In this article, I will review possible flaws in using valuation metrics and defend why they are important. I think some bullish investors make a critical error when they blindly discount valuations. There is a bias against valuations that tends to get built in over time when investors hear for years that stocks are overvalued years before any major correction occurs. Some investors don’t believe they can time the market, so they stay invested. While I think timing the market is tough, blindly buying an asset is a bad idea. This brings me to an important point that gets ignored. When stocks are slightly more expensive than average, it isn’t a big deal. It only matters when stocks are way more expensive than the average. Bullish investors tune out valuations because they here bears wrongly crying wolf when stocks are slightly overvalued; they assume it’s never a good idea to bother with valuations.

The happy medium is for the bears to avoid falling into the trap of being perma-bears. The solution for this is better timing on their part, which admittedly is tough. When I say the Shiller PE being over 27.6 is a signal stocks are extremely overvalued, that is an oversimplification of a complex determination. The best way to decide whether a specific valuation metric is worth heeding is to back test it. The difference in how you react to an overvalued market also depends on your goals. If you are very cautious, then avoiding stocks now is a no-brainer, in my opinion. As I have said previously, when you overpay for stocks you’re increasing the likelihood that you will receive subpar returns. A big determination of future returns depends on whether stocks correct to the median valuation or over-correct and become cheap. That’s impossible to predict.

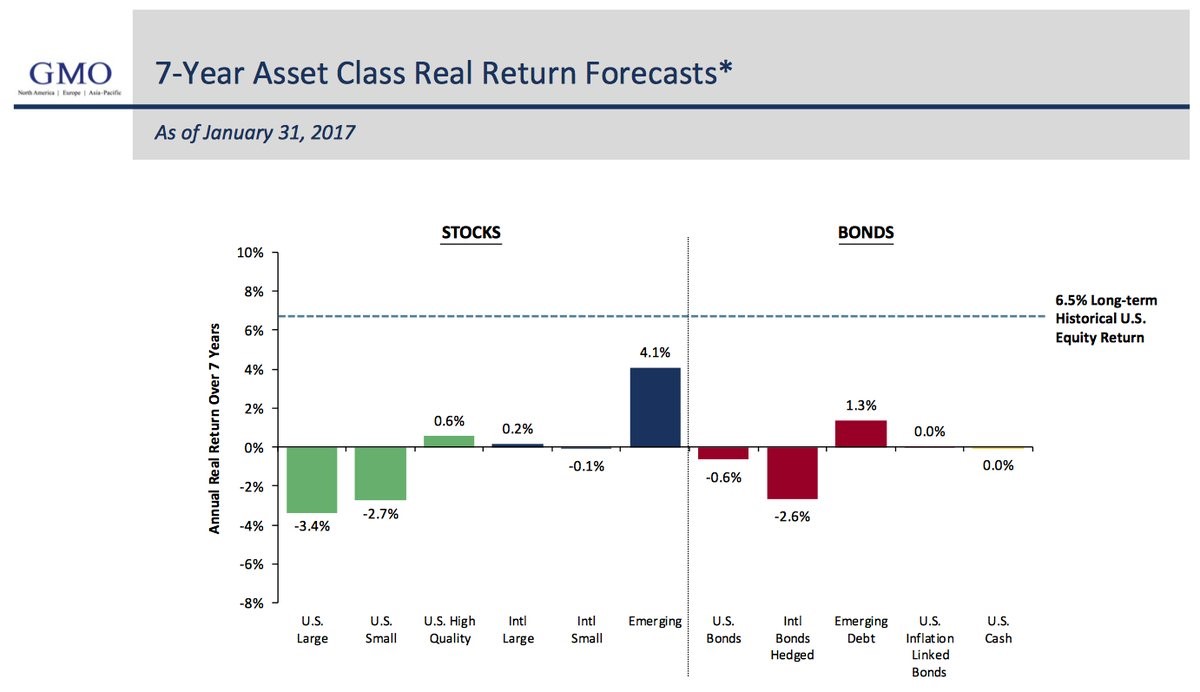

The chart below is the 7-year asset class real return forecasts by GMO. I agree with their forecast based on my analysis of valuations. Even if stocks don’t crash, I don’t see great returns over the next few years in U.S. small and large caps.

