As I expected, the market is rallying today on a great labor report. It wasn’t much of a prediction because the market has recently gone up whether good or bad labor data is presented. It also wasn’t much of a surprise considering the great ADP report. It showed 227,000 jobs were created which easily beat the 175,000 which was expected. The unemployment rate increased from 4.7% to 4.8%, but few people believe the unemployment rate is that low anyway, so it has become irrelevant. The Fed would be raising rates if it really thought the economy was at full employment. If even the Fed doesn’t fully buy into it, it shows how phony it is. Even though the headline was strong, as with most (Bureau of Labor Statistics) BLS reports, there was mixed results below the surface.

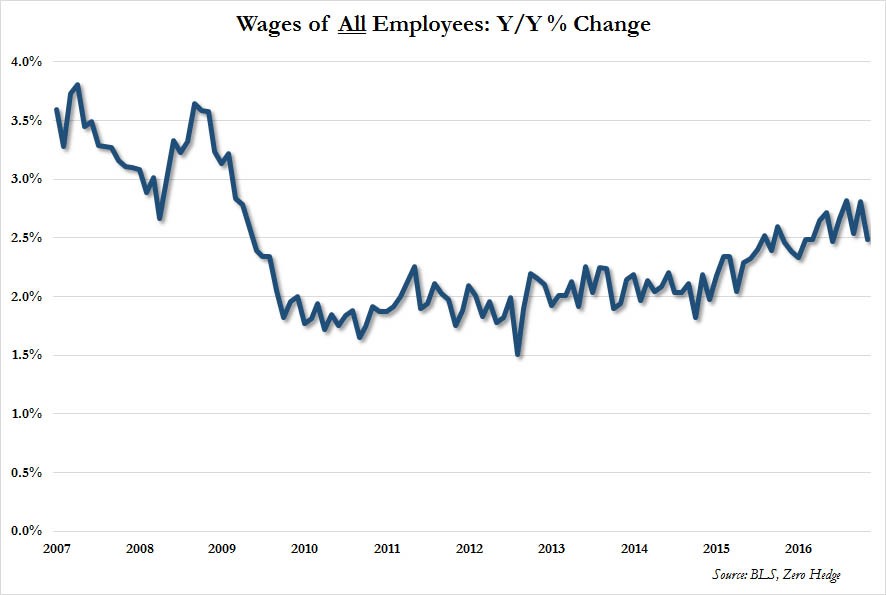

The worst part of the report was average hourly earnings growth. It was expected to show 0.3% growth, but it only came in at 0.1%. On an annualized basis, hourly earnings increased 2.5% which was slowest growth since August. January was the first month were 19 states instituted a minimum wage increase. It’s not a surprise that wages didn’t magically increase with the minimum wage. Employers probably already adjusted to the minimum wage increase after it was announced. Adjustments mean some workers were laid off and some workers got a pay increase. It creates inefficiencies in the system because low skilled workers have a tougher time getting work and employers who need to hire these workers need to replace them with machines or have the workers they can afford to hire, do more work than they may be capable of. Some of these jobs are the first rung of the ladder for new workers which makes it tougher for firms to promote from within. Support for this hypothesis that some beginning workers weren’t hired because of the minimum wage increases comes from the uptick in teenage unemployment which increased from 14.7% to 15%.

The hope for those promoting a minimum wage hike is that the benefits from the wage hikes more than offset the layoffs. Pay increases and layoffs both increase the average hourly earnings. It’s obvious why pay raises do so. With layoffs, all else being equal, wages rise on average because there are less workers on the bottom rung. Even if the employers already made their changes ahead of time, you’d expect a bigger bump in hourly earnings at some point in the past few months than what we’ve see. After all, both the positive and negative effects of the minimum wage boost the average. The fact that it didn’t increase wages implies to me that other workers may have seen a pay cut. Employers may have raised the wages of those on the bottom rung and cut those on the second rung. Employers are profit focused. They won’t accept lower margins. Instead they try to work around the law. Obviously, the fact that there is only 19 states doing this may factor into the disappointing wage growth.

Another possibility is the employers hired new workers because they were optimistic about Trump’s presidency and they started with hiring low wage workers. If you expect increased demand, the first thing you do is increase your inventory and then you hire more workers at the bottom rung. It’s why low skilled workers see the highest vacillation in their unemployment rate caused by the changes in the business cycle. Trump is promising to cut regulations which are the biggest impediment to hiring new workers. He’s also promising to repeal the regulations in Obamacare which may transform some of the part time jobs into full times ones.

