In this article, I will tie up some loose ends from a previous article. I’ll give more supporting facts to further my points. Then I will contextualize the recent statements made by President Trump and NY Fed President Bill Dudley. I have an interesting chart which supports my analysis on the likelihood of various fiscal policy proposals being enacted.

Loose Ends

I have discussed the widening difference between success of large and small firms. The margins of small firms in the S&P 600 have been falling since 2013 while the margins of large firms in the S&P 500 are at cycle highs. I think this represents the late stages of this super cycle as financialization has spurred an increase in acquisitions instead of an increase in investment in new initiatives. If the large firms are picking the best of the small firms to acquire, it makes sense that their margins are up. It’s tough to for small firms to compete with large ones when the large ones can issue bonds at such low rates and their stocks are being bought by central banks like the Swiss central bank.

Furthermore, the increase in investing in indices like the S&P 500 instead of picking individual stocks helps the big companies who are able get into the index and hurts those who are left out. Having a large gap between those who make an index and those who don’t is not an efficient allocation of resources. Those in charge of picking companies to make certain indices have much more power than ever before. I am not suggesting they are abusing their power as there are objective requirements to get in to each one. I am merely stating the changes in requirements have become more important than ever before. It could even make sense in certain instances for a firm to hinder its long-term business interests to maintain membership in an index like the S&P 500.

The new point I am adding to this discussion is that the top 20 companies now account for 52.5% of the total S&P 500’s cash holdings. The top firms in each sector are doing better than ever, but there’s weakness among the smaller names. A lot of the cash the top 20 firms have is overseas which means the repatriation tax holiday is going to disproportionately help them. On the bright side for smaller firms, the regulation cuts will help them more than large firms because often small firms don’t have the budget to decipher new regulations to determine if they can change their business practices. If you don’t know what the law is regarding a new initiative, you simply don’t do it to avoid the legal risks.

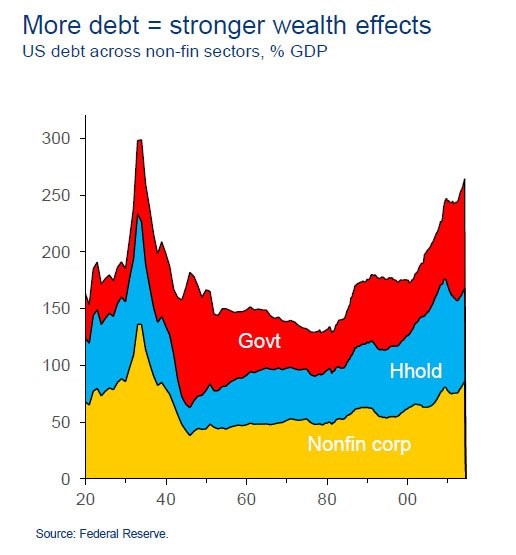

In my last article, I compared the current market to a combination of the 1929 market and the post-World War II era. That’s because the Shiller PE is about 3.5 points away from reaching the height seen in 1929 and the debt to GDP is near the World War II peak. The chart below gives more clarity to the debt comparison with the World War II era. When considering household, corporate, and government debt, the current debt as percentage of GDP comes close to the World War II era. It reinforces my point that the past two recessions didn’t do anything to deleverage the economy. A large deleveraging event will occur as the super cycle ends during the next recession which could start in the next few quarters.

I showed a chart in my last article which had the margin debt reaching a record high. This represents the peak speculation we are currently at. The chart below is a variation of that one as it puts the NYSE margin debt and S&P 500 in real terms. In these terms, the level of margin debt looks much worse because the previous two peaks were in the same ballpark while the current margin debt level blows them away.

Trump Trade

The President tweeted his displeasure with the House Freedom Caucus. He singled out Mark Meadows, Jim Jordan, and Raul Labrador. This signals the GOP’s divide is widening which means the fiscal policy boosts are less likely to occur. The fact that Trump mentioned that he needs the Freedom Caucus to pass tax reform is a preview of the coming battle which will cause more stock market volatility than the healthcare reform debate did. The reason I thought healthcare reform not passing was going to cause more volatility than it did is because I thought it signaled tax reform and infrastructure spending were less likely to occur. The stock market ignored the memo.

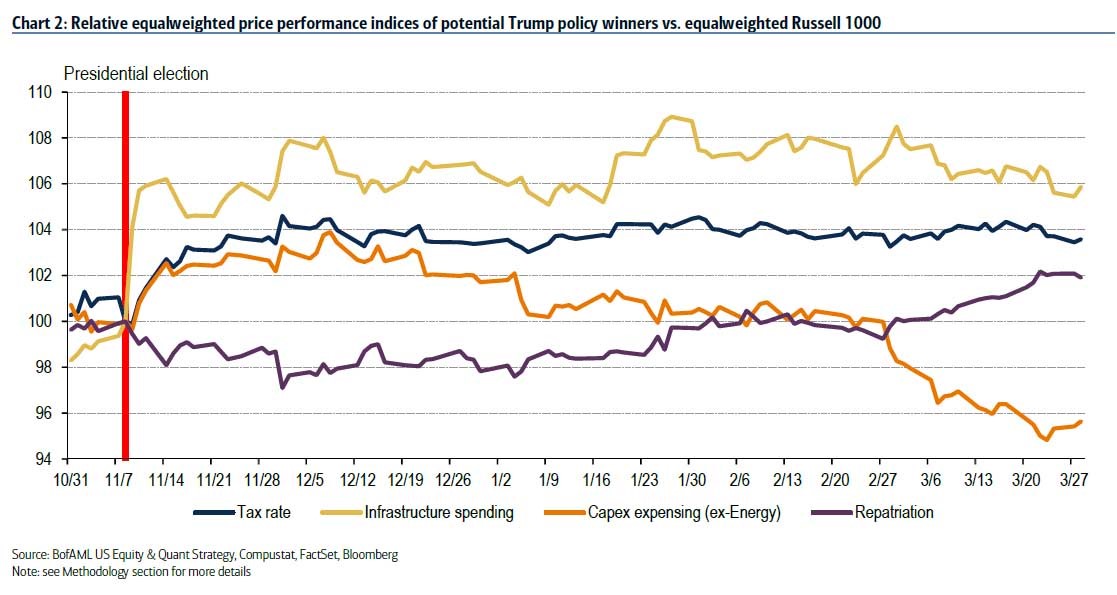

The chart below shows a few groups of stocks which will benefit from the various Trump policies. As I have mentioned previously, because of the budget constraints created by the lack of healthcare reform, the most likely policy to pack the most punch is the tax repatriation holiday. As you can see, the stocks which benefit from a repatriation holiday are the only ones which have rallied relative to the Russell 1000 in the past month.

Bill Dudley

In a speech at the University of Florida, NY Fed President Bill Dudley said “I don’t think we are removing the punch bowl, yet. We’re just adding a bit more fruit juice.” If you aren’t familiar with the punch bowl analogy, the economy is being compared to a party. The Fed’s rate cuts are the punch. When the Fed takes away the punch bowl, it is raising rates. The punch is the alcohol at the party which makes it more entertaining. The analogy is like the goldilocks scenario in that some alcohol makes a party fun, but too much causes trouble. When Dudley states the Fed is adding fruit juice, he means the Fed is making the punch less alcoholic. I interpret this statement as dovish because the Fed always has taken the punch bowl away after the economy grows for a few years. Even with the anticipated three rate hikes in 2017, Dudley is still afraid to say the Fed is taking away the punch bowl. This means the rate hike speed is going to remain slower than prior hike cycles.