It's turning out to be tough to analyze what ECB President Mario Draghi means in his statements. It was widely reported by media outlets and interpreted by the markets that the ECB would taper bond buying after Draghi made upbeat statements about the economy. However, Draghi clarified his statements on Wednesday, saying the ECB isn’t planning on tapering soon. The market keys on tone and word choice. It’s so precise that the market can read things which aren’t there and Mario Draghi can make an unintended change to policy by saying something new. On the other hand, you can argue that Draghi was hawkish in his last statement. He only changed his mind because he didn’t like the way market were pricing in expectations. This is the new world we have been living in since the financial crisis. The most important catalyst for bull markets has been what central bankers say. Draghi is afraid of a taper tantrum for good reason.

If the ECB ends the bond buying, equities will fall. It’s tough for me to make a statement on what the ECB will do in the fall because it keeps changing its mind, seemingly weekly. As with any important market moving decision, there’s a lot of uncertainty. If there wasn’t uncertainty, the changes would be priced into the market. I expect 2018 to be a bad year for global stocks if the tapering is sharp. I expect a continuation of the bull market, if it is soft. The base case seems to be a 30 billion euro taper which means anything less is bullish and anything equal or greater is bearish.

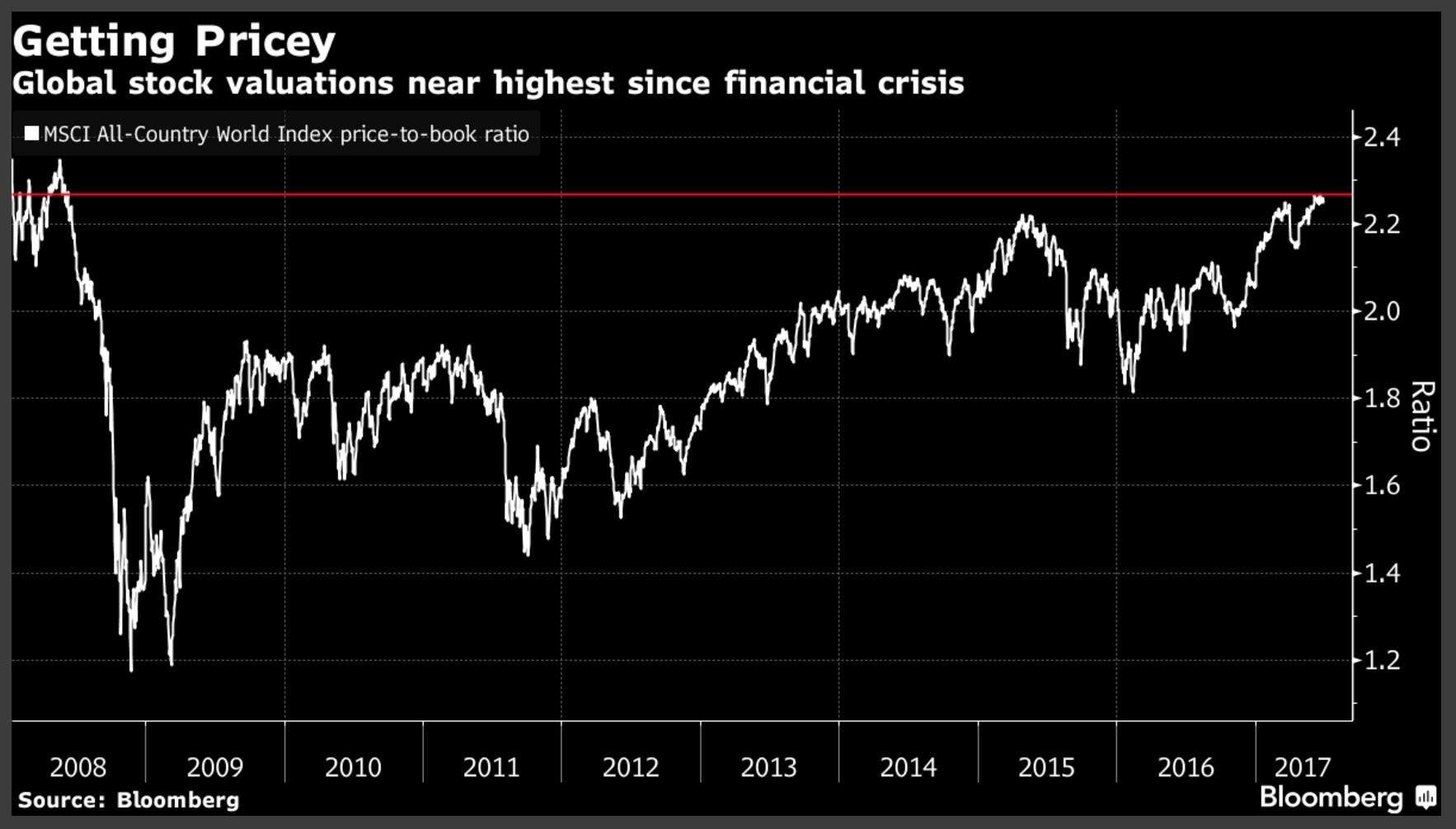

On Wednesday, the stock market forgot about the healthcare bill having some trouble as stocks were bid up on the back of this dovish statement from Draghi. The Nasdaq was up 1.43% and the S&P 500 was up 0.88%. If you can predict what Draghi will say next, you can predict the short term movements in equities. The chart below shows the MSCI price to book value is now at the same level it was at before the financial crisis. That’s the trouble with the addiction to central bank intervention. The more intervention, the greater the decline after it’s taken away. The problem is if it is taken away, that crash happens sooner. To make things even more complex, the central banks must provide guidance that the interventions will end because if they don’t stocks would never fall. The bull market would be even stronger than it is now. Efficient capital markets improve productivity. They become inefficient with bond buying as the risk-free rate is altered. If the central banks said they would never unwind or taper, even more inefficiencies would occur. It would hurt long-term real economic growth potential.