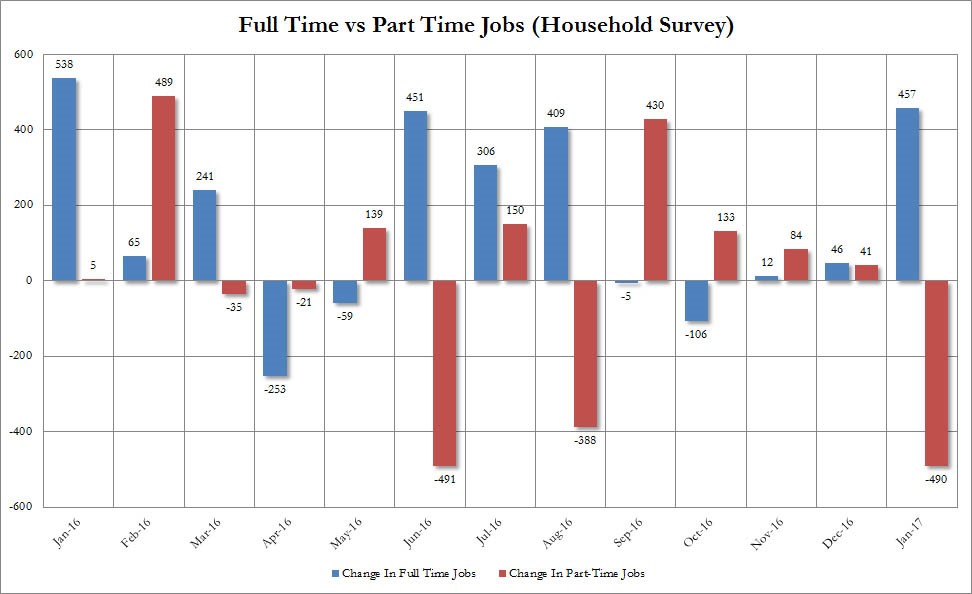

The chart below shows an increase in full time workers and a decrease in part time workers. The increase in full-time workers is the third highest in the past 12 months and the decrease in part time workers is the second most in the past year. Goldman Sachs estimates a few hundred thousand workers are involuntarily working part time because of the mandate that firms which employ 50-99 workers give their employees health care. While Obamacare did cause this increase, there is no evidence this month’s data represents a reversal because the number of people who were employed part time for economic reasons held steady at 5.8 million. However, I suspect the likely reaction to the repeal of Obamacare will be more reports like the report we had this month. Another point worth mentioning is there’s no evidence to suggest the decrease in part time workers is caused by retail layoffs because the data is seasonally adjusted. As you can see, there was barely a decrease in part time jobs last January.

To summarize, the headline employment growth data was great and the switch from hiring part time workers to hiring full time workers was a positive. The total hours worked held flat at 34.4 hours which counteracts some of the good news from the hiring of full time workers. The negative of the report was the 2.5% annualized increase in hourly earnings which is surprising to some given 19 states implemented a minimum wage increase this month.

The data is self-evident. The question outstanding is whether this makes the Fed more hawkish. Steve Liesman claimed the Fed would be watching this data closely and could use media appearances to make March a ‘live’ meeting. The media appearances will tell us whether the Fed is satisfied with the way the market is pricing in the chance of rate hikes or if it wants to raise the chances of hikes. Because this report is mixed, the Fed can draw whatever conclusion it wants. The economy may not be at full employment, but the labor market has certainly been relatively healthy in the past eight months. This hasn’t seemed to make the Fed more hawkish recently. Given the fact that the Fed just gave a dovish statement, that fiscal policy is still uncertain, and that this BLS report wasn’t surprising, I expect the Fed to stay the course on dovishness until its next meeting on March 15th.

Conclusion

The BLS report was great which spurred the Dow to have its best day of 2017 and the Nasdaq to close at a new record high. The weak earnings from Amazon, Gopro, FireEye, and Chipotle did not hurt the market. I expect the Fed to remain dovish until the March meeting. At that point it will be forced to say it is raising rates in May given how good the data has been. If the data weakens from now until May, the Fed may punt on hiking rates, yet again.