In the last Q&A Yellen did, she mentioned that the FOMC members didn’t want to consider the unwinding of the Fed’s balance sheet to be a part of the hawkish policy of rate hikes because the Fed had no experience with unwinding its balance sheet. She said communicating policy on the unwind of the balance sheet to the market would be tough because of this lack of experience. The Fed proved her correct in its Minutes on Wednesday because it bungled its explanation of how and when it would unwind the $4.5 trillion balance sheet. This caused the S&P 500 to fall by about 1% from the peak in the afternoon to the close. The next Fed meeting is in early May, so the FOMC members should clarify the Fed’s position on the balance sheet in interviews with the media. If it doesn’t clarify what its policy is, it could spark a further sell off in equities.

The most confusing part of the unwind is the speed of it. To clarify, when the bonds it has purchased mature, the Fed reinvests the money into new ones. When the Fed discusses an unwind, it isn’t discussing selling the bonds; it is discussing slowing or stopping the reinvestment into new bonds. Technically, even stopping the purchases abruptly would be a slow unwind because the bonds have varying maturities. The Fed mentioned at one point in the Minutes that it preferred to do a gradual slowing of the purchases which is what the market was expecting. It’s logical for the market to expect a gradual pace given the slow speed the Fed has raised rates at.

However, in the Minutes, the Fed also discussed ending the repurchases all at once because it would be easier to communicate to the marketplace and because it would shrink the balance sheet quicker. Shrinking the purchases at a gradual speed wouldn’t necessarily be tough to communicate, but if the Fed plans to alter the speed of the reductions according to the economic data, it will be tough. The Fed plans to provide details to the market on the speed of the purchases well in advance of when they occur. The Fed likely can’t simultaneously provide lead time for its unwind and be data dependent. Whether it can do so depends on the specifics of how much lead time is provided. If the lead time is a month, the data can change between when the plan is announced and when it is executed. If the lead time is one week, then the data wouldn’t be updated in between when the plan is announced and when it is executed. Traders will be front running these decisions in both cases.

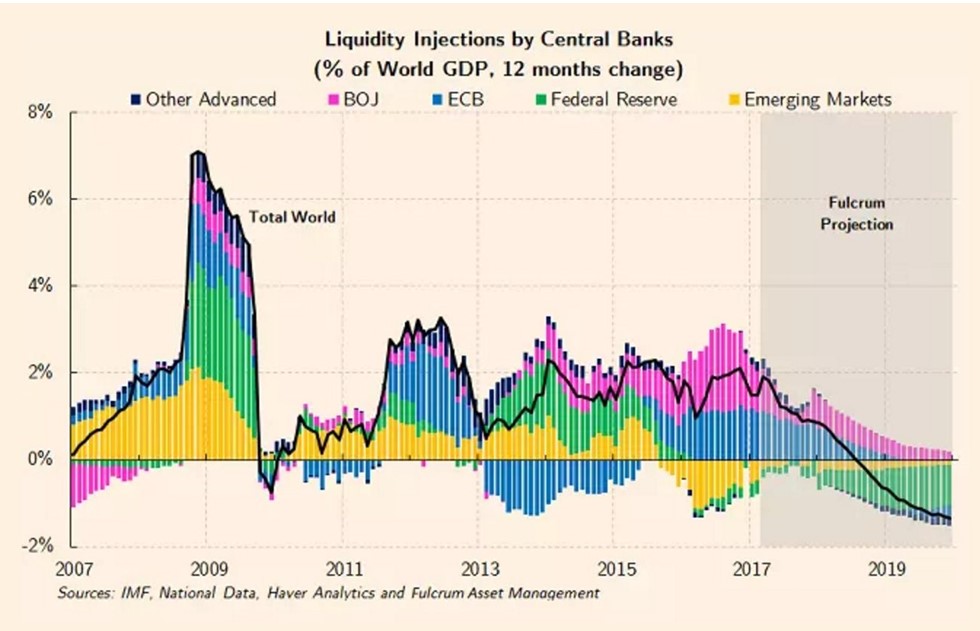

The Fed stated that most officials favored starting the unwind by the end of this year. This is a change in the guidance from how I interpreted it. Originally, the Fed was leaning towards starting the unwind at the end of the year, but as I mentioned in the introduction, in Yellen’s last testimony she seemed to push the schedule back which is why I made the point that the Fed was guiding for an unwind to start in the middle of 2018. Keep in mind my opinion on the guidance is separate from my expectations of what the Fed will actually do. I still don’t see how the global central banks will get away with following the projections shown in the chart below.

Speaking of the global central banks, the ECB may decide to follow the Fed’s actions by unwinding its own balance sheet. Up until now, the ECB has suggested leaving the balance sheet steady. It would eventually become a smaller part of the economy if the economy grew while the balance sheet was stagnant. With the BOJ slowing its purchases and the Fed shrinking its balance sheet, the ECB may decide to shrink its balance sheet to participate in the global currency wars. Once again, I’d like the emphasize the difference between guidance and policy changes. I expect volatility to occur between when these actions are announced and when they are executed. This may stop them from being executed.

The volatility I am expecting is a magnified version of what happened today. The Fed merely clumsily hinted at an unwind which was already expected and the market fell by 1%. As we get closer to the policy taking place I expect this selloff to occur. Since the specifics of the policy still aren’t worked out and the Fed is claiming it will give the market time before it goes through with the policy later this year, the details must be ironed out shortly.

One part of the plan the Fed agreed on was that it will unwind both the mortgage backed securities and the treasury bonds. Several members of the Fed now expect the fiscal policy to boost the economy in 2018 instead of late-2017. This was my original opinion from a few months ago, so I agree with this assessment. It’s interesting how the Fed didn’t change its perspective on rate hikes even though the fiscal stimulus has been delayed. It makes me question if the Fed decided to be hawkish because of fiscal policy in the first place. It may have continued its S&P 500 dependency and decided to raise rates because the market rallied.

Speaking of the market rally, several Fed officials viewed the equity prices as ‘quite high’ compared to traditional valuation metrics. This point is obvious, but the fact that it is being mentioned means some members of the Fed may view knocking down the stock market as an advantage to the hawkish policy instead of a negative. This cycle the Fed has treated the market gingerly. I just mentioned how the Fed may have only raised rates because the stock market allowed it to. If the Fed starts to change from coddling the market to wanting it to fall, it can knock the stock market down easily.

Interestingly, the ten-year bond yield fell after the Minutes were released. The ten-year yield fell about 4 basis points back to 2.335%. This is part of the ‘risk off’ trade. However, it is weird to see that the Fed increasing the supply of treasuries caused move investors to buy them.