While the major stock indices remain near their record highs and show no sign of having their first 5% correction in a few months, there has been changes to the underlying drivers of equities. The changes afoot are that fiscal policy must replace monetary policy in supporting the market and that earnings growth is going to have to replace multiple expansion in boosting stocks since interest rates may be rising.

The Fed chose, for now, to maintain its $4.5 trillion balance sheet, but it’s raising rates finally as we enter a more traditional tightening cycle. According to the Fed’s guidance, it will raise rates 75 basis points this year and next year. It expects to eventually get up to about 3% where it will maintain rates. The Fed has the unrealistic expectation that nothing will go wrong in this process as unemployment will stay at 4.7% indefinitely. The Fed wouldn’t need to meet if these expectations were realized.

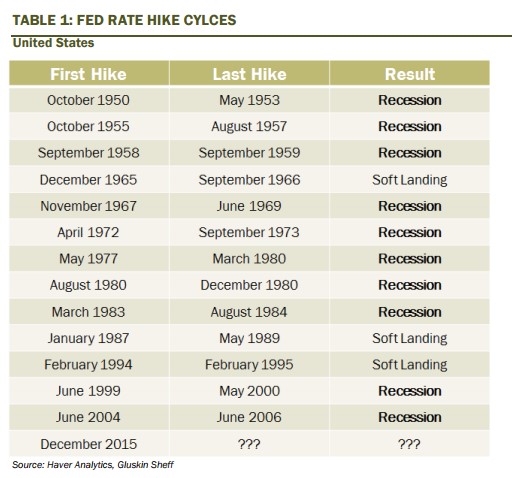

I say these expectations are unrealistic based on historical precedent. As you can see from the chart below, ten out of the past thirteen tightening cycles have led to recessions. The Fed is about one quarter of the way done with its hikes for this tightening cycle and economy is already very weak as the Atlanta Fed GDP model is expecting 0.9% growth in Q1. The Fed doesn’t want to start the next recession with the Fed Funds rate between 0.75% and 1.00% like it is now because it will have almost no wiggle room to cut rates to help stabilize the economy. The next recession, which the Fed doesn’t see coming, will be bigger than the previous two because of how low interest rates were kept for such a long period. The cuts won’t be able to help the economy and QE4 will need to be implemented.

As I said, unless you’re expecting stocks to live off hope forever, earnings must grow to bring stock prices higher, given the potential for higher interest rates. If the economy grows faster than expected, interest rates will rise which will crimp multiples. If the economy grows slower than expected, it will be tough for earnings to rise unless record high margins are achieved. The best- case scenario would be a Goldilocks one where the economy grows at about 3% in 2017 while interest rates don’t rise too fast.

Because the market is trading at a high multiple, earnings growth is more important than usual. Earnings estimates usually decline during the quarter. Estimates accelerate lower at the end of the quarter before reporting starts so firms can beat expectations when they report. This is the smoke and mirrors show Wall Street puts on to help boost the bull market higher. We’re approaching that time of the quarter where earnings estimates will start to dip sharply for Q1. The bottom-up estimate for Q1 S&P 500 earnings fell from $29.58 last week to $29.52. The bottom-up estimate for full year 2017 S&P 500 earnings fell from $131.28 to $131.11. This is a sharper decline than last week, but I would describe it as ‘par for the course’ instead of bad news because estimates usually fall.

