The first revision to Q1 GDP was released Friday. This is the report I was waiting for ever since the 0.7% growth report was released a few weeks ago. I have said that it’s important to take each first guess at GDP growth with a grain of salt because the number is subject to revisions. Economists were expecting the GDP growth rate to be revised to 0.9% growth. It beat expectations by coming in at 1.2%. This report is more consistent with the strong labor market. The U.S. macro surprise index was positive in Q1 and has since fallen to a 15-month low. Having a very weak Q1 GDP number and a very strong Q2 GDP number was at odds with the macro surprise index. While it still differs, the divergence shrank. While the revision was a positive, this may pull back some of the growth bump expected to occur in Q2. In that case, this news is a wash. It simply smooths the data, but doesn’t change the fact that the economy probably grew at below a 2% rate in the first half.

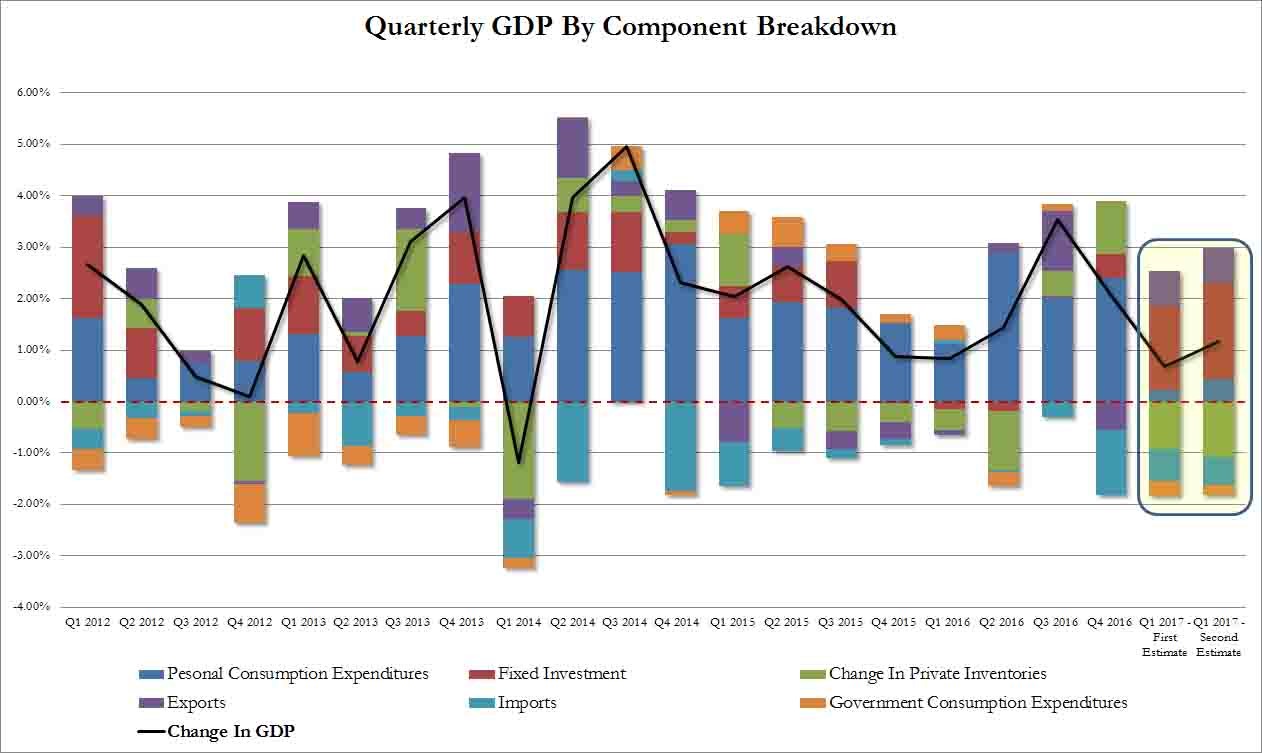

The 1.2% GDP growth revision for Q1 was still the weakest growth quarter in a year. I think the argument that Q1 reports are always weak is a silly excuse because the BEA has already made changes to