In this article, I will discuss the latest developments in European monetary policy and review an interesting chart which shows historical real labor unit costs, but first I will react to the breaking news about bitcoin which was released Friday afternoon.

Bitcoin ETF Denied

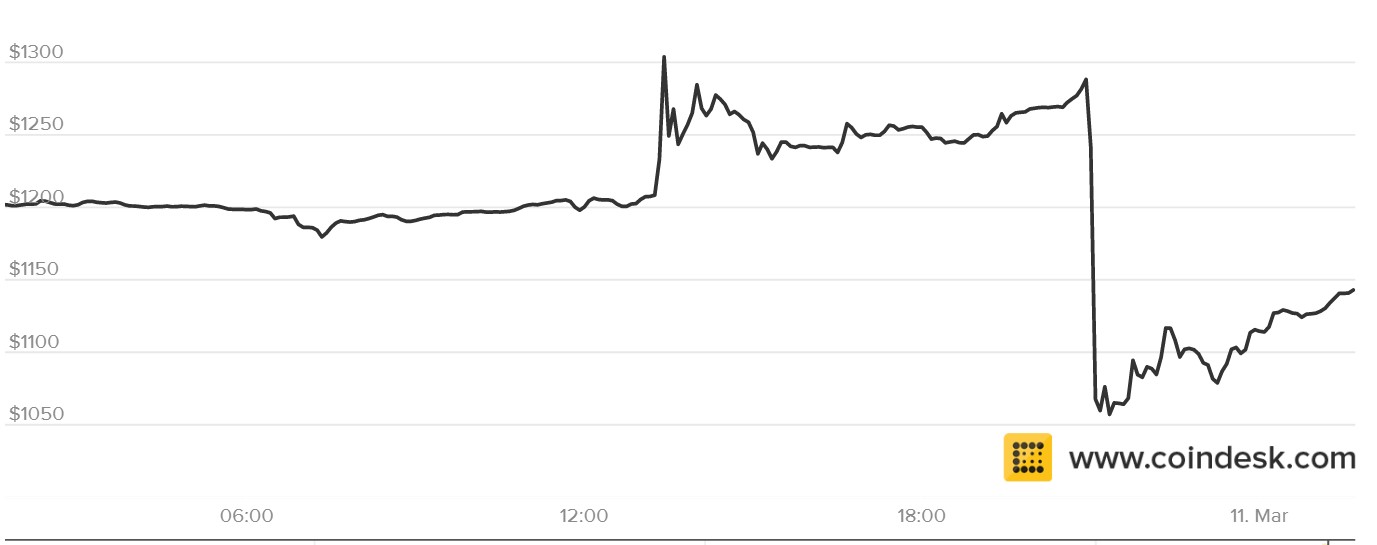

The, much heralded by the media, Winklevoss Bitcoin ETF was denied by the SEC. This caused the price of bitcoin to fall from $1,282.38 to $1,035.08 as you can see in the chart below. It has rebounded about $100 since then as the initial knee-jerk reaction has run its course. Prior to this decision, the betting odds had about a 50% chance of the ETF being accepted by the SEC. I had no idea whether it would be accepted or rejected by the SEC as I’m not knowledgeable on the specific regulations of ETFs.

The first point I will make is that the rejection of this ETF doesn’t mean anything for the long-term fundamentals of the currency. The ETF would have provided additional demand for bitcoin which is why the price ran up so high prior to the decision. I said that it was a bad idea to buy bitcoin when it was above $1,200. Now that it has corrected, you can resume regular purchases. The concept of a bitcoin ETF is a non-starter in my opinion because it removes what makes bitcoin great. It removes trustless transactions. The reason there is a gold ETF is because gold is a physical item which can’t be traded easily. Bitcoin was built online and is easy to trade. There is no need for an ETF. If a hedge fund manager has restrictions on what he/she can buy, he/she must get the restrictions changed. It’s easy for anyone else to buy bitcoin using Coinbase as a digital wallet and Trezor has a storage wallet.

Looking at the SEC’s decision, the government regulatory body cited risk of fraud and a lack of regulation in the world’s bitcoin markets. The Winklevoss twins underwent a three-year process to get this ETF approved. It seems like a lot of wasted effort to me. The SEC left the possibility for an ETF to be approved in the future if the currency develops further in terms of regulations and having “surveillance-sharing agreements with significant markets for trading the underlying commodity or derivatives on that commodity.” As a bitcoin proponent, I’d be willing to forego having an ETF to allow it to remain mostly unregulated.

ECB Raising Rates

Just like in the U.S., except at a later start, the E.U. is now discussing raising rates. It may start raising rates before the end of its Q.E. program. Thus, the German 10-year bund yield has risen from -0.946% on February 24th to -0.081%. That is the same day American bond yields had their near-term bottom. It makes you wonder which country is the dog and which is the tail being wagged.

The chance of an ECB rate hike in December 2017 is above 50%. It was only 10% at the start of March. The deposit rate is currently at -0.40%. Mario Draghi stated in a March press conference “There is no longer that sense of urgency in taking further actions while maintaining the accommodative monetary policy stance including the forward guidance.” BNP Paribas expects the ECB to raise rates by 10 basis points by September and to start ending the bond buying program early next year.

