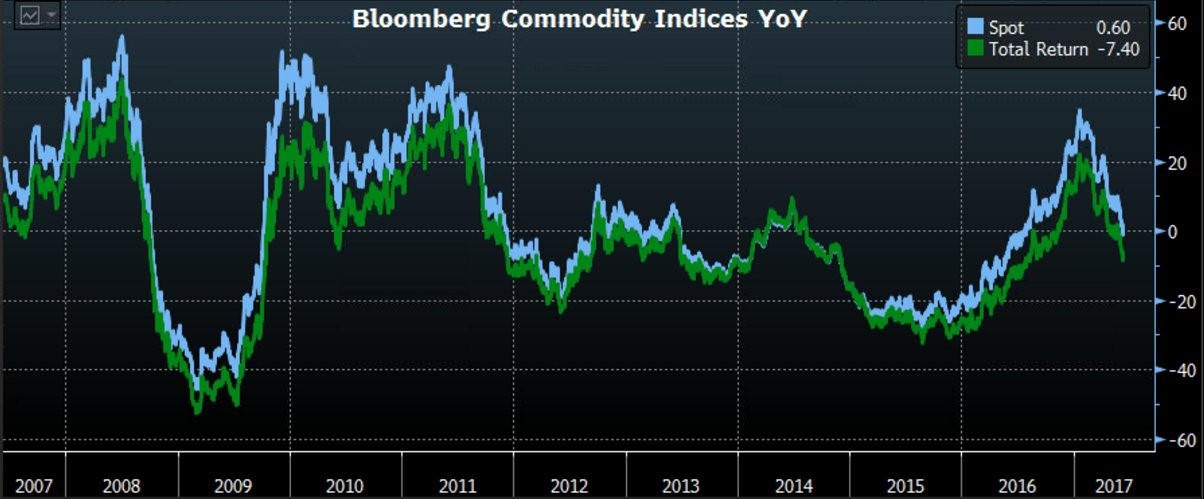

The chart below explains why inflation has been falling lately in Europe and in America. It shows the change in the year over year Bloomberg commodities index. There is a clear trend of disinflation led by oil. Wage inflation isn’t accelerating, so there’s no reason to expect any of the headline inflation numbers, whether it’s PCE or CPI, to look differently than this chart. The ECB took the ball and ran with it by putting out guidance which suggests it will extend the bond buying program when it realized inflation was waning and GDP growth was accelerating. That’s a logical step if the ECB was afraid QE would cause inflation. The 1.5% inflation rate in Europe is the same rate it was at before QE, which implies the ECB thinks there was a mega trend which reversed all its inflation creation. This is a farcical idea.

Regardless of whether the ECB is correct in its assertion about QE causing inflation, this is bullish for stocks as the ECB’s $60 billion per month bond buying program is now more likely to be extended. The Fed is making its decision on interest rates on Wednesday and will give a more detailed explanation of its balance sheet unwind. With inflation declining, the market is giving the Fed an out from raising rates and unwinding the balance sheet. The question remains if the Fed takes the ball and runs with it like the ECB did. At some point soon, the Fed will have to acknowledge the reality about inflation. If you use the word transitory liberally, any move in any market is transitory. If the Fed remains in the camp that this disinflation is transitory, it is using the word in that manner. Either at this meeting or soon after, the Fed will have to decide how to react to this change. It can either do what the ECB did or keep going with its plan to raise rates and unwind the balance sheet.

You may be wondering why the Fed would raise rates after the acknowledging inflation is falling. For a few months, inflation was at the Fed’s target, but that was only an excuse to raise rates. The reason the Fed was hawkish was because it expected wage inflation to rise due to a tight labor market, it wanted to get off the zero bound so it can cut rates in a future recession, and because the bull market in stocks allowed it to raise rates. None of those factors have changed. The labor market is the same as it was 6 months ago, the stock market is still near all-time highs, and rates are still close to the zero bound.