fix that problem. There will always been refinements to data collection, but there have been a few Q1s which have been great which makes this hypothesis faulty. The chart below breaks down the contribution changes from the original Q1 GDP estimate and the second estimate. As you can see, there were upward revisions to business investment, consumer spending, and state and local government spending. There was a downward revision in inventory investment. Inventory investment may also decline in Q2 as the April wholesale numbers showed a 0.3% month over month drop.

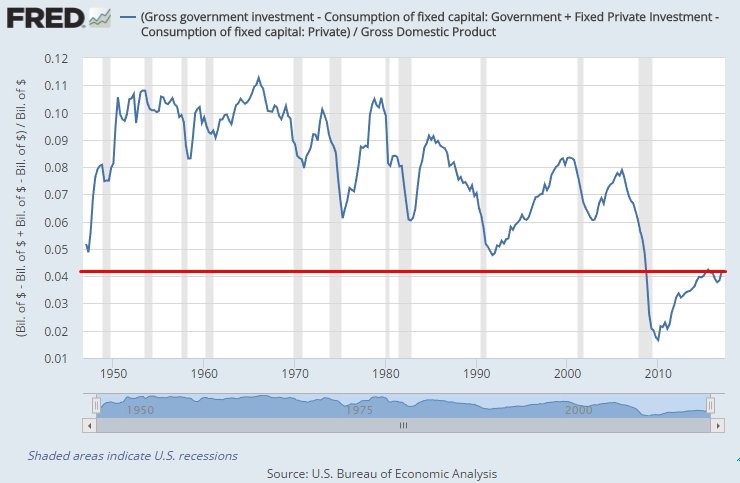

Fixed investment grew 1.85% which was an upward revision from the original estimate of 1.62% growth. Weak private fixed investment growth is responsible for the decline in productivity growth. Interestingly research and development as a percentage of GDP hit a new record in Q1, increasing to 1.84%. Even though there was an increase in R&D spending as a percent of GDP, the productivity growth remains low because of low growth in the capital base. As you can see in the chart below, the net government investment and net private investment divided by GDP is half the rate seen at the prior two cycle tops.

