The stock market closed flat on Monday. The big movement was in the VIX which closed down 7.57% to 9.77. It makes sense that the VIX is near its all-time low given the lack of volatility. The VIX being below 10 is very rare territory. The close today was the lowest since 1993. Volatility is like a slinky. The slinky has been compressed together as far as it can go. It likely won’t go much lower, if historical precedent is maintained. This means the stock market will likely move lower. Even with earnings improving, 5% mini corrections haven’t been eliminated.

In my last article, I mentioned that full employment wouldn’t cause a severe recession like the one in 2008 and like the next one we will see. However, wage inflation does cause margin compression. It makes sense margins are near the cycle peak because although unemployment is low, the hourly wage growth has been stuck below 3%.

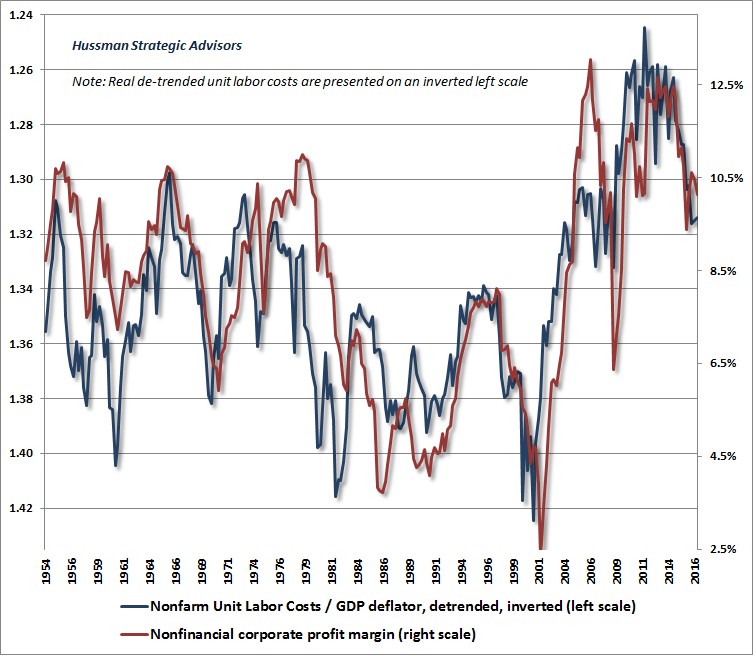

The chart below shows the highly-correlated relationship between corporate profit margins and the unit labor cost divided by the GDP deflator. The GDP deflator is the inflation rate used in the calculation of GDP. The blue line in the chart below shows how fast labor costs are growing in relation to general inflation. When labor costs increase faster than inflation the line goes down because it’s inverted. As you can see, lately labor costs haven’t been increasing quickly which has allowed margins to increase. The chart doesn’t include the latest quarter which isn’t finished yet. As I said in the last article, profit margins mean revert; increased labor costs could catalyze that decline.

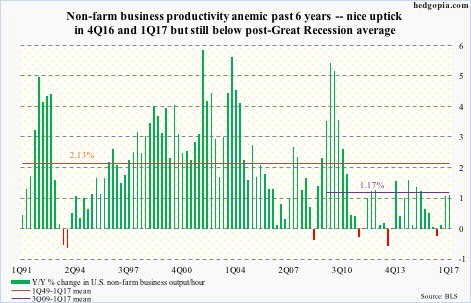

Rising labor costs would be a big problem for firms because business productivity has been anemic. As you can see in the chart below, the non-farm business output per hour growth has averaged 1.17% since the financial crisis. This is about half the rate of growth since 1949. If employees aren’t increasing their output, when they command higher wages because the labor market is tight, businesses won’t be able to hire new employees.

Besides the VIX, the other market I’m focused on is the long maturity bond market. There are two factors pushing the bond market in opposite directions. The first is economic weakness which is seen in the 0.7% GDP growth rate. The second is the increase in selling pressure which will come from the Fed and the Treasury.

