Debt Ceiling Issue Over For The Time Being

There was yet another twist in the debt ceiling debate as President Trump’s meeting with Nancy Pelosi and Chuck Schumer has led to an additional agreement. President Trump wants to eliminate the debt ceiling completely. This has been a talking point the progressives have used for years so it’s not surprising to see the Democratic leadership agree to this deal. In the short term, this helps the President and the GOP because they won’t need help from the minority party to get the ceiling raised, but in the long term it helps the progressives because the fiscal conservatives always try to attach spending cuts to agreements to raise the ceiling. While different deals are made where anything can be attached to it, it’s easier to get spending cuts done because the debt ceiling shows how much the country’s fiscal house is out of order. The December vote to get rid of the debt ceiling will depend on how many fiscal conservatives balk at the idea.

In terms of the current debt ceiling debate, the Senate passed the increase and Harvey relief on Thursday, so it will be up to the House to pass it to send it to the President’s desk. The way the vote turns out will give us an inside look into how the ending of the ceiling vote will go in December. The Republican Study Committee, which has 155 members, opposes the deal. My expectation is this plan will pass because of Democratic support, but the one in December won’t because even more Republicans will oppose it because they want to rein in spending.

Looking at the issue from the stock market’s perspective, this is great news because the chance of the debt rating being cut has been almost eliminated this month. It would prevent future worries if the ceiling was eliminated. The dollar will be hurt by this issue because the risk off trade is no longer on the table and because the U.S. spending without constraint ruins the long term fiscal health of the government. The dollar is now at a 32 month low as my prediction that the dollar would plummet this year has worked out. This will provide a big tailwind to Q3 earnings.

Apple About To Be In ‘Sell The News’ Mode

Even with the positive news about the debt ceiling, the stock market was down on Thursday. Besides some weaker than expected economic data, the market was held back by Apple which was down 0.40%. There was negative news about production delays for the new iPhone which is expected to go on sales on September 22nd. I think the bigger reason for the selloff is because the hype surrounding the new iPhone is fading as the ‘buy the rumor, sell the news’ trade is in full effect. Unless there’s an unlikely shock in the announcement of the new iPhone on September 12th, I expect a modest pullback in the stock in the next few days. This could hamper the overall market.

Economic Weakness & Yield Curve Flattening

Another trend to watch out for besides the dollar weakness is the yield curve flattening. With some recent weakness in the economic reports, the yield curve has begun to flatten quickly. We are now approaching the level seen in 2016 as the difference between the 10 year yield and the 2 year yield is 77.67 basis points. The financials are still holding up relatively well to the S&P 500, but that should change if the 2016 levels are broke. I look at the yield curve as a timer for when the next recession will occur. If the bottom falls out after the 2016 level is breached, we could be looking at a recession in 2-3 years.

Some of the recent economic reports have been softening right before the blackout period in the data where it will start to look erratic thanks to hurricane Harvey. Some of the strong weakness in the reports may actually partially reflect real economic weakness. The chart below shows the weekly leading index which has a growth rate of 1.9%. This a 73-week low. I wouldn’t panic from this report and start to think the economy is about to falter because it’s still positive which wasn’t the case during 2015 and 2016. The forecast was accurate in predicting strong Q2 GDP growth. The slowdown implies a deceleration in Q3 which is also looking like a correct prediction. It will be important to check this indicator in the next few weeks, to see if another slow economic period is coming.

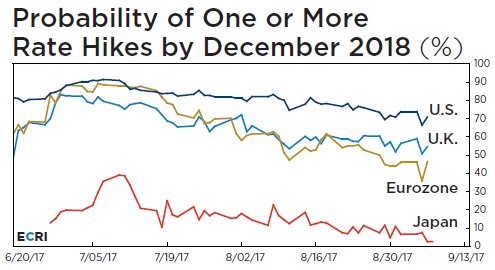

No Rate Hikes Anywhere

For much of the year, we’ve been discussing the possibility of 2018 being the start of a slowdown in global QE. The chart below shows in the past few weeks the odds of rate hikes by December 2018 have been declining globally. In the U.S.’s case the reason for the lack of rate hikes stems of the disinflation and because of the balance sheet unwind which is starting in a few weeks. At first, Fed officials said there would be a pause in rate hikes because of the unwind, but it looks like the pause will last longer than a few months. For Europe, you would think there would be more of a propensity to raise rates because its GDP growth rate accelerated to 2.3% and its rates are set at 0%. However, the tapering will probably be larger than the Fed’s unwind, so that cancels it out. The official guidance is for the QE to end in late 2018 to early 2019 and the zero percent interest rate policy to end after that which means there might not even be a rate hike in 2019.

Conclusion

There was a combination of good and bad news on Thursday leading to a flat market. Many economic indicators are coming in soft and the iPhone might be having production problems which could delayed shipments. On the other hand, for the first time in months, the stock market was supported by the government which is about to raise the debt ceiling. Hurricane Irma looks to have catalyzed a bipartisan agreement for once as FEMA support is needed quickly.