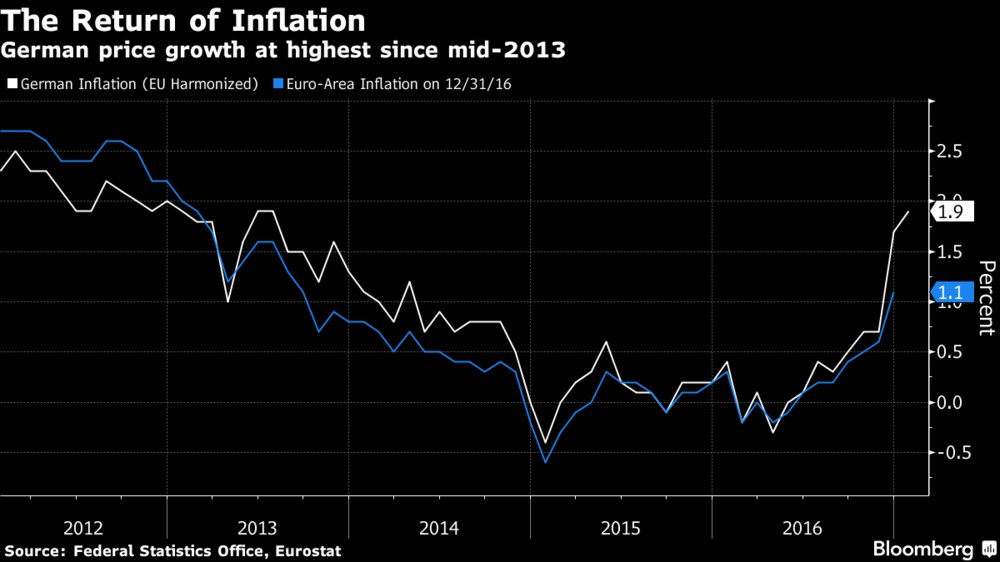

Today the German Consumer Price Index was released. The CPI showed price increases of 1.9% which was below expectations for 2.0%. Two percent is the inflation target the ECB has for the entire European Union. The 1.9% inflation in Germany is the highest rate since mid-2013, as you can see in the chart below. This was driven by a 5.8% price increase in energy costs, 2.7% price increase in goods, and a 1.2% price increase in services. The inflation rate for the whole currency bloc is expected to rise from 1.1% to 1.5% when it’s reported tomorrow; the core inflation rate is expected to stay stable at 0.9%.

The response to this data was a strengthening in the euro versus the dollar. At 8:00 AM when the data was released, the euro/usd was at 1.0625. It hit 1.707 five hours later. Even though the CPI missed expectations, the reason the euro strengthened is because it is rising. If it would have hit the 2.0% estimate, the euro would have rallied even more. It is a bit of reverse logic to think a high inflation rate is good for a currency, but this is one example of how the central banks distort markets. If the inflation rate comes in higher than expected, it means the ECB will pursue hawkish policies which is bullish for the euro. If the inflation is moderate, it means the ECB can remain dovish which is bearish for the euro. There is an alternate case of scenarios where the ECB doesn’t act as it’s expected. If the ECB doesn’t try to limit inflation and it continues to rise, it would be bearish for the euro.

The situation the EU finds itself in is rising inflation, so the only two options are either it does something to stop it or it doesn’t. Based on historical precedent, I’m expecting the ECB to respond to any inflation pressures by cutting the cord on its QE program which, as of now, is set to keep going until December 2017.

We are seeing two permutations within this decision making which complicates the matter. It’s not surprising to see ambiguous language from policy makers and analysts after a report because the ECB wants to leave all options open until a decision is made. The only reason why comments come after economic data is to calm the market. It’s not a signal of it leaning in one direction. German politicians are critical of QE, but favor a gradual normalization process.

The first permutation is in regards to whether the German inflation is actually increasing. The headline of 1.9% looks ominous, but it can be argued that energy prices are too volatile to be a good enough signal to taper QE. There’s two sides to the argument of whether to use core inflation or the total rate. The total inflation is the best metric of what the consumers are feeling. However, if energy prices can be affected by statements made by the OPEC, policy makes don’t want to have to rely on an unreliable organization and how it effects a very volatile commodity. The best way to look at this difference, in my opinion, is to focus more on the core rate, but keep an eye on the total rate. Consumers don’t notice if there’s a slight difference between the two, but if energy prices were to spike again, they would. The problem with this thinking is spiking energy prices would be the time when policy makers would especially want to avoid focusing on one commodity. As of now, this is only a potential problem. Since I think oil prices will fall in the next 6 months, I’ll avoid that question for now.

The chart below shows the historical CPI services index. It shows the inflation rate is moderate. There’s a possibility that those who are promoting the narrative that inflation isn’t really as high as the headline are in favor of maintaining stability. The story of German inflation creates political tension, so some may say “look at this rate; don’t worry!”

This political pressure is the second permutation. The current numbers don’t present any problems, but they are about to if they continue on their current trajectory. The ECB must focus on the entire EU, not just Germany. The scenario of inflation in Germany reaching 3%, while staying below 2% in the EU seems possible this year. The Germans are already angry with the bailout rules being altered to help the Italian banks and with the extension of QE until December, so this will only irk them more. This is a reversal of fortunes as the southern European countries have been forced to pass austerity to stay in the EU. Now Germany, which has benefited from being in the EU because of its cheap currency helping exports, is feeling the heat from being in the EU. It has been stated that a ‘Grexit’ or ‘Italeave’ would be the potential catalysts to end the EU, but Germany can also end it if it feels the cost benefit analysis no longer favors staying in it. The German elections are on September 24th. The inflation rate for the EU, which is released tomorrow, takes on a greater importance. If it is below expectations, it increases tensions because hawkish action is less likely even as Germany is seeing higher inflation.

The QE which I have referred to in this article is the $60 billion per month in ECB asset purchases which were originally set to end in March, but were extended until December. It was already tapered from $80 billion per month. The question is if it will taper and extend the program again or end it finally in December. Germany wants it ended earlier, but the ECB is set to decide on QE in the summer, so that clearly won’t be happening.

Unwinding the balance sheet is impossible. I expect the ECB to maintain the size of its balance sheet which will shrink as a percentage of GDP over time. The only reason why there’s a chance of an unwind in America is because Trump may appoint someone who is politically against interventionist monetary policy