Every Friday FactSet releases the updated aggregate information on earnings. I will review the new data. It was a poor update, but clearly the market doesn’t care as it rallied to new all-time highs. The market hasn’t cared about earnings for this entire cycle. Amazon stock declined after having a disappointing earnings report, but it already made new highs again today. Microsoft stock also declined because of weak earnings and has recovered almost all its losses. Any bad news about a company just slows its trek higher. It is the same situation with the indices and economic reports. A bad report may send stocks lower for a day, but they always rebound. This is the reason the market hasn’t had a 5% correction in so long. If investors believe every time the market falls 5%, it’s a buying opportunity, then they think front running any small correction is a good strategy.

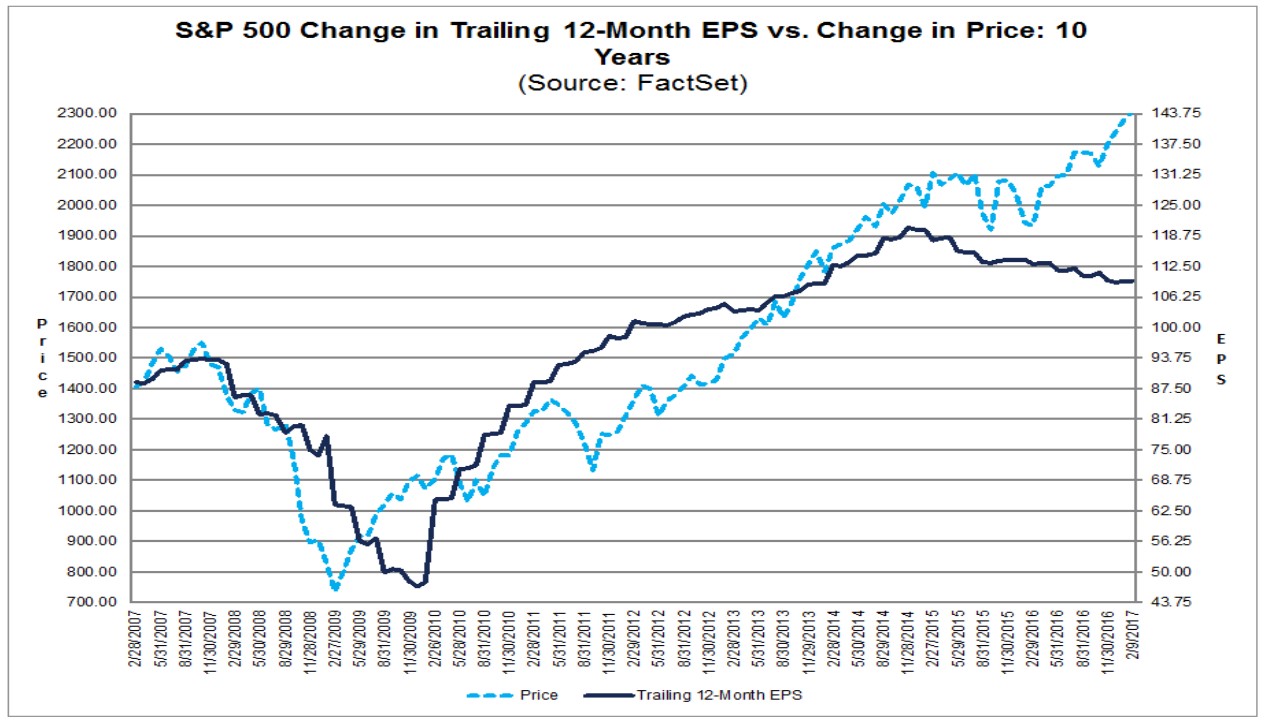

Today the market is acting unusually because the VIX is up 2.76% even though the S&P 500 is up 0.52%. Even with this gain in the VIX, it still has an 11 handle. My point about the market ignoring any bad news can be seen in the chart below. Trailing twelve month earnings fell which caused the market to flatline. Now that earnings are projected to go higher, the market has broken out of its range. Even if earnings do hit estimates causing the trailing twelve month EPS meets the previous highs, stocks are still overvalued because they have already rallied.

One of the biggest offenders in this market that only prices in good news and ignores bad news is Caterpillar. The chart below shows the trailing twelve month EPS compared with its stock price. The stock had sold off initially because of the manufacturing recession in 2014-2015, but now the stock has rebounded without earnings improvements. I’ve never seen a company cut guidance and have its stock march higher the way Caterpillar has.

Investors are now questioning how they value Caterpillar because it is a cyclical. The concept being promoted is that the stock shouldn’t fall that much during downturns because upturns are inevitable and Caterpillar is a stable company which will always survive downturns. I don’t believe in the argument that the stock shouldn’t go down when it does poorly. In theory, you can estimate peak and trough earnings to come up with a fair value for the stock, but as you can see in the chart, the stock has always fallen when its earnings falter. My guess is foreign central banks are buying Caterpillar stock since it’s a great American brand. They’re creating bubbles which will have messy bursts.

