Over the weekend, I was speaking with my cousin about a pawnshop he went to. He told me the owner told him that no one comes to the store to pawn items anymore. The owner said he should turn the store into a regular retailer. That is a sign of the economic times. Pawning an item seems quite ridiculous in today’s world. That change in behavior is partially caused by the fact that you can sell any item on the internet easily, but more so because interest rates are low so it’s easy to a loan without having to pawn your favorite possession. Add the strong labor market into the mix and the idea of pawning an item for quick cash seems outlandish. In business and in finance, normal behavior can change quickly.

This information on pawnshops is anecdotal evidence. I feel anecdotes can be combined with rigorous statistical analysis when doing research. In 2000, there were article titles like the one seen below. The unemployment rate in October 2000 was 3.9%. It hit 6.3% in 2003 which likely caused pawnshop lending to increase once again.

In November of last year, there was a similar story where a pawnshop in Virginia closed, after being in business since 1933, because of strength in the labor market. The owner stated “there are just not enough people coming in here to pay the bills.” My point is pawnshop lending weakness can act as a signal of a top in the labor market.

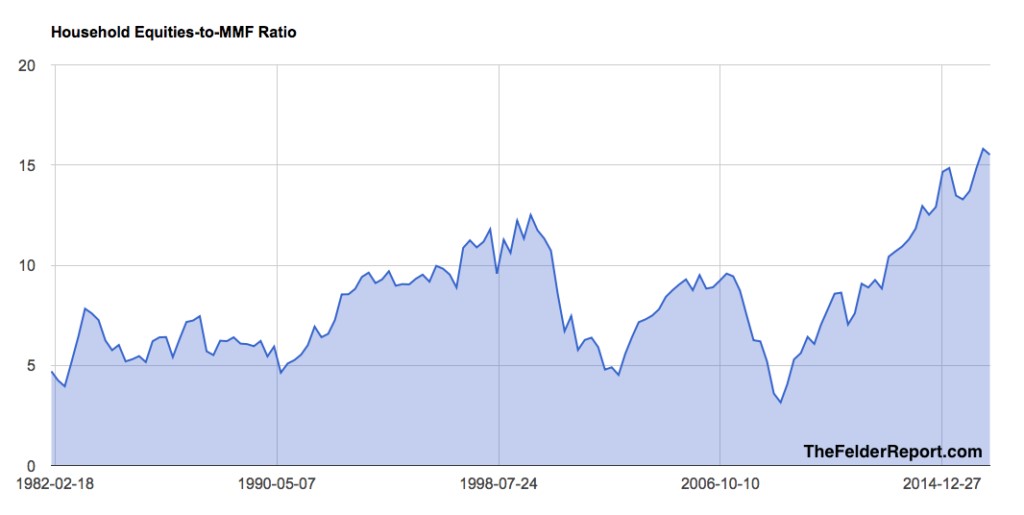

Another behavior which seems normal to us now, which wasn’t always the case, is keeping a high percentage of your assets in stocks. As you can see in the chart below, the ratio of household equities to money market funds is much higher than at the top of the previous two bubbles. Everyone is in stocks. It’s a catch-22 scenario. If you buy stocks, you own them when everyone and their grandmother owns them which means you’re late to the party. If you decide to keep your assets in money markets or bonds, you’re locking in low interest rates.

