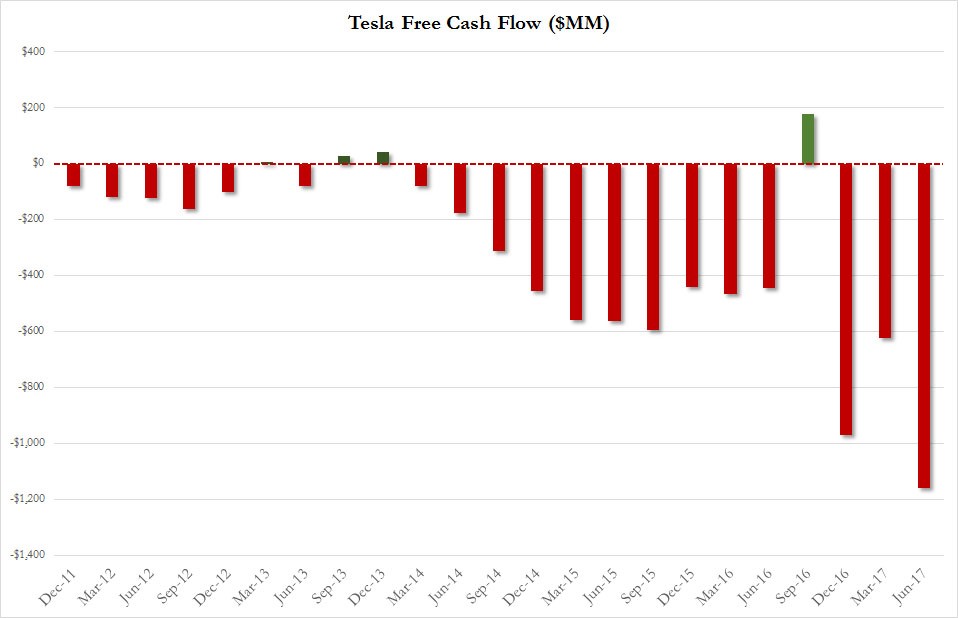

The story that got the most buzz in the financial press on Wednesday was TSLA - Tesla’s earnings report which beat expectations sending the stock soaring over 7% after hours. The adjusted loss per share was $1.33 which was less than the expected loss of $1.82. The revenue was $2.79 billion which beat expectations for $2.51 billion. The bears will point to the disastrous cash burn seen in the chart below as a reason to be concerned, but it hasn’t been an issue to investors as the stock has rallied after years of having negative free cash flow. There is a bait and switch among Tesla bulls where they say each new car launch was paid for by the previous one; then when you show them the negative free cash flow, they say the company needs to invest in producing more cars. Not all firms need to run negative cash flows to invest in new production. Most firms are self-sufficient- they use their working capital to fund new initiatives.

Most of the debates this earnings season about the high-flying names like Netflix, Amazon, and Tesla have been the same ones that have been happening for many quarters. In Tesla’s case, the bears usually make better points, many contentious comments are made, Elon Musk says unintelligible things on the conference call, and the stock moves higher. It’s a dystopian world we live in. The craziest quote from the conference call was when Musk said, "If you go to our stores, we don’t even want to talk about it [Model 3] really." The point of that statement is that Model 3 has so much demand that the company doesn’t need to market it. He has said the ramp up is ‘production hell’ in the past. This would mean the company has the high quality problem of having too many orders.

