It’s important to recognize that there are many people in the financial industry who will never change their minds regardless of the facts. When you realize that, you become more skeptical of every opinion, which is a great skill to hone. For example, mutual fund managers are always optimistic about the long term because they want investors’ money. It’s possible to be optimistic about your own performance and pessimistic about the market, but the industry likes to keep it simple by remaining optimistic to avoid scaring people out of the market. If many managers were warning of a crash, some investors would pull out of everything instead of going with a manager who is hedged. Hedging isn’t a concept understood by some non-professionals.

On the bearish side, there are is an industry dedicated to selling doom and gloom to reinforce people’s biases. Some of the bears become addicted to reading dire stories which is why this industry has survived without being right in years. Just because stocks have done well recently, doesn’t mean doom is around the corner; more objective research needs to be done. The final group of individuals who are entrenched in beliefs are those who don’t want to change because they are emotionally attached to their positions. It’s important to differentiate between healthy skepticism and constantly changing your mind. It’s a subtle point that takes a lot of work, but getting it right makes you a skilled investor. You must be open to different perspectives without necessarily changing your mind every time you hear a new point. The key is to figure out which point will move markets and avoid acting on ‘noise’ which is interesting, but not actionable information.

The chart below is one example of bullish earnings arguments which are illogical. The point is that it is biased to only look at the positive perspective when negative events occur. Bulls ignored housing earnings, GAAP earnings, and went back and forth on energy depending on if it did well. The point isn’t that you must always be bearish when these silly arguments are explained. The nuanced point is to know what you own and why you own it. You should’ve bought stocks in 2014-2016 if you were bullish on total earnings, not because energy earnings don’t matter. Every sector matters because, at the most, it can cause a cascading effect on the economy like housing did and, at the least, it can weaken total earnings like energy did.

