What Will Draghi Say?

Yellen is speaking on Friday at 11AM. The same day, at 3PM, ECB chair Mario Draghi is speaking. There are conflicting reports about whether he will give new guidance about the tapering. I always thought he would give guidance in October or November because it’s closer to when the bond buying ends which is December. This policy has an end point, so if he were to not address it at all, then the bond buying program would end in December. It would be fitting for Draghi to make a policy statement at Jackson Hole because his policy has been inspired by the Fed. The rhetoric he uses is unique as he often says he will go to the end of the earth. That extremism has been backed up as the ECB has the largest balance sheet out of any central bank in the world. It’s easy to make extreme rhetoric.

The hard part is having a nuanced tone which is what is needed when a central bank is tapering. He can’t become fully hawkish because that would hurt the stock market. Nuance has befuddled Draghi this year as he has wavered from dovish to hawkish to dovish. I was confused by this volatility in his rhetoric initially; then I realized was he was simply trying to constantly cover up from his mistakes. If you want to be hawkish, but you strike too harsh of a tone, then you must backtrack by being dovish. It’s a messy process which might continue in the speech Friday. It will finally end when he announces the tapering. The question after that will shift to when the bond buying will end completely. I don’t delve too much into that because we don’t know what the initial taper will be or what the market’s reaction will be. The 20 billion euro tapering in April didn’t do much, but this one should be larger. I expect somewhere between 20-40 billion euros in tapering for the first 4-8 months of 2018. Then we’ll get another announcement like the one coming this fall right before that policy ends.

Just like how I said Janet Yellen would defend financial regulations in her speech, Draghi might defend QE in his speech like he did in his last speech this week. Draghi said: “Policy actions undertaken in the last 10 years in monetary policy and in regulation and supervision have made the world more resilient. But we should continue preparing for new challenges." I disagree with the resiliency factor because we don’t know the effects of QE until after it ends in 2018 or 2019. No one is arguing that the ECB policy made the current environment better, but the question is what the costs are. If the financial system was propped up for a few years, but then there’s an even worse crash in 2019, what has Draghi accomplished? That seems like a bad tradeoff.

Draghi went further by telling a journalist, "you need serious conceptual analysis and base policy on that, not on prejudice, or -- even worse -- on moral grounds. Some people say ‘Oh, QE is immoral, because it creates money out of nothing." Draghi like many politicians and technocrats loves to talk about how great his policies are without looking at the tradeoffs, making his critics look like tinfoil hat crazy people. Regardless of how he paints his critics, the obvious question is if these policies are so great and have no side effects then why is he halting them? The fact that he is halting QE is leaving him open for criticism. That’s the reason for his rant. It would be like conservatives supporting raising taxes or progressives opposing Medicare expansions.

The two takeaways from the point I am making is that the QE policy will have side effects and that Draghi will be tapering soon. There would be no need to defend his past policies if he was planning to keep them in place. His main critics come from Germany which feels QE helps Italy and Greece while hurting Germany. If he makes the same points he made in his last speech at Jackson Hole, then the market won’t react. If he’s hawkish, there will probably be a selloff. The timing of the speech is weird because it’s very important, but it’s also on a Friday afternoon at the end of August. The market reaction might not happen right away.

Economic News

Let’s now look at some of the economic reports which were released on Thursday. First let’s look at the jobless claims. Jobless claims remain very low as the weekly claims were 234,000 which was 4,000 below expectations and up 2,000 from last week. There’s not much to say other than the labor market remains strong.