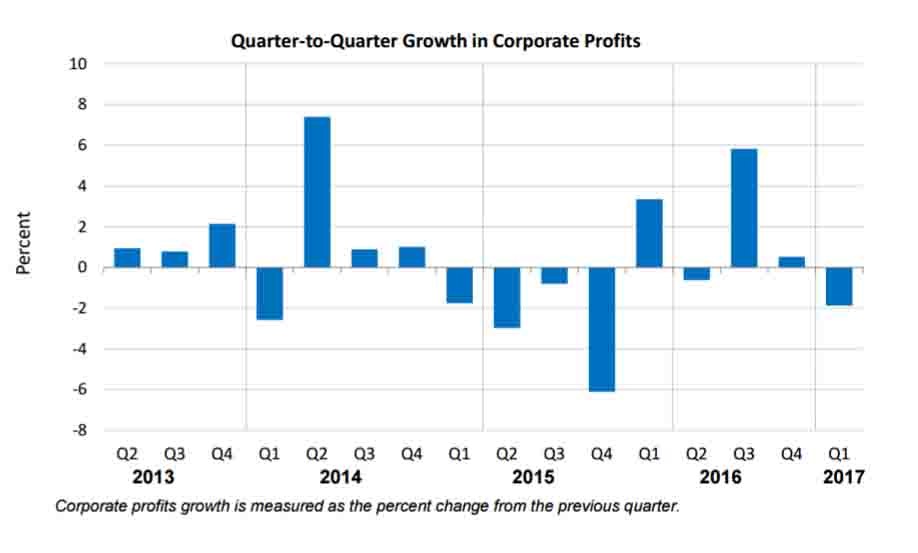

Another interesting part of the Q1 GDP report is that corporate profits decreased on a quarter over quarter basis by 1.9% as you can see in the chart below. This is in sharp contrast to the double digit bottom up growth estimates provided by S&P Dow Jones Indices and FactSet. The main reason for the difference is because of heightened legal expenses which corporations count as one time charges. With the all-out assault that global governments have been waging on global banks, it’s almost as if this charge shouldn’t be considered a one-time expense. Deutsche Bank had a $3.1 billion fine against it and Credit Suisse was dealt a $2.48 billion fine. I think legal expenses rightfully are excluded from earnings. That being said, usually at the end of the business cycle financial regulations are cut and fines are limited. Imagine how high the fines will get in the next recession, especially if the recession is blamed on the banks.

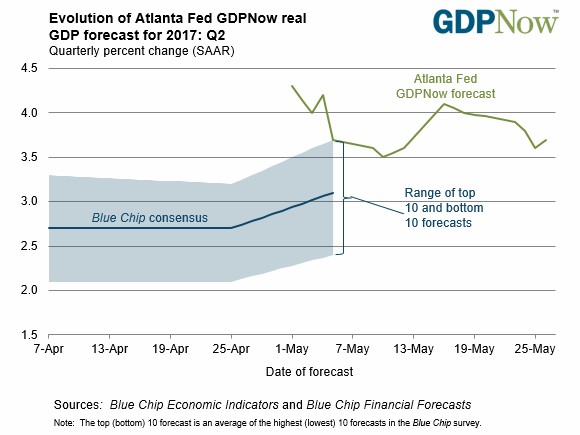

As I said, the estimates for Q2 growth are coming down just as the Q1 estimate was revised higher, making it a wash. To get to 2% GDP growth for the first half, Q2 GDP growth needs to be 2.8%. The likelihood of that occurring declined on Friday. The NY Fed’s GDP Nowcast dropped one tenth of one percent to 2.2%. This week’s data gave the estimate a boost via the wholesale inventories report. There was a negative impact from the advanced durable goods report and the new home sales report. As you can see from the chart below, the GDP Now forecast fell from 4.1% to 3.7%. The GDP Now estimate was lowered because of housing reports from the Census Bureau and the existing homes sales report. The estimate for real residential investment growth fell from 8.3% to 3.1%.

Another bad economic report for April was the core durable goods new orders report. It fell 0.4% month over month even though it was expected to rise 0.4%. Headline durable goods orders fell 0.7% month over month and were unchanged for the year. I don’t understand why the estimates for Q2 GDP growth are at about 3% given these bad results. I think we know that April was a bad month for the economy at this point. The numbers for May are sparse and obviously June hasn’t happened yet. There’s no way to make an accurate estimate for what GDP growth will be with such uncertainty for how the quarter is going. Anyone who says Q2 GDP growth will be above 3% isn’t thinking clearly. Taking estimates at face value is a fool’s game.

The bond market clearly is on the side of the bears as the ten year bond minus the two year bond is approaching the levels seen in Q1 2016 when there was a recession scare. Traditionally the yield curve inverts before recessions. The recent decrease in the spread is a warning sign to investors. If the yield spread falls below the Q3 2016 bottom, I will say with a high level of conviction that the stock market will not be within 5% of the all-time high. The question is when the declining spread will start to impact stocks. I think the spread may fall when the Fed hikes rates in June.

Conclusion

Q1 GDP growth was better than expected, but still was weak. Q2 estimates fell because of weak data. I’m surprised investment banks still think GDP will grow at 3%. I’m in no position to project where it will be. What I can say is if May is as bad as April, 3% growth is unlikely. The risk of a stock market correction will elevate if the yield curve flattens a little bit more.

1 Comment

Zac

May 30, 2017Nice Work, it is nice to get different information than the MACD!