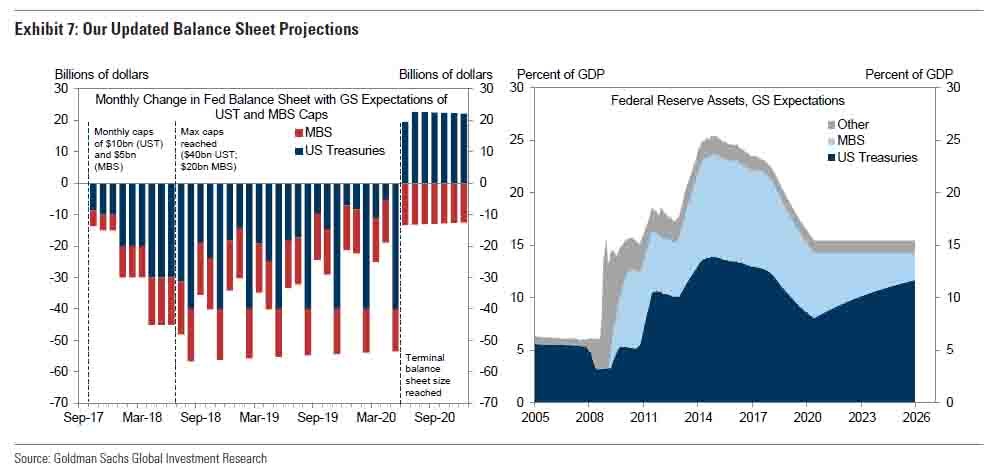

My base case scenario remains similar to what it has been in the past few weeks. The Fed has said it will pause hiking rates during the beginning of the unwind so it doesn’t spook the market. This allows the Fed to stop raising rates during this bout of disinflation without changing its plans. The odds for the third-rate hike will depend on what the Fed says Wednesday. The chart below shows Goldman Sachs’ forecast for the unwind based on what the Fed has said. The fact that the stock market doesn’t care about the unwind or the rate hikes is something the Fed may want to take advantage of even with the low inflation. It already ignored the weak Q1 GDP report even though it admitted the weakness wasn’t caused by the weather, so ignoring disinflation isn’t a stretch.