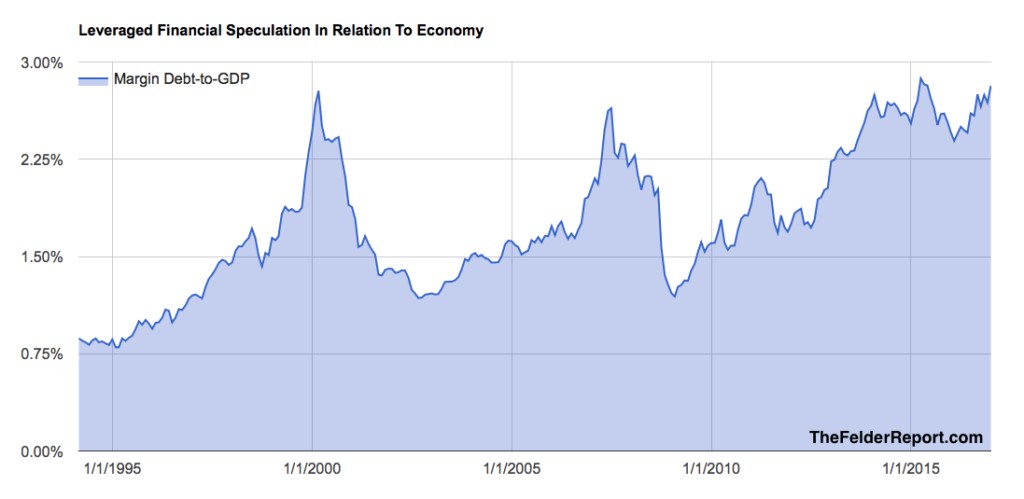

Investors who are piling into stocks do not see the benefit of wealth preservation. It’s easy to understand why someone would shirk the concept; having low returns is not an exciting prospect when you’re saving to buy a house or retire. Because I cannot predict when stocks will crater, I can only say stocks will provide low returns over the long term. This makes some investors miss out on the benefits of being cautious. What they hear in their minds is me saying “stocks may provide low returns, so you should invest in something safe which will provide low returns.” However, they’re only focusing on the upside potential and not the downside. The reason why owning stocks in a low return scenario is bad is because of volatility risk. One group of people who are focusing on the upside and ignoring volatility risk is speculators. As you can see from the chart below, the level of leverage to GDP is near the previous two bubble peaks.

On a related note, in researching the Google Trends data for “payday loans” I noticed a decline in the number of times it was searched in the past three years which was probably caused by the Dodd-Frank regulations enforced by the Consumer Financial Protection Bureau. The goal of the regulations is to limit poor people’s use of payday loans to stop them from getting into debt situations which they can’t recover from. The Google searches for “payday loans” peaked in 2013. The increase from the recession to 2013 may have been caused by the income inequality created by QE which boosted stock prices, but didn’t help wages. I cannot say for sure where the search stats would be without the Dodd-Frank regulations. I am skeptical of the search trends for the terms “pawn shops” and “pawn” because of the TV shows associated with the topic.

My viewpoint on payday lenders is that they are responding to demand. It’s not the payday lenders’ or the pawn shops’ fault people are in economically desperate situations. The root of the problem is addressing hourly wage growth. This looks to be the framework for the Trump administration’s agenda in dealing with the CFPB. The administration wants to lower regulations to allow businesses to grow. This growth would boost job creation and hourly wages.