The trend has moved toward central bankers easing off the gas pedal as inflation has increased and growth is expected to get stronger by the end of the year and into next year. I had initially thought that Fed policymakers were being cautious by delaying their response to the GOP’s fiscal policies, but that’s no longer the case. The ECB doing another round of tapering or ending its bond buying program altogether along with raising rates could be a mistake if oil prices continue falling next week as energy is the principle cause of rising inflation. The ECB may be being pushed by the Fed to act because the Fed wants to raise rates without having the dollar increase too much. The ECB’s new hawkish tone may be why the 10-year U.S. bond has reached new heights while the dollar is $2.57 off its December high.

Real Unit Labor Cost Sky High

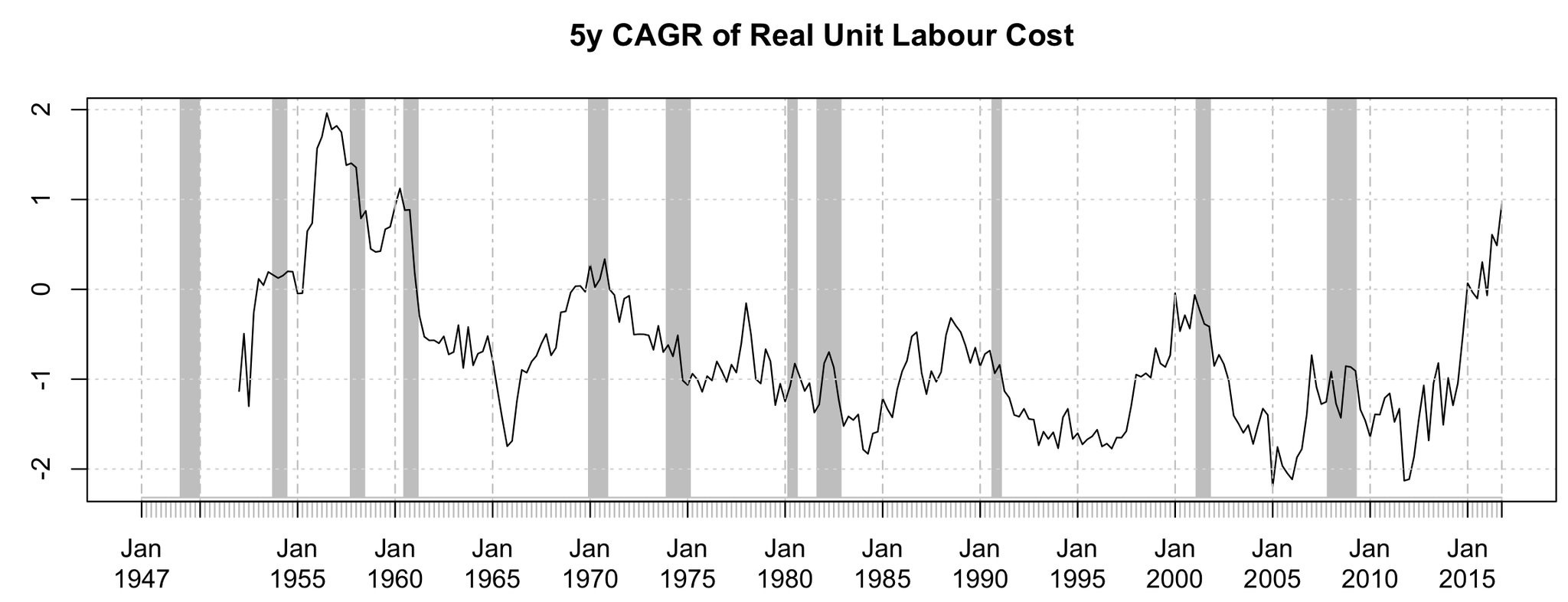

As I said in the introduction, I have a chart which shows the historical five-year compound annual growth rate of real unit labor cost. Unit labor cost is the average cost of labor per output. As you can see in the chart, real unit labor costs are in the 96th percentile. Real unit labor cost is wage growth minus productivity growth. The reason unit labor cost is so high is mainly because productivity is so low. If the Fed keeps rates low to try to eke out more wage growth, it will increase real unit labor cost even more which will hurt corporate profit margins. Declining profit margins is the only way for wages to increase, while having low productivity. This an alternative way of looking at why profit margins will not increase next year. The only hope for earnings to grow double digits in 2018 is for a tax cut. This is a long-term problem, so a tax cut will only delay the inevitable decline in profit margins by a year.

Conclusion

This article was a bit disjointed because I wanted to respond to the crash in bitcoin’s price due to the ETF being denied by the SEC. I consider the correction in bitcoin to be a buying opportunity. The ETF would have gotten more money into bitcoin, but it wouldn’t have improved its fundamentals. Real improvement comes from an expansion of the ecosystem and adoption by more users. If the price was pushed higher by hedge fund managers without these improvements, it could have been unhealthy for it in the long-term.

On another note, the ECB will be following the Fed’s footsteps and raising rates just as the catalyst for inflation’s increase starts to cool. Through the increases in the rig count, we are seeing that American shale firms are happy with $50 oil. This means $50 per barrel is a ceiling, which in turn means the E.U. inflation rate is about to become more subdued.

Finally, the high real unit labor cost could crimp near-record high profit margins that corporations are currently enjoying in the U.S.