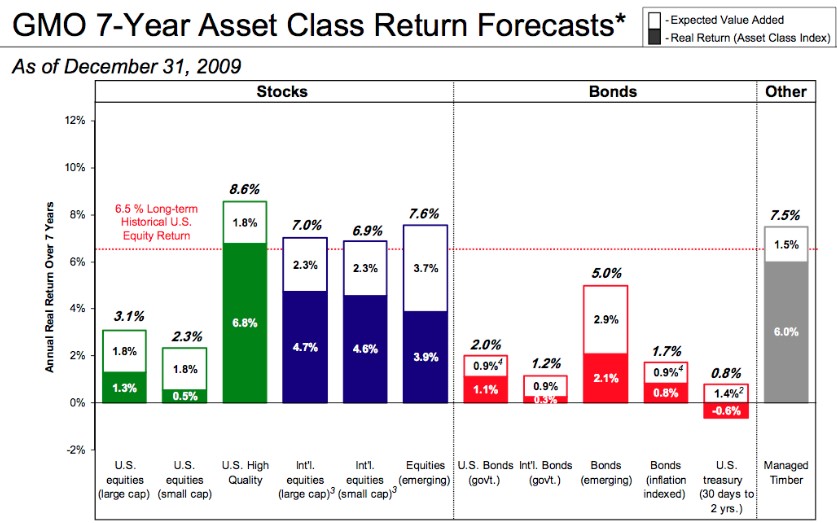

Since I am an intellectually honest bear, I will show the 7-year forecasts GMO made on December 31st 2009. As you can see from the chart below, GMO thought small caps would only return 2.3% per year and large caps would return 3.1% per year at the beginning of this massive bull market. Since it has been over 7 years since that projection, the results are in. Large caps rose 12.9% per year which makes it a 9.8% mistake. Small caps rose 14.2% per year which made it a ghastly 11.9% mistake. The Shiller PE on January 1st was 20.53. This is above the median of 16.09, but it’s not a sign of extreme overvaluation. If you only sold stocks when the PE was above 27.6, you would almost always hold stocks. That’s the way it should be. Recommending selling stocks is serious advice because it will likely mean investors will lose out on potential gains.