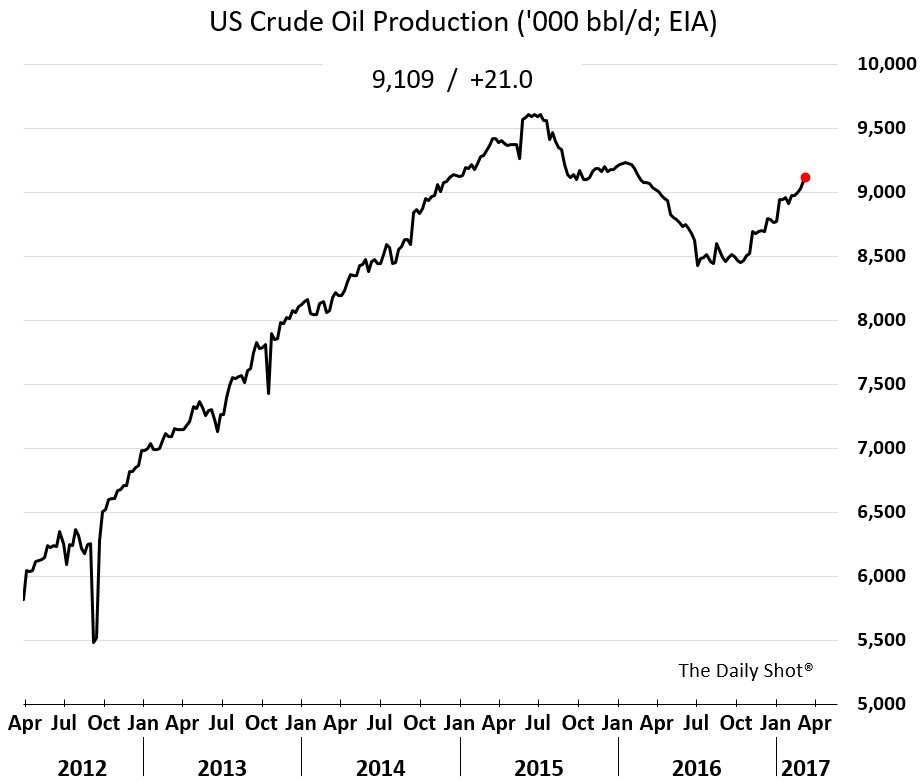

As of now, Q1 2017 earnings would grow 9.0%. That type of result is what would be needed to sustain the market. Energy earnings growth estimates for the full year fell from 312.2% growth last week to 310.1% growth. The more efficient fracking firms become, the lower oil prices go. The firms are hurting their profits by becoming more efficient. Individual firms must do this to compete since American shale firms are operating under a free market unlike the OPEC cartel. As you can see from the chart below, American free market shale production is thriving as about half of the decline in production due to falling oil prices has been erased.