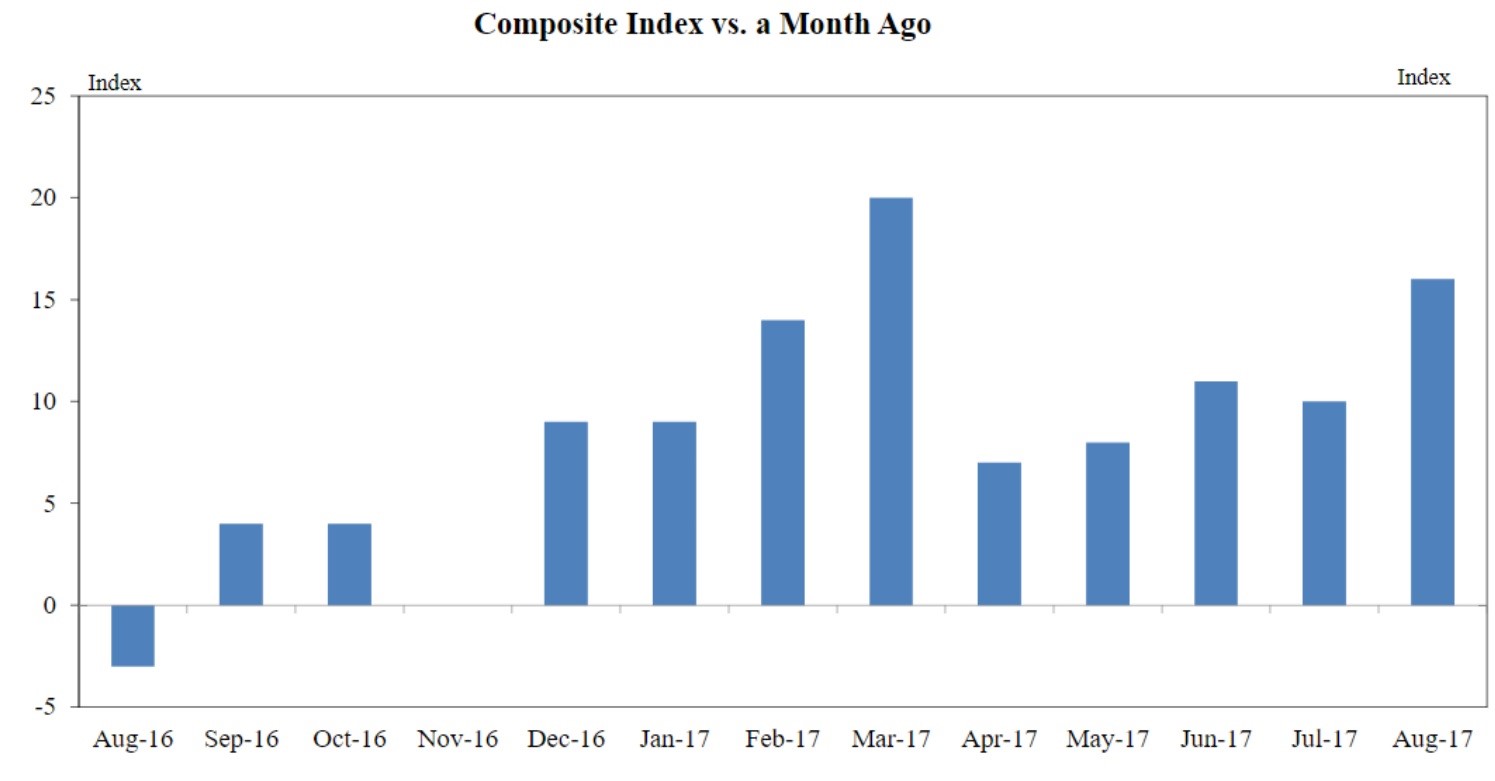

In keeping with my thesis that the Markit survey was wrong to say there is manufacturing weakness, the Kansas City Manufacturing survey showed improvement. As you can see from the chart below, the seasonally adjusted month over month index increased from 10 to 16. The most interesting quote was the following: “Health insurance premiums increased 22% in current year. Next year may be too expensive to maintain coverage for employees.” This shows how healthcare reform isn’t just a political football. There will be real world consequences if the healthcare system isn’t improved by next year. It will have a negative impact on the economy; the only question is how much.

Conclusion

The economy is in great shape as the jobless claims and Kansas City Manufacturing reports show. However, this won’t matter if Draghi or Yellen give hawkish forward guidance on Friday. I’m not expecting any bombshells, but you never expect bombshells and they still occur. It will be interesting to see how the new Fed chairperson deals with Draghi and other global bankers. Setting monetary policy should be influenced by what other central bankers are doing. This should be an obvious concept, but President Trump could pick someone who isn’t familiar with the nuances of the job, so it’s worth pointing out.