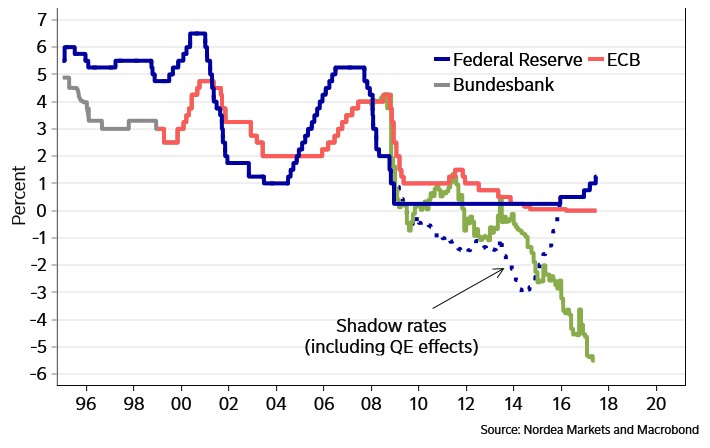

The chart below adds more depth to the traditional understanding of interest rates. This chart looks more confusing than it is because the grey line represents the Bundesbank policy before the ECB was created. The dotted line is the Fed’s shadow rate including QE and the green line is the shadow rate of the ECB which includes its QE. I have discussed previously the shadow rate of the Fed, but what I’ve never seen before is the shadow rate of the ECB. The ECB has the largest balance sheet out of all the central banks. It’s continuing its downward trajectory as there has been only a momentary unwind in 2013-2014. It’s nearing -6%. With such extraordinarily easy monetary policy, Draghi shouldn’t consider moderate growth and 1.4% inflation as a major win. This is a low bang for QE’s buck. It’s like getting a power washer to remove a leaf from a house. The policy hasn’t done much. Either QE isn’t a major factor for the economy or its masking massive weakness which will be renewed once the bond buying is tapered. We will see the results once the tapering accelerates in January 2018.

Economic Reports

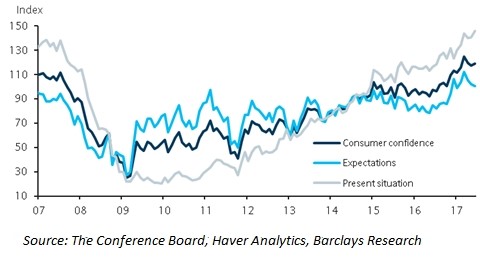

The consumer expectations index was released from the Conference Board. It showed moderate improvement as you can see from the chart below. It went up from 117.6 to 118.9. The Present Situations index rocketed to 146.3 from 140.6. As you can see, it is right where it was in 2007 before the financial crisis. The Expectations index fell from 102.3 to 100.6. The Present index breaking above the Expectations index might be a late cycle indicator as this also happened in 2007. The question is when the negative catalyst that consumers see will impact them. Maybe they don’t have faith that tax reform will pass.

On the negative side, the U.S. home prices index grew 5.5% in April which missed estimates for 5.9% growth. The S&P/Case Shiller index increased 5.9% in April of 2016 and 5.8% in March 2017. The managing director and chairman of the index committee said demand was rising and supply couldn’t keep up. The quote taken from him was "The question is not if home prices can climb without any limit; they can't. Rather, will home price gains gently slow or will they crash and take the economy down with them? For the moment, conditions appear favorable for avoiding a crash." I find it perplexing that he would bring up a crash with the Case-Shiller index showing such steady growth. Maybe he has recency bias by being nervous about a crash since the housing market just had a crash in 2008. It’s either that or he’s seeing something in the market that is more negative than the price action suggests.

I think the housing market will be hurt in the next recession, but the lending standards didn’t diminish like they did in 2000-2005 which means there won’t be a huge burst. This cycle the housing bubbles are in Australia, Sweden, and Canada. In Sweden, they have interest only loan payment structures. With the American housing bubble, fresh in our minds, we know what to look out for when we see the factors playing out in other countries. I expect those markets to burst sometime in the next 2-3 years.

The chart below shows the vacancy rate for apartments. As you can see, it’s beginning to tick up slightly. This increase from 4.2% last year to 4.4% isn’t a big deal, but it could signal an impending downturn in apartment real estate in 2018. Average rent prices were up 3.0% year over year. Shelter has been where inflation has centered this cycle. There will be a lot of new inventory coming online in the second half of the year, so vacancy rates will increase further. If an economic downturn occurs in the second half, it would amplify this negative momentum. On the bright side, second quarter construction was the lowest in two years. This may be a negative signal for the economy and the apartment market, but it means the vacancy rate will stop going up in 2018. If vacancy rates were to increase further, prices would fall. This decline in building might prevent that. From the consumer’s perspective, they wouldn’t mind a break on their rent costs because the rent as a percent of GDP is at a record high.

Investors Not Confident?

On Tuesday, the State Street Investor Confidence index was released. 100 is a neutral rating. The global index fell to 101 from 102.6. The North American reading fell from 104.2 to 102.2. I usually don’t care about investor sentiment because the prices of stocks tell you all you need to know. However, I find this noteworthy because you would expect sentiment to be high given the expansive rally this year. In January 2016, during the last correction, the U.S. investor confidence index was 108.8. Investors are worried about oil prices falling and valuations. I find this fear to be good news as excessive optimism signals the top is likely in. I wouldn’t buy stocks on this news because those investors in the survey are right; stocks are expensive. However, this skittishness could fuel the rally in the near term.

Conclusion

The ECB tapering its bond buying is a bigger story than the Fed unwinding its balance sheet. The amount of money is higher. Currently the ECB buys 60 billion euros per month which translates to about $68 billion. At the peak of the Fed’s unwind, it will only let $50 billion in bonds expire. We may never get to that point because a recession will probably occur in 2018 or 2019. The ECB is now at an almost -6% shadow interest rate. Even getting back to 0% would be a tall task.

Even though I’m open to the bearish thesis, I’m surprised to see the director of the Case Shiller index say housing prices can’t rally forever. In the housing bubble of 2000-2006, commentators thought housing prices would rise forever. This concern is exactly why I’m not as worried about housing as I am about the student loan and auto loan sector.