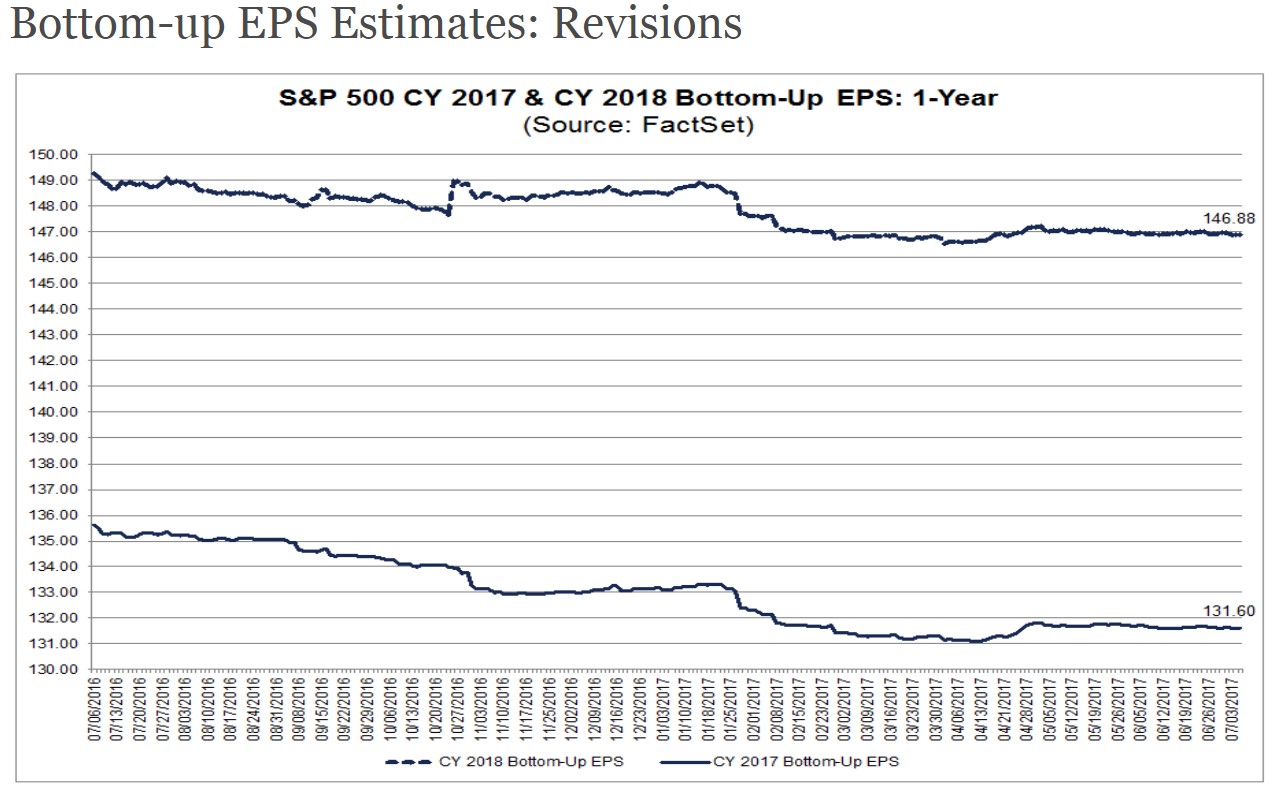

While the bulls focusing on the earnings growth of the past few quarters being boosted by energy after ignoring the energy declines is disingenuous, it doesn’t imply the earnings situation is bad. As you can see from the chart below, there hasn’t been much of a change in bottom-up 2017 earnings estimates in the past 3 months. It has been stuck at just below $131, using the Fact-Set results. On a less important note, the 2018 earnings estimates have also been stable. Q1 earnings were so great that estimates improved, which is a rare feat. A big part of that was international earnings growth. I will delve into how that effects future results in a moment.

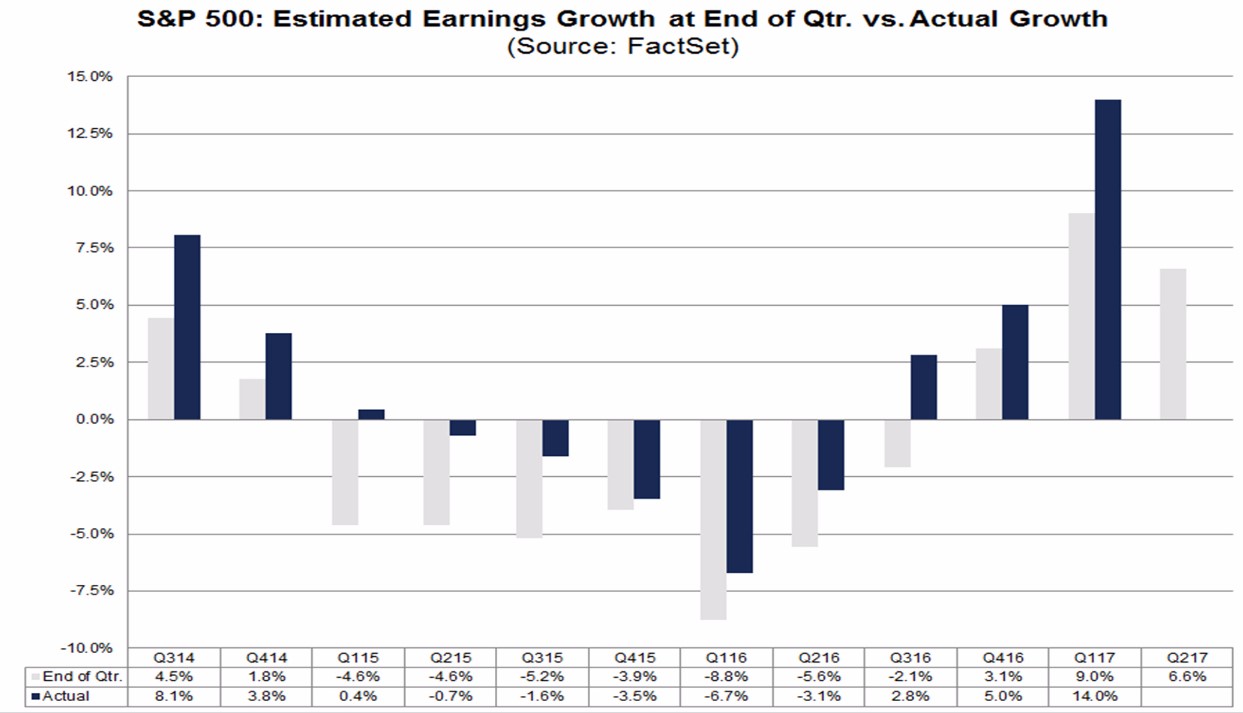

On the negative side, earnings growth is decelerating. This doesn’t meant stocks will fall because it was expected that 14% Q1 earnings growth was unsustainable. It was boosted by the easy -6.7% year over earnings results in Q1 2016. Not only are sequential earnings estimates up against tough comparisons, but also the actual results are tough to compare with because of the 5% beat which was above average as you can see in the chart of recent results. This sequential decline has been caused by a deceleration in revenue growth despite an acceleration in margin expansion.

