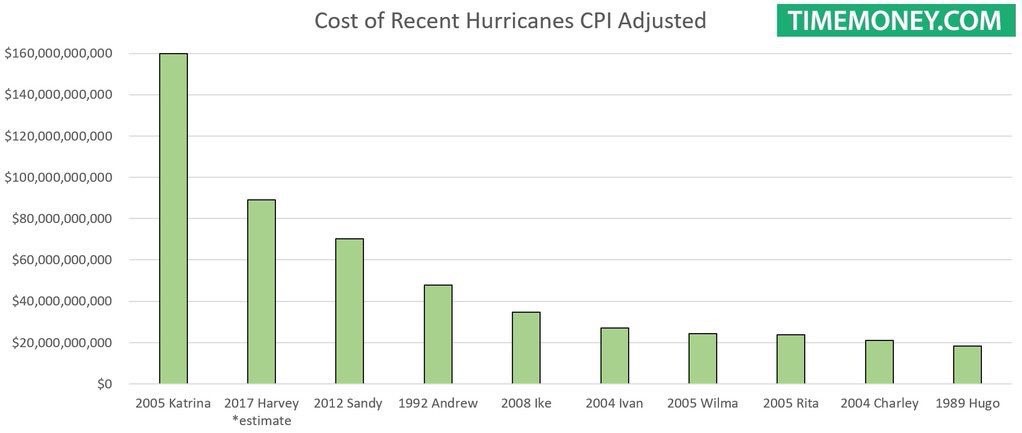

As you can see from the chart below, hurricane Harvey was likely costlier than Sandy, but less costly than Katrina. However, when you add in the cost of hurricane Irma, it could be worse than Katrina. That effect will cause the Q3 GDP growth rate to take a decent cut, but it probably won’t affect monetary policy. To get an idea of what the GDP effect will be, Goldman estimates hurricane Harvey will take 0.8% off GDP growth. The growth rate excluding the hurricanes probably would have been between 2.5% and 3%, so taking it down 0.8% brings us to 1.7% to 2.2%. Then if you add in the effect Irma had, it means the GDP growth will be below 2%. On the bright side, Q4 will get a boost from the rebuilding efforts.