In my last article, I discussed the possibilities of Yellen’s Friday speech at Jackson Hole. I was accurate in my expectation of what her speech would be on as the main point of her speech was to defend the regulations put in place since the last financial crisis. This was the speech of someone who is leaving their position. There’s no need to warn people about regulations being relaxed if she is staying at the helm. As I have said, it’s tough to say whether President Trump will pick a dove or a hawk, but the one thing that is certain is the Fed chair won’t be in favor of regulations.

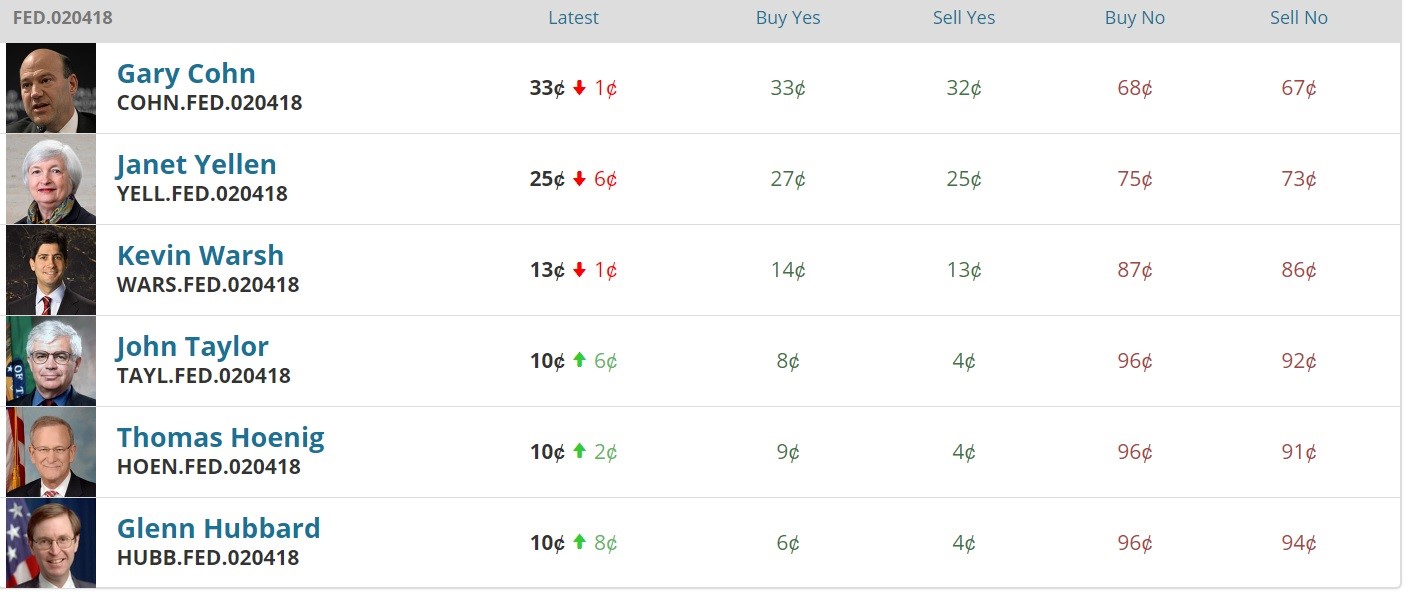

The list below shows the percent chances of each person being the next Fed chair in February 2018. This list is from the Predict It betting market. I consider it a very weird list because the top 2 people on the list seem like unlikely to take the job. Janet Yellen has a 25% chance of getting picked. Even though President Trump complimented her recently, it would be a PR nightmare to select her after he criticized her on the campaign trail. There’s also the philosophical difference on regulations which is quite dramatic. Gary Cohn is one of the most trusted people in President Trump’s cabinet, but it looks like Cohn won’t be picked either because former Fed governor Mark Olson told Cohn not to accept the Fed job it the President offers it to him. Olson’s reasoning is that Cohn doesn’t have any monetary policy experience. He referenced G. William Miller’s 1-year term as Fed chair under Carter not going well as evidence that picking an inexperienced chair isn’t a great idea.

President Trump may not care about whether the new Fed chair has specific monetary policy experience, but his hand will be forced if Cohn doesn’t accept the offer. To summarize, Cohn doesn’t have a clear path to the nomination because he might not want the job because he isn’t specifically qualified. There was also reports that Cohn almost resigned as Director of the National Economic Council after the events in Charlottesville. This further drops his stock. This explains why no one has above a 50% chance of getting picked. This is a big risk facing the market because uncertainty obviously can lead to a bad outcome. A bad outcome for stocks would be President Trump picking a hawk who isn’t concerned about how stocks react to monetary policy. I don’t think that would be a bad choice for the country and economy, but stocks would fall. Most economists who aren’t of the exact mold of Bernanke and Yellen probably won’t care about stocks as much. They have babied the market, making sure nothing spooks it.