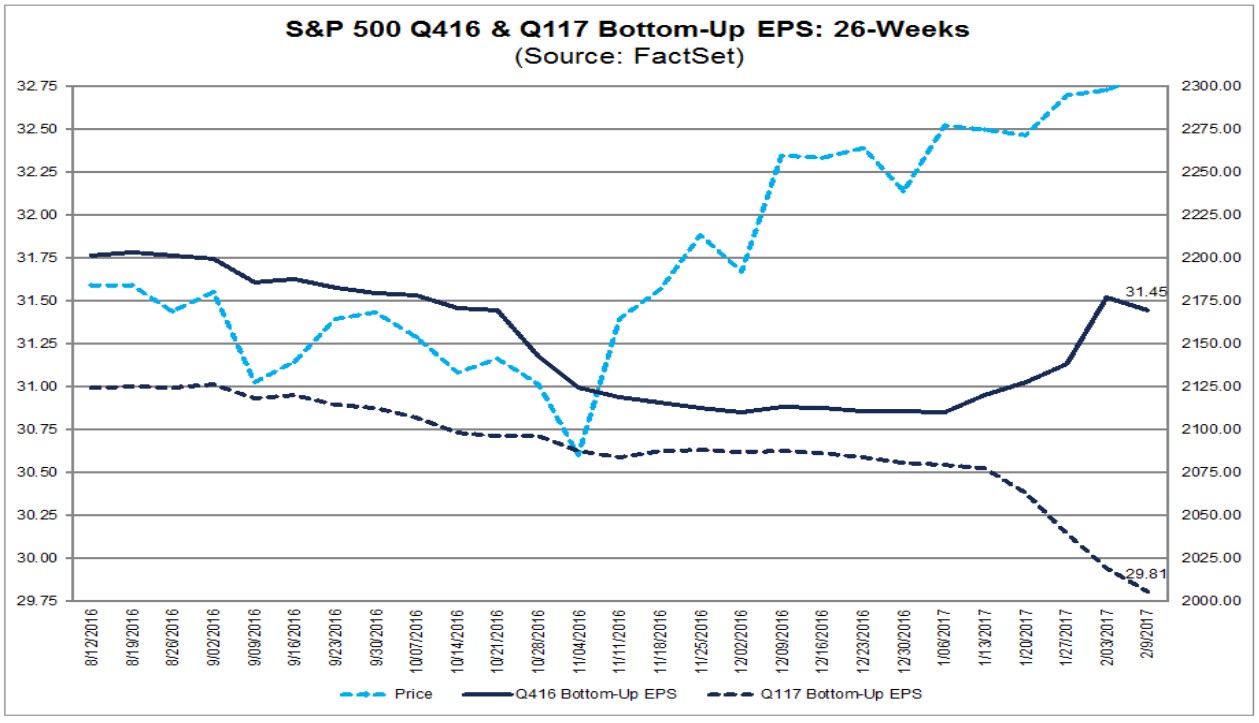

Getting to the updated metrics, the chart below shows the bottoms up EPS estimates for Q1. The Q4 metrics are a mixture of actual and estimated results. The S&P 500 price has literally rallied off the chart even as the Q1 estimates are falling fast. This has been a common occurrence in the past few years as earnings estimates never seem to come close to being met. This is the quickest way to get to a more expensive Shiller PE. It is now at 28.85 as economic miracles are being priced in to the market as if they are a sure bet.