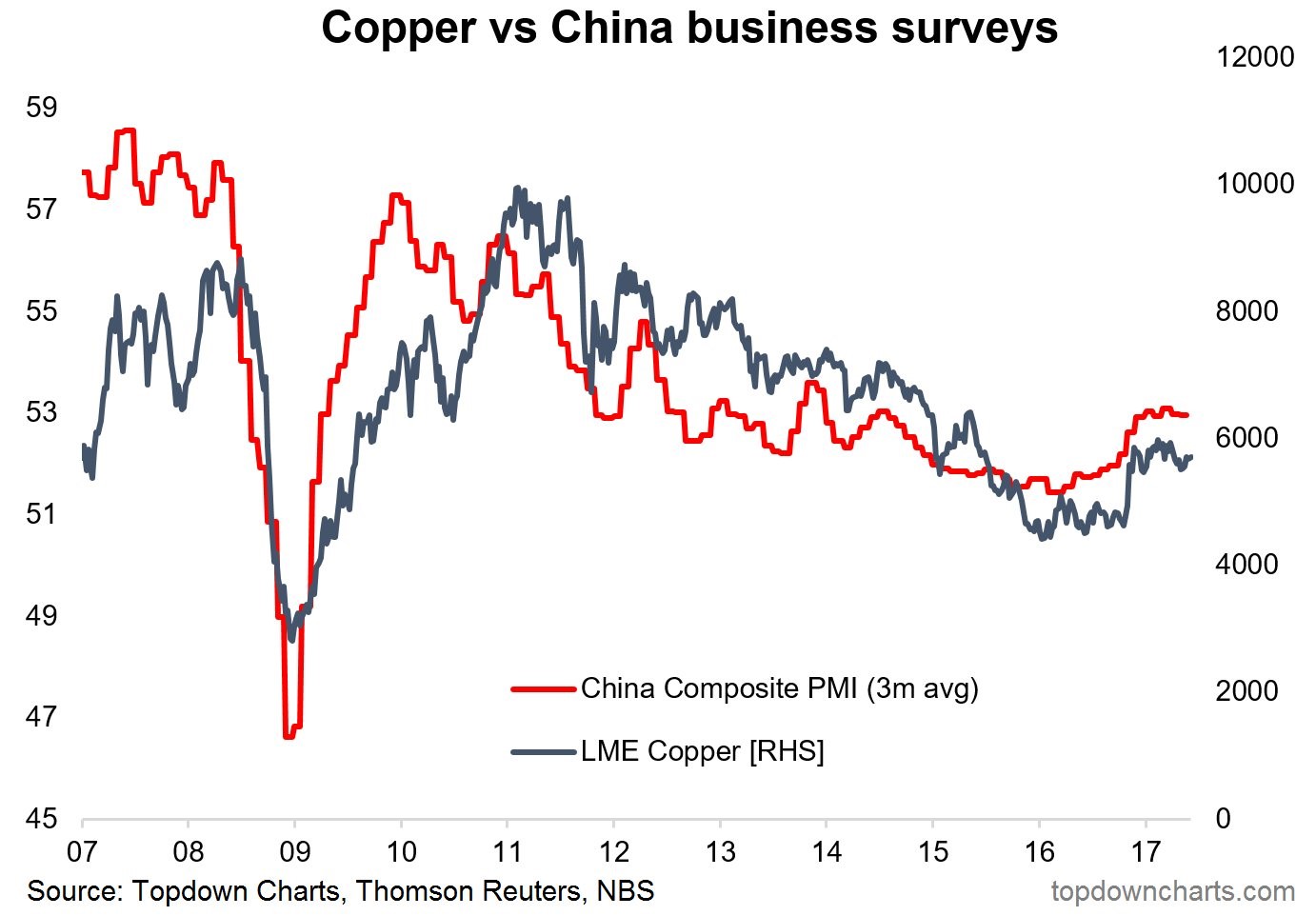

The chart below gives a description of why commodity prices have fallen. As you can see, China’s composite PMI has fallen alongside copper prices. China has done its biggest stimulus since 2009, but there has only been a slight increase in the purchasing managers index and copper prices. If China’s stimulus had worked, commodity inflation would be much higher. It’s important to acknowledge that central bankers have a myopic viewpoint on the economy. They over emphasize the good that they do and under emphasize the bad things they do. It’s human nature. Since investors can’t be myopic, looking at the Caixin China manufacturing PMI, the May report fell to an 11-month low hitting 49.6. This was below expectations for 50.1 and fell below 50 which signals a contraction. Given the fact that 2017 is an election year for China, I think extra stimulus put lip stick on this pig of an economy. With the election over in the fall, China may ease off the stimulus gas pedal which could further this decline in commodity prices.

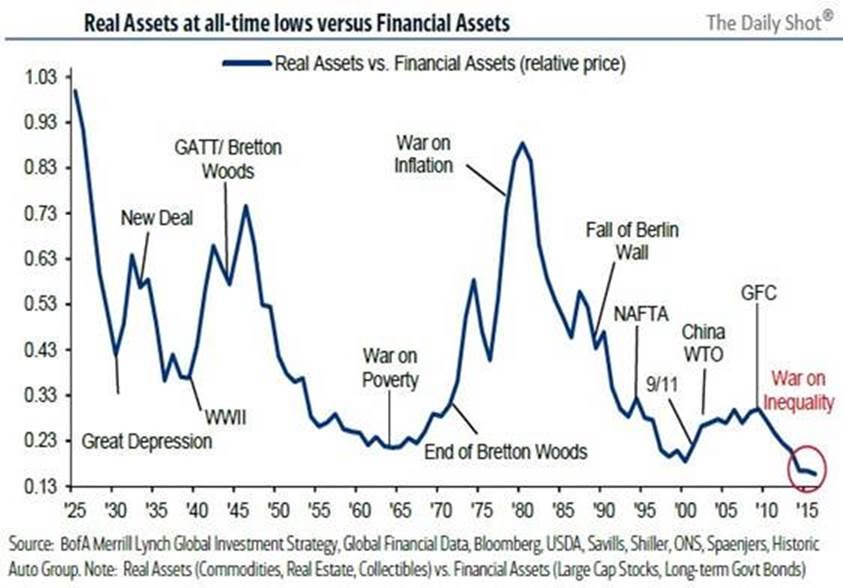

This brings us to the chart below. The ratio of real assets to financial assets is near an all-time low. The decline in commodity price inflation and the increase in stock prices has caused this as QE has lifted stock prices. Low interest rates create an environment for this relationship since stocks become the only game in town. It’s a catch-22 because the Fed won’t raise rates unless commodity prices rise, but this relationship is falling because of low interest rates boosting stocks. Also, the Fed is happy with this relationship. It doesn’t want to see the inflation of the 1970s. That inflation was spurred by the price controls Nixon imposed in 1971 which were eventually lifted causing businesses to make up for lost ground, the OPEC oil embargo, Nixon eliminating the last connection the dollar had to gold, the large budget deficits, and the Fed’s refusal to fight inflation by raising rates. This all spurred inflation and caused stocks to fall 40%. For the current relationship to end, I think the stock market’s record valuations would have to fall. In the 1970s, leadership thought endless inflation was fine and now they think endless stock price increases mean the economy is healthy. Both are foolish.

Conclusion

If the Fed decides to be more dovish because of the latest disinflation, I think stocks will rally. The endless cycle of low GDP growth, low inflation, and high stock prices would continue. A few weeks ago, I said this Wednesday meeting wouldn’t matter because the Fed gave most of the details about the unwind in the Minutes in May and because a rate hike is almost a guarantee. However, with the inflation data changing, I am going to key in on whether the Fed emphasizes this change or ignores it. It’s going to be the guidance I need to forecast future policy actions.

1 Comment

Zac

June 12, 2017I would like to see a lot more of this material I am tired of Hindsight charting