Let’s briefly look at Janet Yellen’s comments on regulations. She said “the evidence shows that reforms since the crisis have made the financial system substantially safer.” Yellen, like other technocrats/politicians seems to think her policies on regulations are what saves the economy and it’s the market that creates the risk in the system. That’s a selective memory as she doesn’t acknowledge the proper lessons from the crisis such as the fact that interest rates were kept too low for too long. It’s tough for her to strike a balance on regulations, because she wants to promote the so-called progress the Fed has made, while acknowledging the potential for risk. She did a better job of that in this speech after she failed miserably in June making the dubious claim "I don't expect another financial crisis in our lifetime." That’s the type of quote that’s looked back upon ominously right after a crisis. It’s effectively saying risk has been made obsolete. It’s the type of statement someone with very little experience would say.

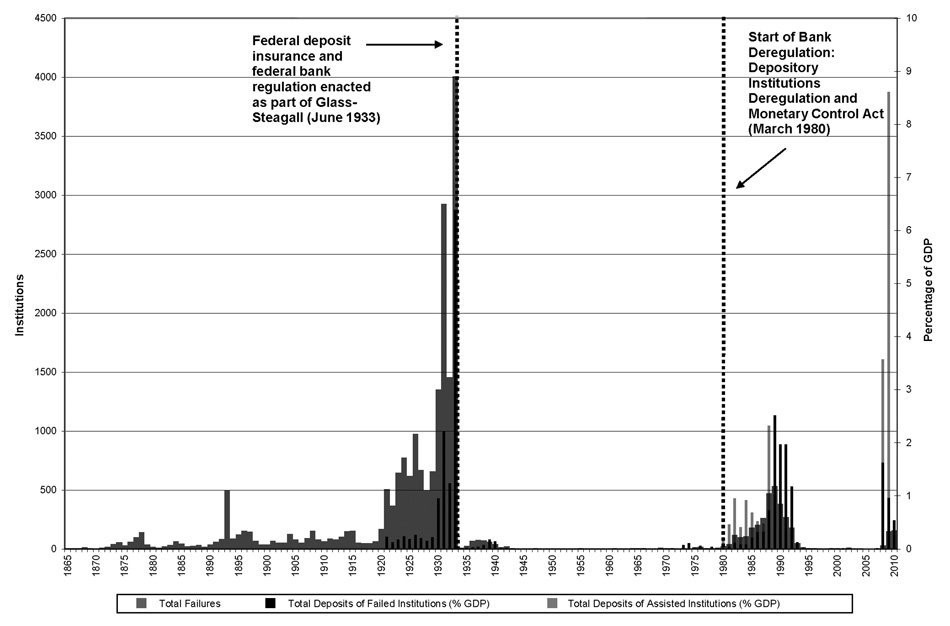

The chart below shows the periods of regulation compared to the number of failed banks. I don’t think correlation equals causation. Firstly, the regulations happened after the Great Depression. The implication that the regulations created this calm situation isn’t correct. The economy improved during that time making there less likelihood of bank failures. There’s also a cyclicality to regulations. At the end of cycles, deregulation occurs as the people want growth, forgetting about the last crisis. After a recession, new regulations are always enacted. The final reason why this chart is wrong is because it only shows two regulations. That’s a simplistic analysis to only look at two banking regulations when there’s hundreds of regulations and the business changes dynamically meaning old regulations sometimes aren’t applicable.

The two reactions to Yellen’s speech were that the dollar fell and the chances of rate hike in December fell. The dollar index fell 0.72% to a 1-year low. The chance of at least one rate hike fell from 44.4% to 42%. This would make you think the Fed was dovish. It’s tough to analyze this because there wasn’t any discussion on monetary policy. How could nothing be considered dovish? These aren’t major moves, so it might be algorithmic trading causing the action. That’s ironic because Yellen warned about the dangers of algorithmic in her speech. I think algorithmic trading can cause weird action in stocks, but I think systemic risk is caused by excess speculation combined with bad regulations and bad monetary policy, like what occurred in 2008.

Conclusion

The main takeaway from Yellen’s speech is it’s highly unlikely she returns as Fed chair which is bad for the stock market because she has been dovish. She didn’t discuss the rate hike which was considered dovish. The market might have thought that she needed to push the odds up if she was serious about the cut since it’s priced in at under a 50% chance. I don’t agree with that because she can be hawkish at the September meeting to push the odds up. That meeting will be important because it will tell us if a rate hike is happening this year and the final details about the unwind of the balance sheet.