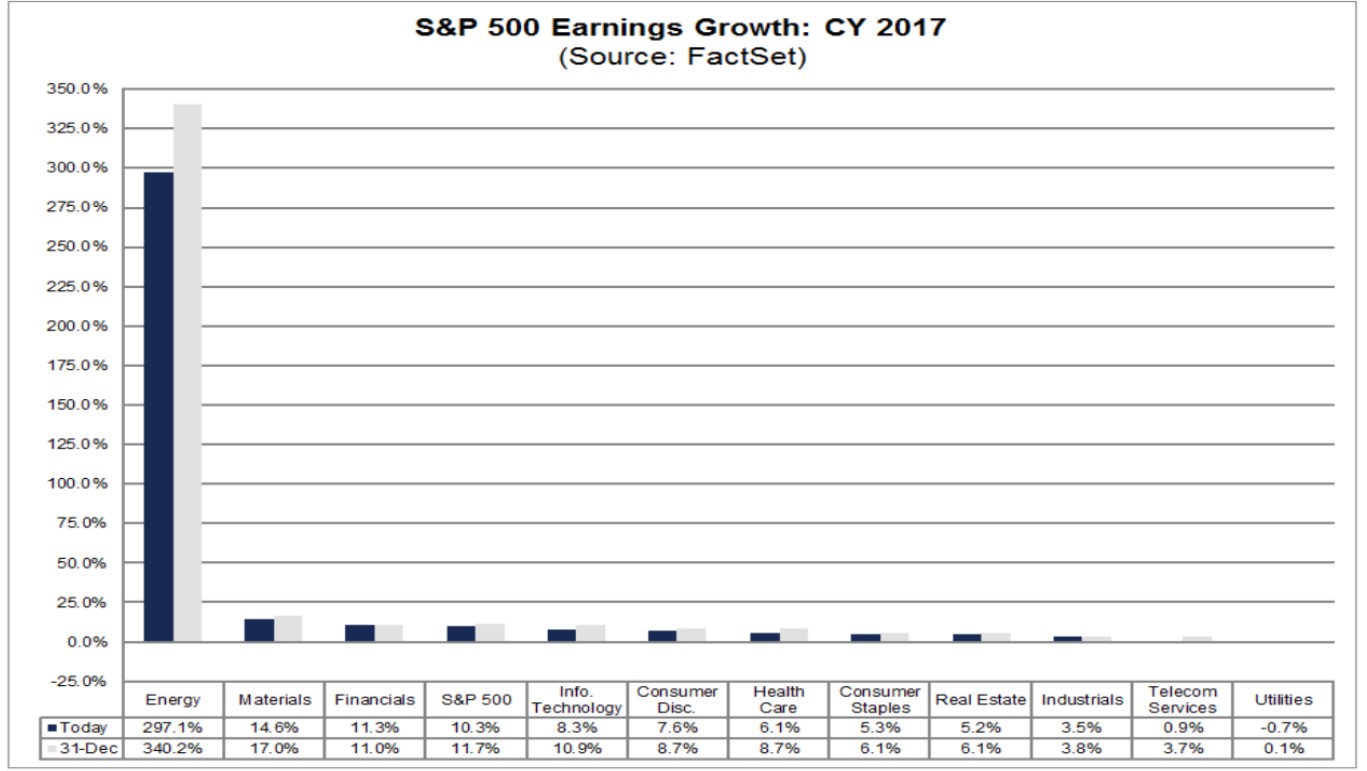

Partially as a result of the estimates for Q1 declining, the 2017 full year earnings estimates also fell. Last week estimates for 2017 were for 11.1% growth. Now full year earnings are only expected to grow 10.3%. Declines in information technology, consumer discretionary, health care, consumer staples, real estate, industrials, and telecom services caused this revision lower. It was a broad-based change in earnings expectations which would send the market lower if it cared about profits.

Energy earnings estimates improved by 3.1%. Today oil futures declined 1.8% because the US Energy Information Administration said US shale production is going to rise 80,000 barrels per day to 4.87 million. Oil drillers added the most rigs since 2012. There are now 591 rigs which is the most since October 2015. If this trend continues, it could lower earnings estimates which is what I’m expecting. I am fine with staying out of the market if total S&P 500 earnings growth is in the mid-single digits. I will stay true to investing based on valuations even if the market wants to ignore them.

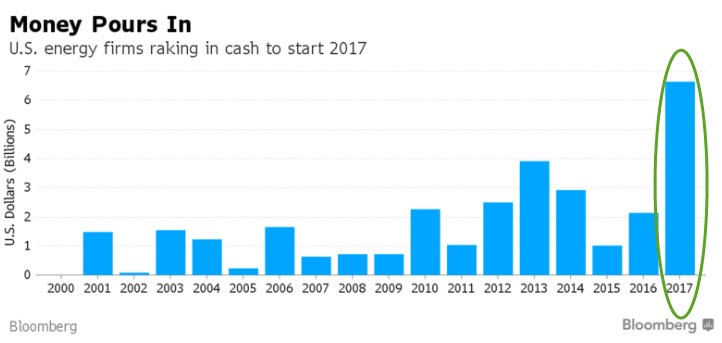

As I mentioned in my article last week, high yield energy and mining firms are receiving investor money as their bond yields are falling to pre-crash levels. It’s not a surprise that animal spirits would cause traders to buy energy debt even though oil prices haven’t rebounded fully as the market likes to front-run what is expected to occur. It also makes sense investors would flock to it in this market because high returns are so hard to find. It’s the same thing for energy stocks as many have rebounded significantly in anticipation of earnings growth which will come this year. It’s rare to find a firm with such high earnings growth outside of energy. This scenario is evidenced by the chart below. I think there’s risk that this excess money flowing into energy firms can be a mistake if oil prices correct lower given the high level of long speculation in the futures market.

Conclusion

Not surprisingly, the market didn’t fall even though earnings estimates for Q1 and full year 2017 fell. I think some investors who claim they are buying stocks because earnings growth is expected to rebound in 2017 are using that as an excuse. The stock market had a great 2016 while S&P 500 earnings only grew 0.5%. Part of the reason why bulls clung to increased earnings as a reason for buying stocks is because the Fed was expected to raise rates. Now that rate hikes have been put off, the animal spirits don’t need earnings growth. Trump’s regulatory cuts and tax cuts won’t affect earnings until 2018. That’s great for the bulls who will do mental math to conclude stocks should go higher. It’s tough for me to come up with a catalyst for a correction because previous economic reports and political events which I thought would cause one, haven’t done so.