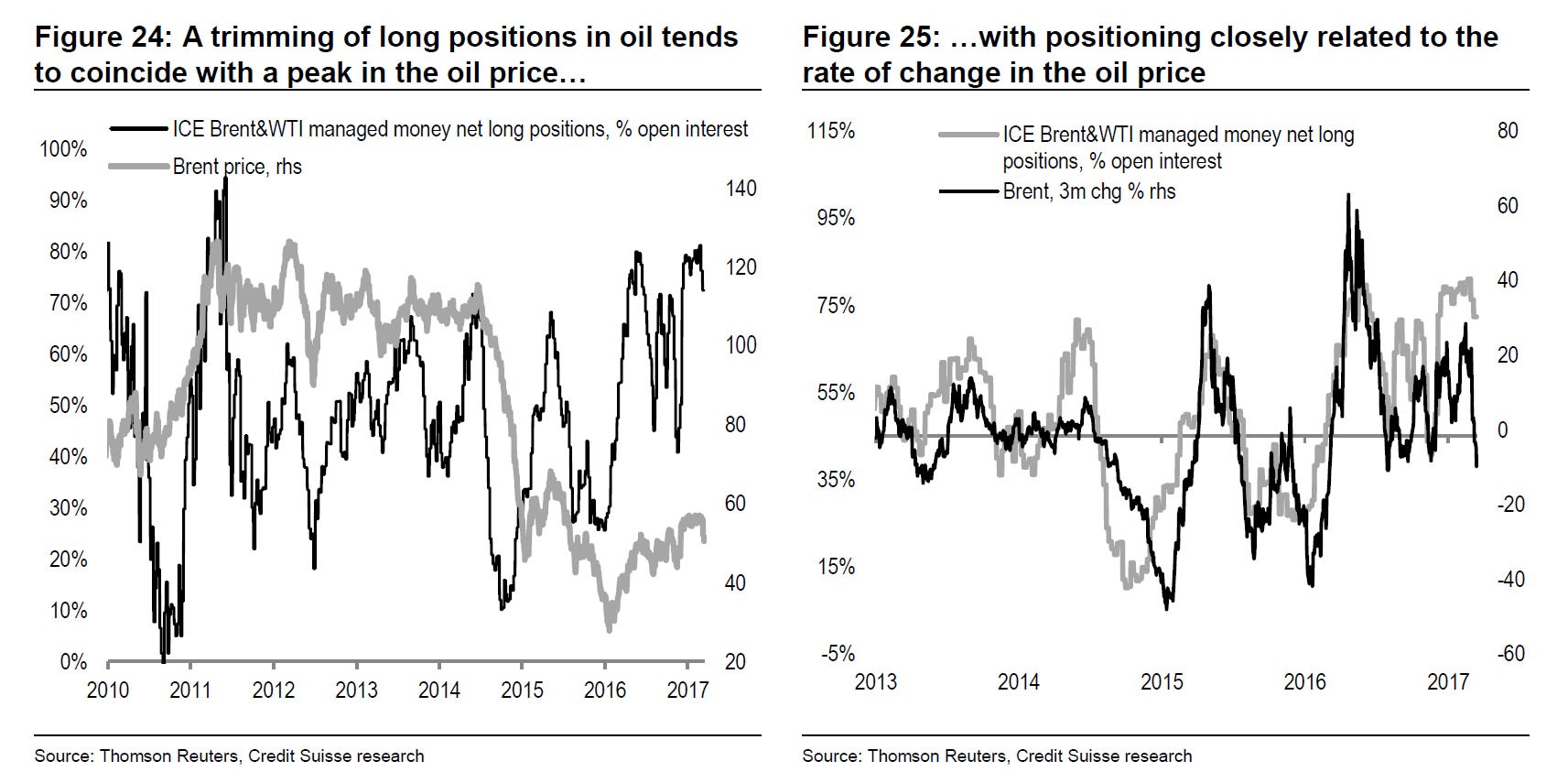

As you can see from the Credit Suisse chart on the left, long positions in oil have declined modestly. The reason why I was bearish on oil when it was in the mid-$50s was because of this high amount of long positions. It seemed obvious that oil prices would fall given the increase in production from shale and the high amount of these long positions. They are still historically high, meaning oil may fall further from the 48 handle it’s at now. The chart on the right shows the unsurprising fact that positioning affects oil prices.