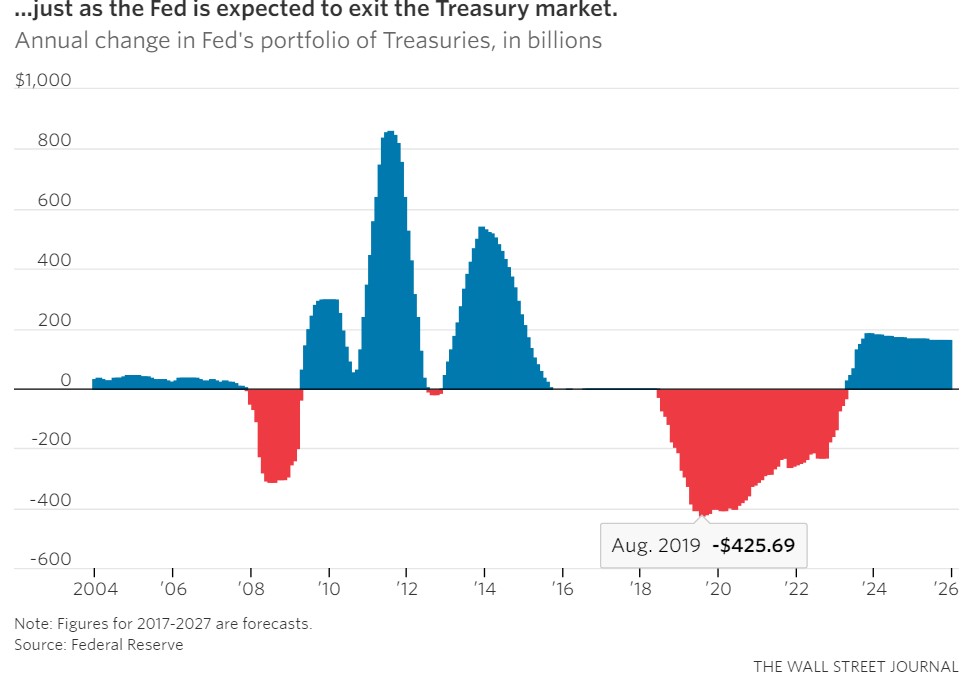

The timing of the Fed’s unwind of its balance sheet will be critical. The chart below provides an estimate for the unwind policy. It’s the Wall Street Journal’s best guess on the timing based on the Fed’s statements. The consensus is it will start in late-2017 in small increments and pick up in 2018. The next Fed meeting in early June will likely give the details to the plan making it the most important Fed meeting in years. The March, June, September, and December meetings are associated with a summary of the Fed’s economic projections and a press conference by Fed chair Yellen. It’s unusual to see the Fed about to embark on a new policy plan right before a new Fed chair is about to be named. This would be like if President Obama enacted a new tax policy during his lame duck session. Janet Yellen is a lame duck. This may have been why President Trump mentioned his support of Yellen recently. Maybe he didn’t want her to alter policy objectives because her term is almost up.

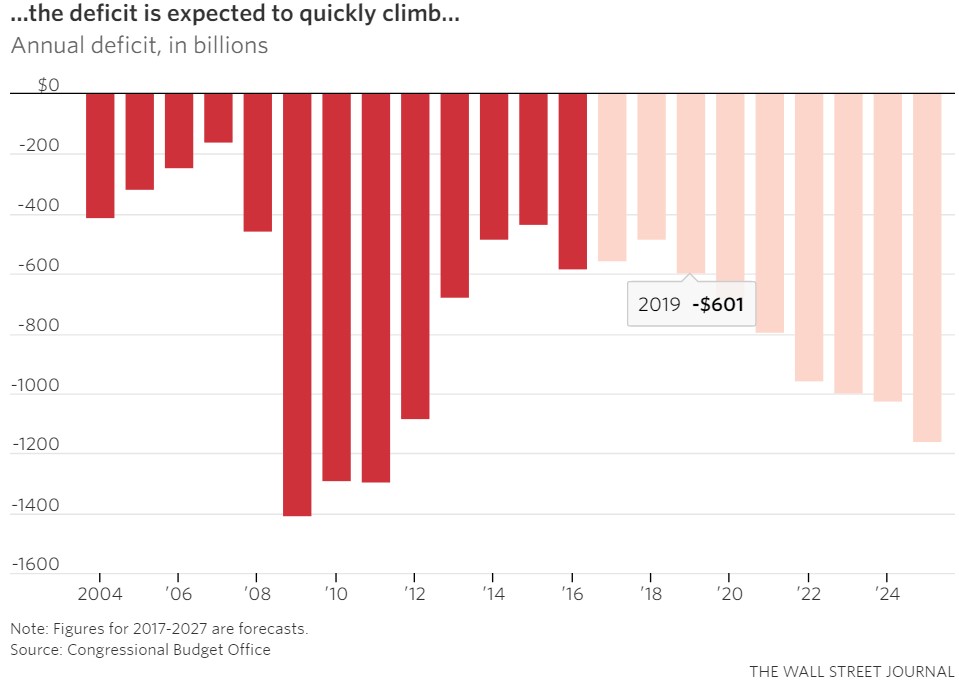

The possibility of Yellen not remaining the Fed chair is the first part of the confusion regarding monetary policy. The second is the rising deficits. Even if there isn’t a recession or spiking interest rates, the deficits will rise in the next few years because of entitlement spending. If the fiscal policy proposal involves tax cuts which aren’t paid for by a border tax, the deficits will be higher. It’s illogical that after years of keeping the same balance sheet, the Fed would decide to unwind just as deficits rise. There may be an inkling of logic to Trump picking Yellen to serve as Fed chairperson again because he wants consistency with policy and low interest rates. However, that logic breaks down when reviewing the unwind of the balance sheet, because he’d want a stable balance sheet while deficits increase to avoid flooding the treasury market. Trump also wants a chairperson who is in favor of deregulating the banks.

This makes the Fed pick even more confusing than before. Trump has given his guidance that he wants a Fed chairperson who is for deregulation and low interest rates, but what would the chair’s perspective on the unwind be? I would handicap this situation by saying there’s a 75% chance the new Fed chair will do the unwind slower if the fiscal policy calls for higher deficits. Considering that Trump doesn’t have a direct role in crafting the new tax and healthcare plans, it makes sense to be patient. If the Congress comes up with a plan where the tax cuts are paid for by cuts in healthcare spending, he may be fine with unwinding the balance sheet. If the plan increases deficits, then he may want to hold off.

That reflects a pragmatic approach to monetary policy which seems consistent with his thinking because once he saw that deficits would increase, he changed his tune on interest rates. He went from claiming low rates cause a bubble during the campaign, to supporting them in his latest explanations of who he’d want as Fed chairperson.

Conclusion

The market hasn’t had a 5% correction this year as earnings are being powered by an increase in margins. Margins might fall in the future as we get closer to full employment and hourly earnings increase. To be clear, when I was describing how Goldman Sachs was wrong about wage inflation overheating and causing a recession in my last article, I was making the point that Goldman views a low inflation rate as proof that the labor market is tight. Clearly there’s still slack left. When the labor market runs out of slack, we’ll see pressure on margins.

President Trump will have a pragmatic approach to who he picks as Fed chair. I don’t think he will keep Yellen. It will be a chair who is in favor of a more dovish approach to the balance sheet if the deficits soar which seems likely given the lack of a boarder adjusted tax in his tax proposal. The CBO hasn’t scored the new healthcare bill, so I can’t comment on its effect on the budget.