There was recently an article on CNBC about why Trip Chowdhry, the managing director of equity research at Global Equities Research, believes the Snap IPO is “total junk.” He thinks the social media phase is over and users don’t want to try new apps. I think Trip was projecting his own personal viewpoints instead of doing objective work on the company. I’m not disagreeing with his standpoint that the stock is overvalued, but I think he’s too negative on the business. Given the fact that the market is already overvalued and that hot IPOs like Shake Shack defied gravity for a time, I think Snap can do the same. The reason Twitter’s stock has had poor performance is because it’s user growth stalled out. If Snapchat is able to have accelerated user growth, I can see the stock doing well.

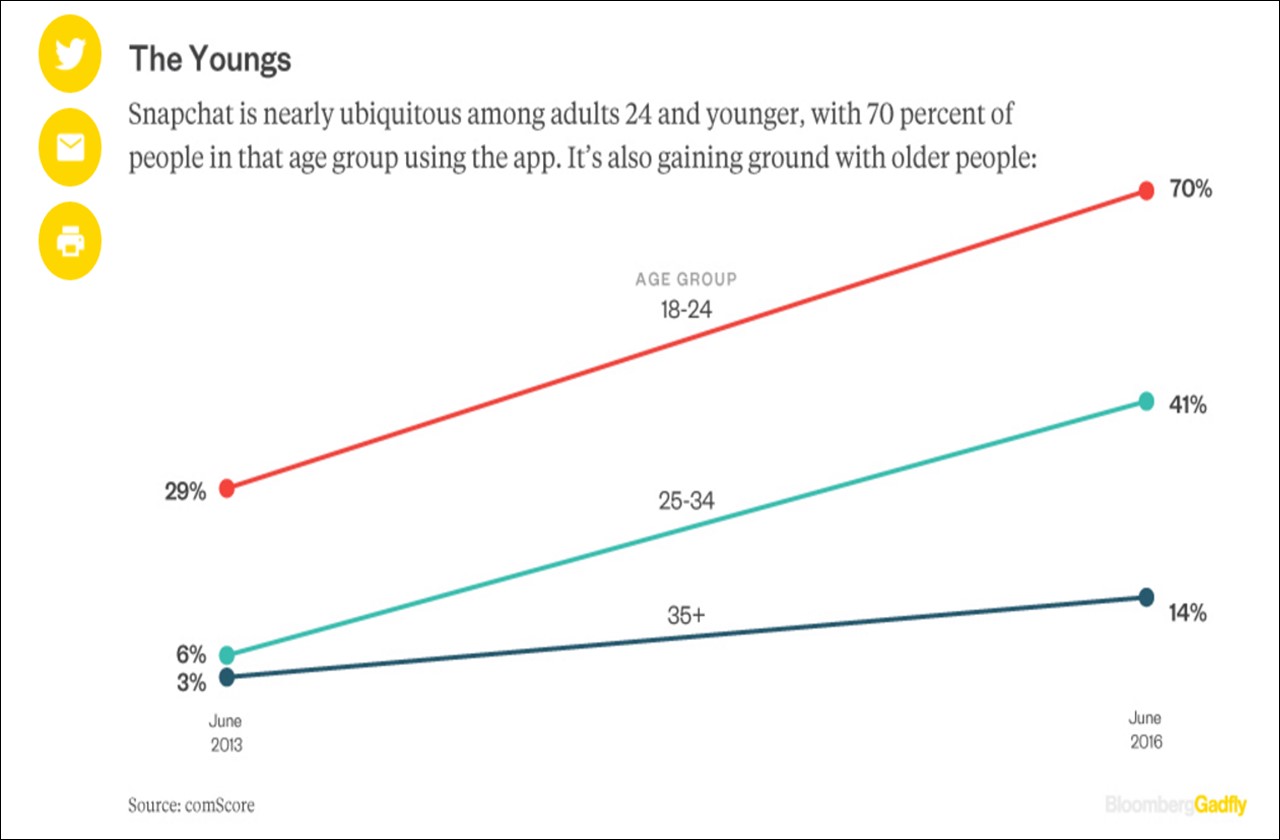

Age may be a factor in Trip’s personal issue with Snap. For people his age, Facebook and Instagram are their main social presences. He sees Twitter dying, so then concludes that no other social app can compete with Facebook. The reality is Twitter has its own separate issues it needs to deal with in terms of being user friendly. Snapchat has become the Facebook for young people. It’s not an up and coming app. It already is used instead of Facebook. The key issue for Snapchat will be expanding outside its young demographic. I think the users it already has are very sticky. Young adults would rather see their friends’ daily lives on Snapchat instead of read about it on Facebook. This is why Facebook is trying to add features Snapchat has. The chart below illustrates my point as now 70% of 18-24 year-olds use Snapchat. I can tell you from my own experience that, that metric is solid. The app will become more ubiquitous with teens in the next couple of years.