The key question which will impact stocks is when the margin expansion slows since revenue growth hasn’t driven this rebound in earnings. Energy is the most responsible for the latest margin improvements. I will use the S&P Dow Jones numbers to illustrate these points. In Q1, year over year sales growth was 6.84% and in Q2 it’s expected to be 4.75%. In Q1, margins were 9.84% which is closing in on the ceiling I believe exists based on historical results. However, Q2 estimates don’t see the ceiling being hit yet as analysts are expecting margins to be 10.40%. That’s a 15.16% year over year increase which is above last quarter’s 12.46% increase. The headwind to further margin expansion is the energy sector which must deal with mid-$40 oil and the end of easy comparisons. In Q1, the earnings contribution to the S&P 500 increased 7.48% year over year, while in Q2 it is expected to improve 5.96%. That isn’t bringing down margins yet, but the headwind gets stronger as we go into the future. Q3 is only expected to have a 3.16% improvement. To be clear, these are net improvements, not percentage changes because 2016 had negative contributions. To get the 7.48% change I subtracted -3.41% (Q1 2016) from 4.07% (Q1 2017).

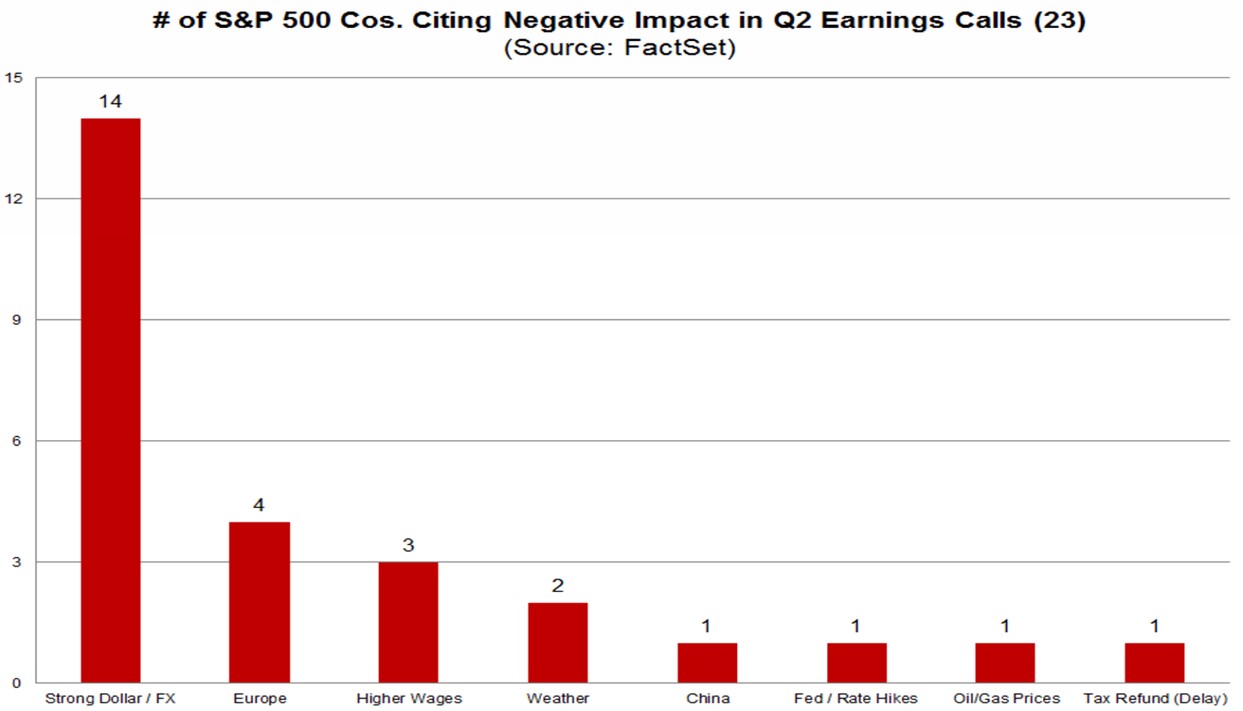

On the positive side, the weakening dollar might be a reason to be more optimistic about second half 2017 earnings. First, I’ll mention that the decline in oil in the face of a weakening dollar shows the downtrend’s strength as supply floods the market from the OPEC nations which don’t have to cut production. As you can see from the chart below, so far in Q2, 14 firms have mentioned the strong dollar as a negative impact to earnings. The dollar index is down 4.99% in the past 3 months, so this headwind may be lifted soon. The dollar is now down about 1% year over year which is a big change from the about 4% year over year increase in April. Since international earnings drove this rebound from the earnings recession, this dollar tailwind might catalyze second half earnings beats.