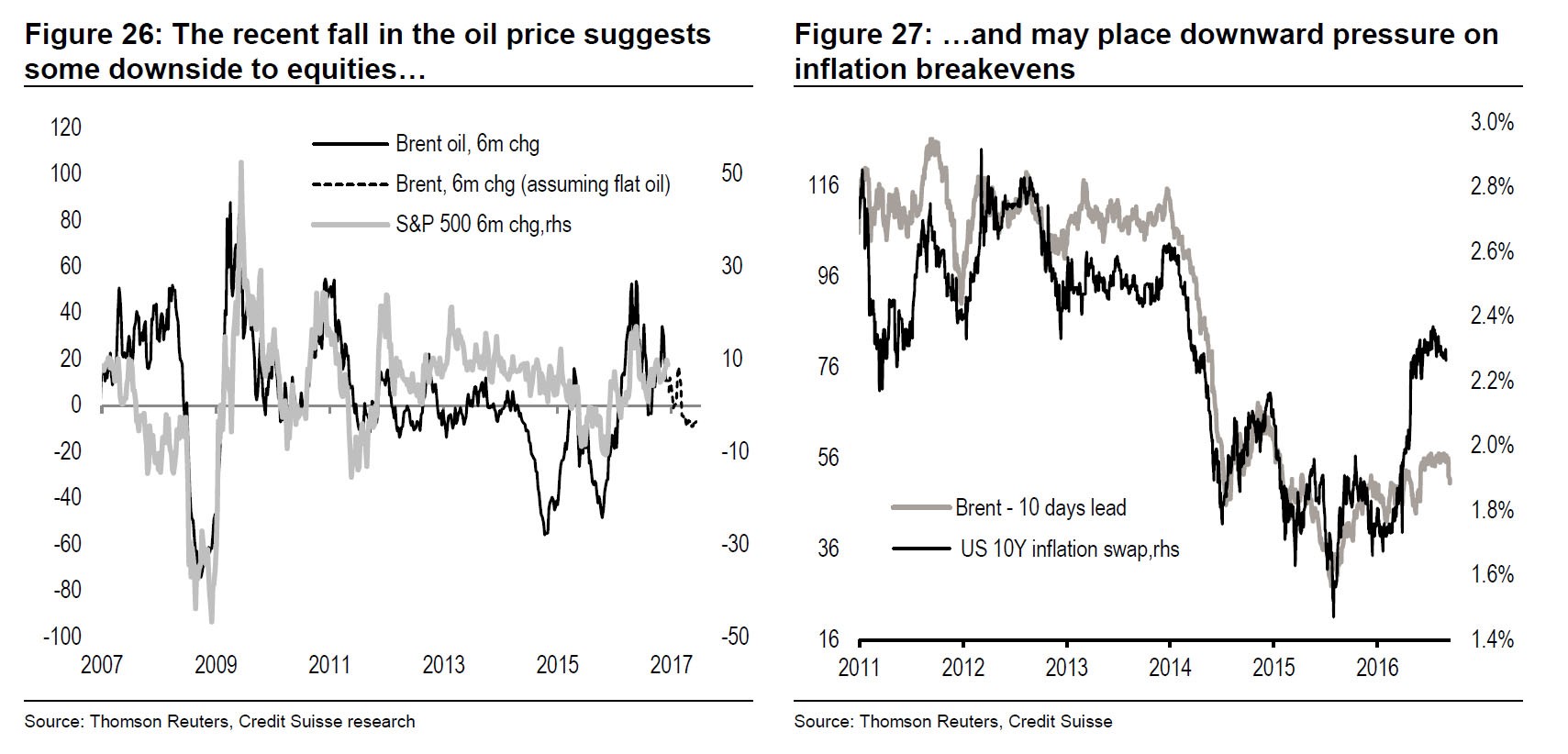

The chart on the left shows oil prices falling may hurt equities. I think it should hurt equities more than usual because S&P 500 earnings growth is relying on the energy sector more than usual. The chart on the right shows oil and the market based measure of inflation. Inflation has been driven by oil prices which is why I have said falling oil prices will make the Fed’s hawkishness seem like overkill. As you can see, the black line shows inflation was much higher in 2012, yet the Fed didn’t raise rates then.

Conclusion

The Fed may hike rates until something breaks like Jeffrey Gundlach suggests. Hiking rates in this moribund economy is like throwing stones in a glass house; everything will break. The market will rely on fiscal policy and earnings improvements to boost it higher. It will probably get the earnings growth it is looking for in Q1 as 9.0% year over year growth is expected. That’s still a weak growth rate when you look at the two-year stack because last year’s Q1 earnings fell, but it’s a step in the right direction. Oil prices will need to stabilize in the high $40s or move higher to maintain the energy sector’s highly positive impact on 2017 earnings estimates.

In my next article, I will discuss the latest on the fiscal policy front as it looks like the House of Representatives will vote on healthcare reform on Thursday. This is the first step in the process as the Senate will look at it next. It needs 216 votes in the House to pass.