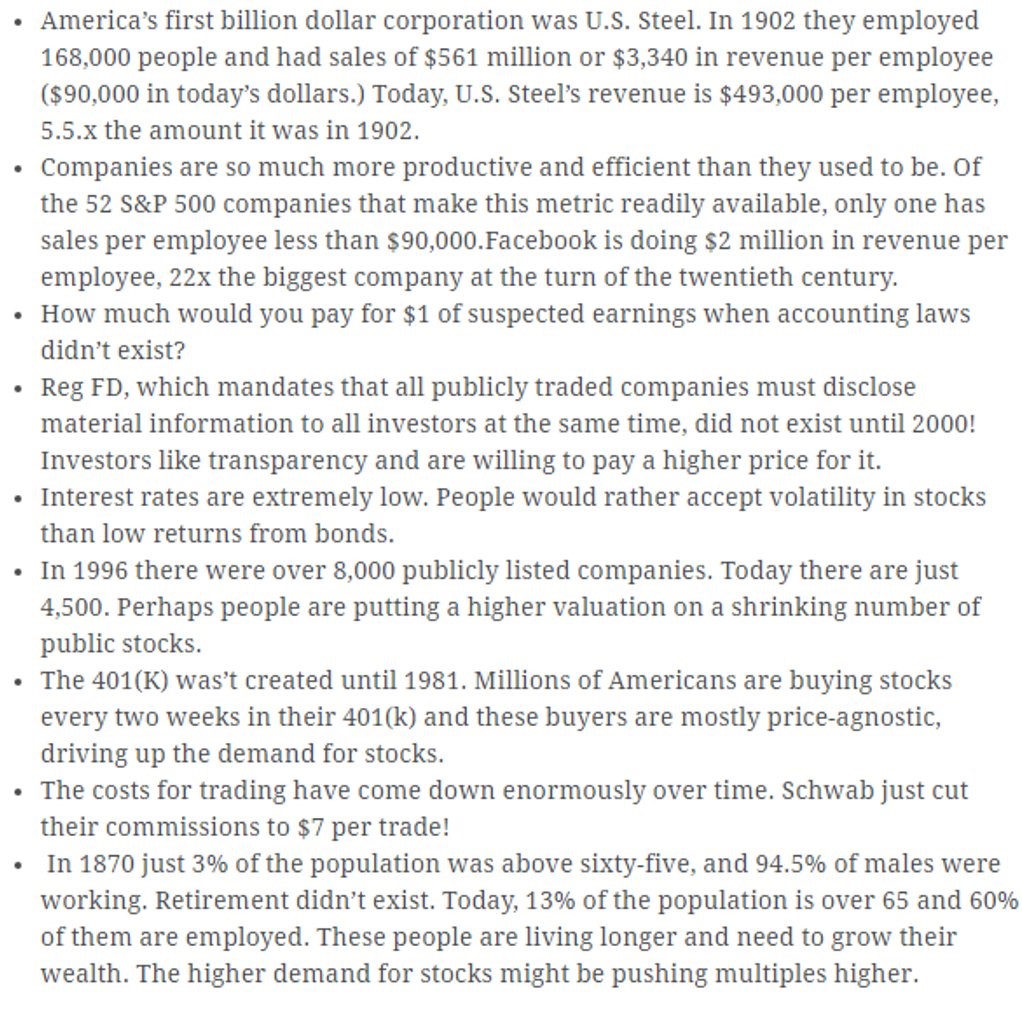

I will now finish responding to the bullet points which have the theme of telling investors to buy stocks despite high valuations. The third bullet point talks about how better accounting laws mean stocks should be valued at a premium. An obvious counterpoint to this is the CDOs which were off-balance sheet risks which brought down the financial system in 2008. The accounting laws cannot protect you from risk. Sometimes the laws aren’t followed and sometimes the laws are bad. In theory, better accounting is great because it shines more light on the business. However, more regulations don’t necessarily increase clarity.

The fourth bullet point deals with regulation FD which mandates all investors get material information at the same time. I think this is a bad thing as I am in favor of legalizing insider trading. Insider trading doesn’t hurt anyone. The one thing it does do is make asset prices more closely reflect reality. Without insider trading, there is a higher chance that the stock you are buying is not at the correct price based on all the information available. This increases risk because it subjects stocks to sharp movements once the news is announced.

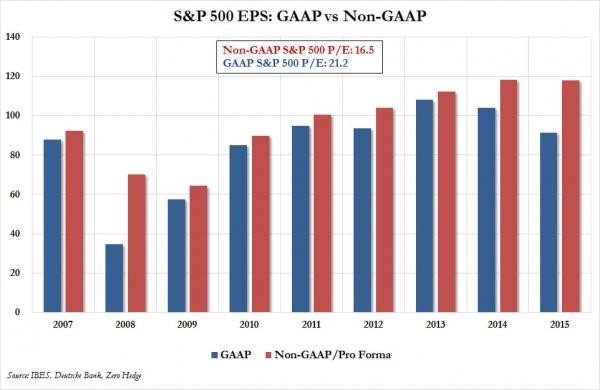

Another point worth mentioning is if accounting laws are so great, how come so many companies are using non-GAAP metrics to describe their earnings? The wedge between GAAP and non-GAAP earnings in 2015 increased to the highest amount since 2008. I am interested to see what the results for 2016 will be.

The next point is about interest rates. I acknowledge that stocks are expensive because interest rates are low. This is an explanation of the current market, not a prediction for future returns. If you were to tell me you’re expecting interest rates to stay low for the next few years, then I’d grant you the point that being bullish is an adequate response based solely on that information. However, this list doesn’t say that. Future investors in stocks won’t care what interest rates were at in early 2017.

The next point discusses how there are less stocks. I can make the argument that less stocks means there’s less competition which means businesses are run worse than ever. If Trump’s regulatory cuts open competition from small businesses, this may hurt the 4,500 public firms’ ability to maintain their lofty profit margins. The original argument is also factually misleading because there were way less stocks in the 1950s than now. Stocks had lower valuations in the 1950s than now.

The point about 401(k) investors is wrong because it doesn’t explain why stocks fell after the peak in 2000 due to over-valuation. Secondly, the passive investing trend is causing the equities bubble. When it reverses, these price-agnostic investors will suddenly panic because they will see the market falling quickly. Another term for passive investors who don’t care about risk until losses pile up is ‘stupid investors.’

The point about trading costs contradicts the previous point. The investors in this market aren’t making a lot of trades. They are passively buying an index fund without paying attention. Trading costs aren’t a factor for them.

The final point is wrong because while there is a need for wealth to fund retirement, it doesn’t exist! About half of American households have no retirement accounts. 29% of households age 55 and older have neither retirement savings nor a pension. The fact that millions of Americans need money for retirement and don’t have it sounds like a massive liability to me.

Conclusion

Just because some bears scream that the market is overvalued too early, doesn’t mean extreme valuations should be ignored. I think that avoiding stocks should be a rare strategy which occurs when stocks hit bubble levels. We are at those levels now. I rejected the arguments provided on why valuations don’t matter.

1 Comment

Harry

February 26, 2017Excellent reading, Thank you!