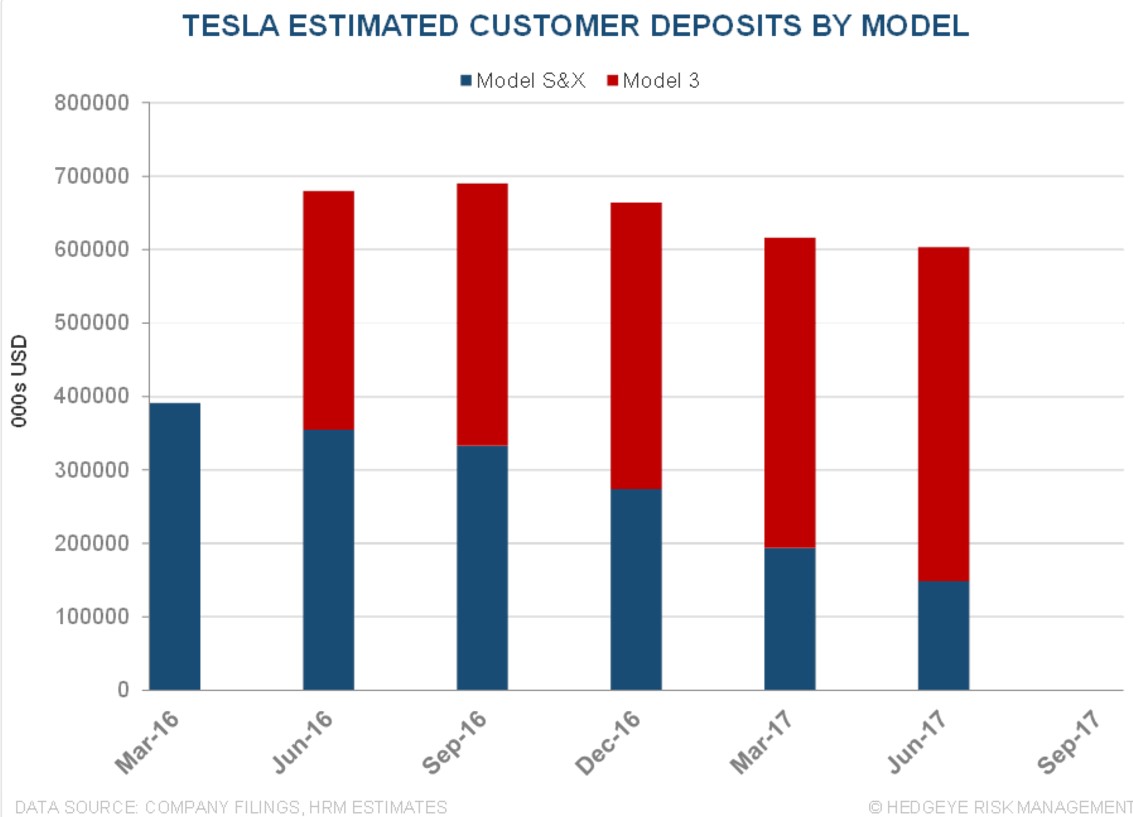

The truth about the number of deposits for the Model 3 is that they are falling. Musk breaks down the number of deposits for the Model 3 by gross and net deposits. A gross deposit is everyone that put a $1,000 deposit on the Model and the net is the number who haven’t taken their money back. The company has 518,000 gross deposits and 455,000 net deposits which means 63,000 people have canceled. This isn’t surprising to me because most people probbaly got excited by the new car, but then realized it wasn’t coming for over a year, so they cancelled the deposit.

It is human nature to get excited by a new product and then sober up. If you actually need a car to drive to work, buying one over a year in advance is nonsense. The chart below shows that deposits for the Model S and Model X have fallen in the past few months because of consumers shifting their demand to the Model 3. That’s a problem for Tesla because the Model 3 is the cheapest. In theory that would mean that Tesla would make less money, but it’s tough to tell because Tesla doesn’t make a profit on any of the cars it sells. This is the exact opposite strategy that Apple employed with its iPhone. Apple started with the lower priced devices to get consumers interested and then worked their way higher by building premium devices to improve margins.

Most of the numbers Tesla reports won’t matter until we see how well the Model 3 performs. Investors who are bullish on the name have been buying the stock for years in anticipation of a cheaper, mass-market car. The first few cars were delivered this week to Tesla workers as they test out the kinks before regular customers get a chance. Before anyone can buy a Tesla, the car will be sold to those who already have a Tesla, to further control the narrative surrounding the publicity of the product.

Speaking of the lower price, Tesla has gotten much criticism because it promised the car would cost $35,000, but that base model isn’t shipping at the start of the launch. The car will cost between $45,000 and $50,000 for many customers who want the autopilot feature and other options such as a color other than black. This situation was predictable because Tesla isn’t exactly a master of cost control. The company couldn’t make a profit selling more expensive cars, so it was obviously going to be difficult for the average selling price to be in the $35,000 to $40,000 range. The Model 3’s price is definitely in the luxury category, but is more affordable than anything it has ever offered.

What will determine where TSLA stock will end up is how satisfied the initial customers are with the Model 3. We will find that out in the winter when more cars are shipped and the company ramps up production. Ramping up production will be tough as more things can go wrong than ever before. The bulls are obviously confident in Elon Musk and Tesla, so there is no chance that they would sell the stock right before we find out how well Model 3 does. The changes in the deposits don’t matter much because none of the issues are with the car itself. If pre-orders dip in 2018, we’ll know that the product was a flop, but until then, it’s all noise. I am open to the bears’ argument, but I recognize that it hasn’t worked.

The only way for the stock to fall is if investors lose faith in Elon Musk and the product. The fate of the company relies on the performance of the Model 3. Even if the Model 3 is successful, I wouldn’t buy TSLA because of its valuation, but I wouldn’t be surprised if it moves higher. The biggest problem I have with Tesla, besides the losses, is that the world is shifting to a sharing economy where cars aren’t owned by one person. If cars are autonomous and shared, this lowers the amount sold which crimps the addressable market.

In closing, much like Apple, Tesla reported a ‘nothingburger’ quarter because everyone is focused on the success of Model 3. The next quarter will also not matter much, but the one after that will give us a glimpse of how sales are going. There will be a lot of media coverage of the car’s performance; it will be impossible to miss.