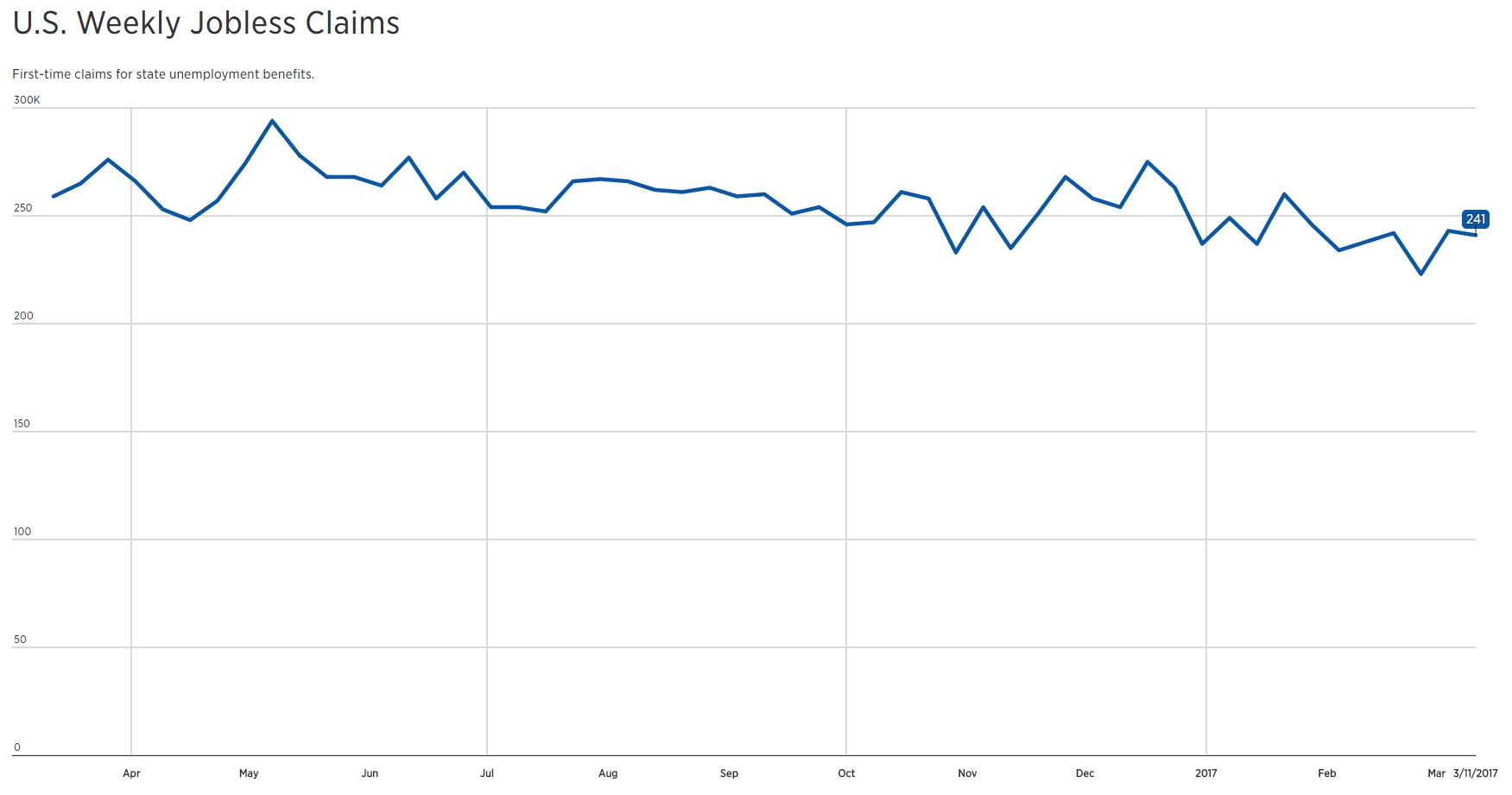

To contextualize this information on pawnshops, payday loans, and deregulation, let’s look at the latest jobless claims stats. As you can see in the chart below, jobless claims dipped 2,000 from last week. The 4-week moving average increased by 750 because of last week’s increase. The strong labor market would be in tune with the declining need for loans from pawnshops. The strong payday loan search growth in 2013 didn’t jive with the strong labor market. The latest decline in search volume since then may mainly be caused by regulations, but the latest blip higher in hourly earnings growth after a weak recovery, may play a part in the decline.

In past cycles, deregulation has come before recessions. It would be a mistake to use this as evidence that regulation cuts cause economic weakness. The reason the cycle works this way is because of changes in human psychology. After recessions, there is a political push to regulate industries which were involved in the crisis to prevent it from happening again. This is the wrong approach because recessions cannot be outlawed. After a few years of growth, people forget about the last crisis. They want to improve growth which starts to weaken at the end of the cycle. This leads to the slashing of the regulations made in the post-crisis period. Capitalism is praised when the economy is healthy and is rewarded with deregulation. Capitalism is demonized when the economy is weak and is punished with regulations.

Conclusion

Normal investors in today’s world would be described as speculators if you use historical context. That’s because low interest rates have made it normal to take more risk. It was normal to flip houses in the early 2000s. Soon afterward people realized how it was speculative to assume housing prices would always rise. When a strategy is popular, it makes it seem less risky, but that’s the exact time when it is the riskiest. Today’s consensus of buying index fund ETFs will look risky after poor returns are realized.