Although American earnings have been doing well because of international growth, global profit estimates are being cut. As you can see from the chart below, the Citi Global Earnings Revisions Index is showing negative revisions for the first time since February. It looks damning to see revisions negative while the price to book value is so high, but the same situation happened in 2016 as you can see. Valuations effect long term returns, but they haven’t effected returns in the past few years. The question is when the long term arrives. Looking at valuations, you’d expect American stocks to deliver almost not returns annualized over the next 10 years, but stocks have increased in the past month. Stocks have increased more this year, than long term valuation metrics have predicted they’d go up in 10 years. At some point the expensive valuations will cause a large correction or extended period of underperformance.

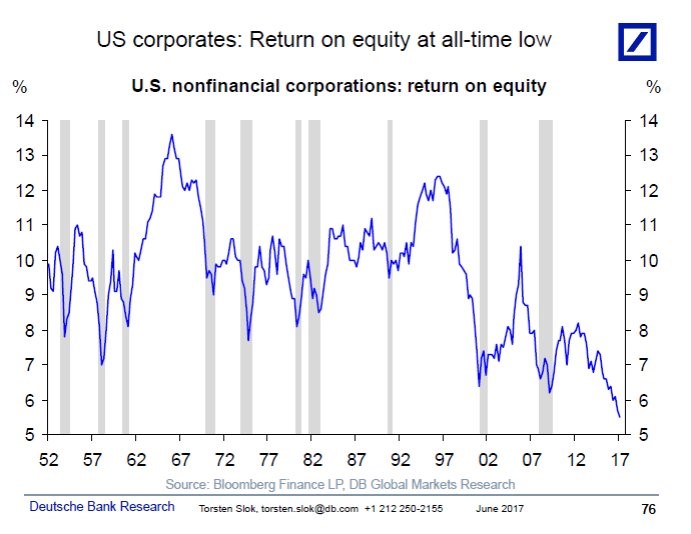

The chart below furthers the evidence that buying stocks based on valuations with a plan to hold them long term makes no mathematical sense. As you can see in the chart, for U.S. corporations, return on equity is at an all-time low. Return on equity is the amount of profits a firm generates with the capital shareholders infuse into the business. With return on equity at the lowest ever, it has never been a worse time to own stocks. You can probably find a diamond in the rough, but when the market returns to rationality, all stocks will fall together. It’s very frustrating for me to tell non-financial people about how stocks are a bad long-term deal because they see them rallying when they watch the news. The next movement might be for return on equity to fall, but in the long term it will mean revert.

Stocks are different from other less liquid assets because of the ability to sell them at any time. You probably wouldn’t buy a house which was 50% overvalued because it would take time to sell it. Within that period where you’re trying to list it, the price can fall. With stocks being traded every day, mom and pop investors make the miscalculation that they can get out before the selloff. I will continue to write articles on monetary policy, fiscal policy, the economy, earning, and valuations, but I recognize that calling the exact top is futile. For now, speculators are willing to take a chance on a bad deal because of the greater fool theory, but it cannot last.

Conclusion

Draghi either changed his mind or was misinterpreted. Either way, the market now sees him as dovish so stocks rallied to within less than 1% of their all-time high. Earnings revisions for global firms are now negative, but that isn’t stopping stocks. More importantly, return on equity ratios are at their all-time low. It’s a bad deal to buy stocks for the long-term. Everyone thinks they can time the top or they convince themselves that stocks are a great deal. The proof is in the numbers. If you buy stocks with a low return on equity, you’re locking in low returns with the potential for a sharp drawdown in the meantime.