Draghi & Yellen Deliver Nothing

Besides Yellen, Mario Draghi, the ECB president, spoke at the Jackson Hole event. There was some intrigue into whether he would give detail on the ECB’s bond buying program, but that will be pushed off into October as he didn’t give any monetary policy updates. The dollar continued to selloff versus the euro after this speech was released. It’s interesting to see the sharp moves in assets when no information on policy that moves markets in the short term was given. Draghi’s speech was another political rant like the one he gave earlier this week and the one Yellen gave. Draghi will be in his position longer than Yellen, making him more important. Let’s look at some of the points he made.

The main theory Draghi pursued is that because the western economies are maturing, they are seeking protectionist policies which hurts growth. He said, “Only higher potential growth can provide a lasting solution. So, clearly, to foster a dynamic global economy we need to resist protectionist urges. But to do so, we also need to identify how best to respond to protectionism." This is a great point. Protectionism in America is being longed for because other countries are more competitive in the manufacturing area. People don’t want to hear that they need to compete harder instead of asking for a government handout which is what tariffs are. Tariffs are a tax on the consumer to provide manufacturing jobs. They hurt growth and slow the global economy. We are seeing the benefits of trade growth this year despite the rhetoric. It’s pushing emerging markets’ stocks higher.

The other point Draghi made was in support of regulations, much like what Yellen spoke about. Essentially, Draghi gave a speech which is the antithesis of Trump’s message which is against free trade and regulations. Draghi said, “When monetary policy is accommodative, lax regulation runs the risk of stoking financial imbalances. By contrast, the stronger regulatory regime that we have now has enabled economies to endure a long period of low interest rates without any significant side-effects on financial stability, which has been crucial for stabilizing demand and inflation worldwide. With monetary policy globally very expansionary, regulators should be wary of rekindling the incentives that led to the crisis.” It’s convenient for Draghi to say low rates mean regulation is needed because I bet if rates were high, he’d say high rates need regulation. Secondly, he tacitly acknowledges that low rates and QE can cause financial bubbles by saying that regulation is especially needed in this environment.

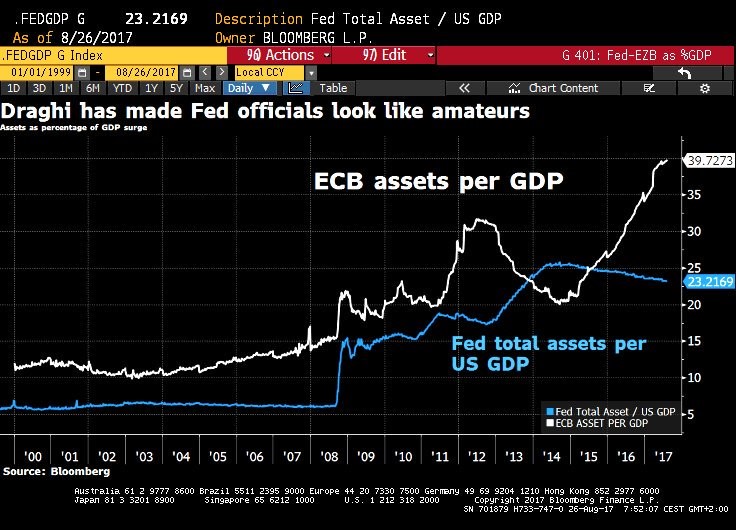

The chart below summarizes why Draghi is more important than Yellen. He will be around longer than her and the ECB’s balance sheet has become massive compared to the Fed’s. The ECB’s balance sheet is near 40% of GDP as the central bank is coming close to running out of assets to buy. It would be ironic to see the ECB asking Greece to issue more debt so the ECB can meet its buying goals since the EU has demanded Greece spend less money. That’s a hypothetical scenario which could happen at the pace the ECB is at. The chart gives us a reminder that when the ECB shrunk its balance sheet, the Fed was doing QE 3. The coming decline in both lines in this chart will have a big effect on financial markets if it happens.

Economic News

On a relatively unusual note, there was a string of mostly negative economic reports which pulled down GDP estimates at the end of this week. The only positive report in the past two days was the Bloomberg Consumer Comfort report which isn’t surprising because the jobs market is solid and stocks are near their all-time highs. The weekly index reached 52.8 which is the highest reading since August 2001. The current economic view index rose to 53.2 which is the best reading since April 2001. The personal finances gauge reached a 10-week high.

I get confused by these surveys because 78% of workers are living paycheck to paycheck and about 40% are living with crushing debt. It’s tough to figure out what this all means since it’s common sense that someone living paycheck to paycheck with debt that isn’t manageable doesn’t seem like someone who would be optimistic about the economy. It’s possible student debt is crushing workers who have good jobs. I shiver at the problems the student debt market will see in the next recession since it’s currently looking awful while the labor market is strong.

The two major weak economic reports this week were the existing home sales report and the durable goods report. There was a big disappointment on the existing home sales front which is consistent with most of the housing reports in the past few months. Existing home sales fell 1.3% which was below expectations for 0.9% growth. Supply was down 9%. That’s the narrative behind the housing weakness- not enough houses are being built. While that seems like a great problem, it’s not because that means prices are rising, hurting affordability and building isn’t growing as strong as it could be which stunts economic growth. Durable goods orders directly affect GDP growth. They fell 6.8% in July which was below expectations for a 6.0% decline. Bookings for transportation equipment fell 19%, led by Boeing which had 22 orders, which was down from 184 last month. Boeing stock is still near its all-time high, so this probably is the case of lumpiness rather than sustainable weakness. On the bright side, non-defense capital goods orders were up 0.4% which beat estimates for 0.3% growth.

These reports had a sharply negative effect on the GDP Now estimate as it fell from anticipating 3.8% growth to 3.4% growth. The NY Fed, which has been the most bearish this quarter, dropped its estimate from 2.09% growth to 1.93% growth. The St. Louis Fed expects 3.35% growth. The fact that July numbers are still impacting the estimates shows how we’re still only slightly above 1/3rd of the way through the data for Q3. Technically, with the many revisions which are coming, we still aren’t 100% sure what Q2’s GDP was.