Trip compared the Snap IPO to four other failed IPOs in the past. I will explain why Snap is not like them. I could easily say Snapchat is similar to Instagram in its growth trajectory. It actually is in the same business as Snap, unlike the companies he named.

The first firm he compares Snap to is Zynga. Zynga is the social video game maker which is best known for Farmville. Zynga isn’t like Snap because Zynga relied on Facebook for its users. This meant Zynga never controlled its own destiny. Snap controls its destiny and will only fail if it stops innovating. Zynga also was relying on selling virtual items in Farmville. It’s a weak business model which loses its appeal quickly. Snap sells advertising to firms which is a stronger model. Video games all have short lifespans of popularity, but low graphics games have especially short ones. Flappy bird is one example of this. Social media apps don’t have short a lifespan. Facebook has been able to exist profitably for many years without plunging.

The second firm Trip compares Snap to is Groupon. Groupon is an app which lets people buy goods in groups for a discount. This business is going against Amazon. Amazon sellers don’t need groups to purchase goods together to offer a good price because they already have economies of scale. I used Groupon once and the product didn’t meet my expectations so I never used it again. Consumers have decided they want online shopping be like department store shopping where they simply buy the product. They don’t want to join groups in the hopes of getting a deal and they don’t like bidding on products like eBay has. Groupon failed at competing with Amazon because its core service was worse. Snapchat has the same business model as its larger competition, Facebook. Snapchat hosts video and picture content on its app and shows ads in-between content. This is the same model as all social apps (with sponsored lenses being a unique twist which can bring in additional revenue). Because Snapchat’s model isn’t different from Facebook’s, it is not comparable to Groupon.

The next company Snap was compared to was Fitbit. Fitbit sells fitness bands which track health statistics. Fitbit is a hardware product which means to generate sales it has to constantly improve its product or users won’t upgrade. Convincing users to upgrade a hardware product is tough since the first Fitbit purchased likely has many of the same features the new ones have. Snap is in an easier position. It simply has to convince users to log in every day. There is no big hurdle of asking users to upgrade. Secondly, Fitbits weren’t worn consistently. Many people wear Fitbits for a month and then stop wearing them because they get bored. The product doesn’t fulfill a powerful enough need. Anyone who witnessed this firsthand, could tell the company was toast. Snapchat users continue to share constantly and there is no drop-off after a few days or weeks. I think lenses may be a fad, but Snap can innovate such as the experimentation with using the user’s face as a character in a mini-game. Sharing your life online and messaging friends appear to be a more stable trend which won’t fade.

Finally, Trip compared Snapchat to GoPro. GoPro was built on false hype that it would be able to monetize its content. That’s not possible using simple logic. Camera firms don’t own the video recorded on their devices; the creators own it. That would be like claiming Apple could monetize the videos created with iPhones. It would be like if Asus made money from this article because I’m using its product to type it. GoPro also has limited market potential because not many people do extreme sports. Not many people can surf and record themselves at the same time using a GoPro camera. If Snap goes on its roadshow claiming it can make money from the glasses it sold which record videos, I will compare it to GoPro’s content strategy because it’s an unproven model. Even in that case, it would be better because GoPro’s content serves as marketing while Snap’s glasses are an actual product. Snap’s potential market is not limited like GoPro’s was. There is no inherent reason why older folks won’t adopt Snapchat. I’m not saying it’s a slam dunk, but if they can upload videos to Instagram, then they can upload videos to Snapchat.

Conclusion

Chowdhry is right that Snap is overvalued, but he may be wrong about the direction of the stock because his analysis of the business model is incorrect. I explained why Snap is not similar to the firms he compared it to. I think Snap stock is not a buy for fundamental investors, but if it grows its user base, its stock will act more like Facebook’s than Twitter’s.