It’s trouble in paradise for the GOP led Congress. Their reward for winning the contentious election last year is to deal with the problems with the U.S. tax code. Considering the convoluted nature of the system, it sounds more like a penalty, to me. On the campaign trail, it’s easy for politicians to claim they want to lower taxes, simplify the code, and cut wasteful spending, but acting on those promises is much tougher. The reason why I’m discussing this in terms of investments is because of two main reasons.

The first is that equities rallied after the election in the anticipation that pro-business measures would be implemented. If they aren’t implemented, the rally would have to reverse itself. I thought it was dangerous for stocks to assume a dysfunctional government would suddenly pass legislation efficiently. We are seeing this play out now as the tax code is like a Jenga game. If you alter a part of it, either it will have a tougher time getting passed or some constituency will be hurt. The logic of the market rallying because of a GOP president also seemed off because it’s not as if the market was doing poorly under a Democratic president. It not like stocks were being held back by the regulations in the past 8 years. I’m not saying regulatory cuts wouldn’t help growth. I am saying stocks were already over valued before the post-election rally.

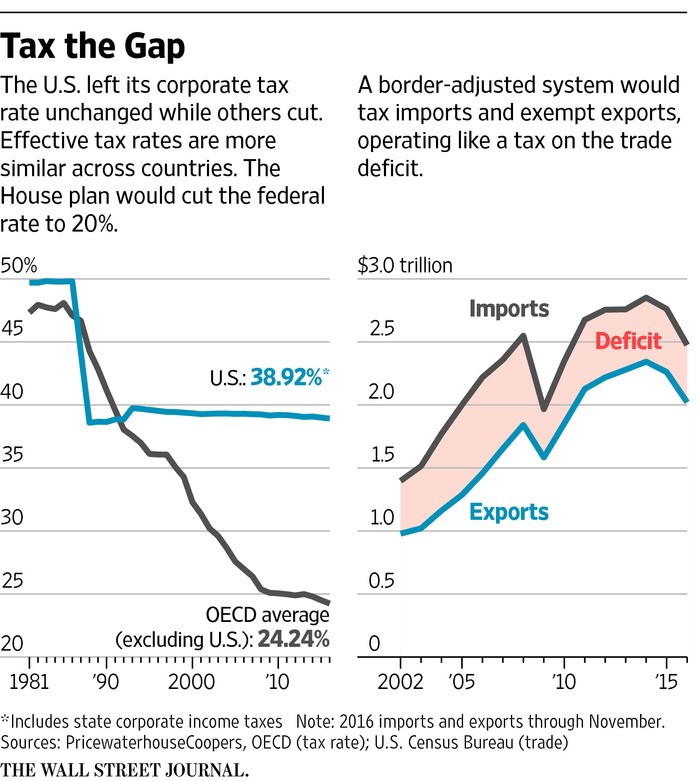

The second reason it is important for investors to stay focused on tax reform is because there is potentially a chance for some industries to be hurt and some industries to be helped by it. There is a possibility that the entire code is reformed. A tax cut is code for: some people will benefit and no one will get hurt. Tax reform is code for: some people will be helped and some people will be hurt, but the process will be simplified. The effective corporate tax rate is 39% when including state taxes. The tax rate can’t be cut to a globally competitive 15% rate unless a boarder adjusted tax is implemented. This is where the situation becomes messy.

The boarder adjusted tax or destination-based cash flow tax is a value added tax on imported goods. The current rate being proposed is 20%. The tax is based on where goods are consumed instead of where they are produced. The goals of the tax is to reduce the tax incentive to ship jobs overseas and to make up for the deficits the cuts in the corporate tax rate will bring. The tax supports products made in America, but hurts products made overseas. Because so many consumer goods are made overseas, this becomes a tax on consumers. The benefit consumers will be getting is the income tax is going to be lowered. Another factor to keep in mind is that the dollar is expected to rise because of this tax. The strong dollar would help imports and hurt exports, so it would act as a counterbalance to the tax.

The key contention with this is the amount the dollar will rally. It’s expected to be boosted by 25% based off comparisons from countries who have done this in the past. It’s risky to bet an entire tax policy on the movement of a currency. Fed policy and economic reports also impact the dollar which could erode its gains. Trump would have to stop talking down the dollar to make this plan work. If he did, the dollar may rise more than 25%. The border adjusted tax increases prices for consumers causing inflation. This hurts the dollar.

Investors need to figure out the chances of the boarder adjusted tax being passed to figure out if it’s worth positioning their portfolios for its impending impact. While the boarder adjusted tax may not be perfect, it is the lynchpin for tax reforms and cuts. Therefore, even if you concluded the boarder adjusted tax would hurt consumers and thus be a negative, it is counteracted by the benefits of lower taxes.

The border adjusted tax may be met with refute by other countries who may strike back by boarder adjusting their own corporate taxes. It also may be challenged by the World Trade Organization. Therefore, Goldman Sachs says that the border adjusted tax only has a 20% chance of being passed. Goldman says a 25% corporate tax rate may be passed without the border adjusted tax if dynamic scoring is used.

The firms who will be helped the most by corporate tax cuts are the ones who pay the effective tax rate and don’t get any breaks. Smaller companies that aren’t large enough to do tax inversions or make substantial profits overseas will benefit. If import taxes aren’t offset by a rising dollar these small firms will be hurt by the border adjusted tax. Any large firm that gets to repatriate its overseas profits at a lower tax rate will see its stock increase because this cash will fund buybacks. You can look at the firms lobbying for and against the border adjusted tax to see who will benefit and who will be hurt. GE is in favor of the tax plan because it is an export driven company. As you can see from the chart below, the border adjusted tax acts as a tax on the deficit. Retailers are lobbying against the tax because it will increase prices on imported goods. They’re skeptical that the dollar’s rise will offset the 20% tax.

Conclusion

Fixing the American tax code is easier said than done. Proposing a repeal and replace to Obamacare is already expected to be pushed back until 2017. The tax cuts and reforms are going to be tough to pass. Government often has a tough time doing simple things like raising the debt ceiling, so I don’t have faith in it to come through. However, because there are mid-term elections in 2018, the GOP must show it has done something to improve the country by then. There is nothing that motivates a politician more than getting re-elected, so at the least some parts of Obamacare will be dismantled and there will likely be some tax cuts.