When I refer to investors being optimistic, I am referring to multiple expansion. If earnings are rising then stocks going up is not evidence of optimism; it is an example of sound judgement. The optimism we’re seeing in this market is blind. It ignores any negative factor and only focusses on the positives. It will be interesting to see if the Fed raising rates causes a similar correction as it did last year because that seems to be the only thing the market focuses on. Not even buybacks slowing has mattered to the market.

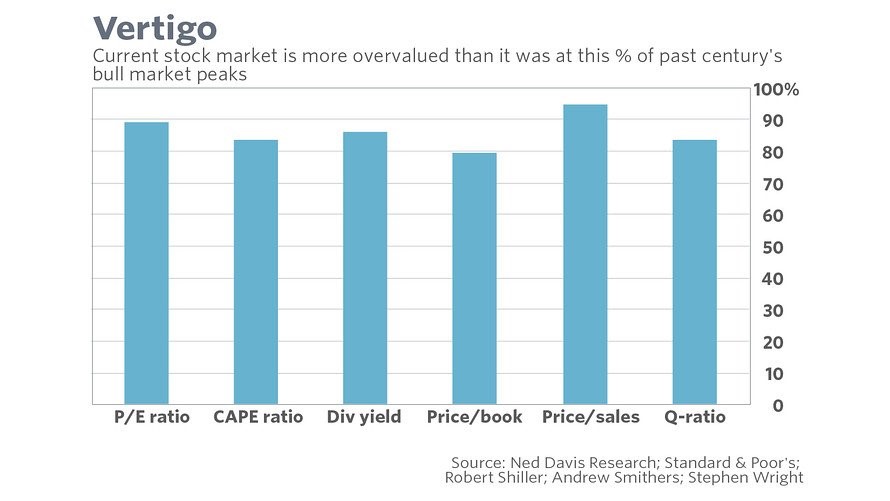

The idea that valuations will cause the market to fall has become a meme of late because the market is so detached from reality that it is more expensive than most bull markets at their peaks. The chart below looks at a few of the most common valuation metrics and compares today’s valuations to the past market peaks. As you can see, most are above the 80th percentile and the price to sales ratio is above the 90th percentile. Every time the market rallies a few percentage points like it has done in the past few weeks, these numbers rise higher and higher. Even a 1% move higher in the indices is impressive in this market because of how expensive it is. Either earnings have to improve or there will be a large correction.

The market is putting its trust in the central bankers to save the day. Every bull market extreme bubble has a theory which ends up being proven wrong. In the tech bubble speculators thought eyeballs mattered more than profits. In the financial crisis speculators believed housing prices could always go up. Now speculators have endless faith in the Fed. Even as a critic of the Fed, I have recognized the possibility that the Fed could buy stocks and levitate the market even higher. As a critic I recognize how bad the consequences of that are, but I’ve never really questioned its likelihood.

If I’m not questioning it then I bet the bulls think it is a likely scenario. This is the big lie of this cycle. Considering Congress is controlled by the GOP, the odds of the Fed buying stocks are much lower than what speculators believe. The pro-business GOP would never be in favor of the nationalization of private firms by the Fed. The limit to central bankers’ power is political. Just because central bankers are buying ETFs in Japan, doesn’t mean it could ever happen here. The only way it will be considered is if the market tanks, the GOP is blamed for the weakness, the Dems led by Bernie Sanders win the mid-term elections, and he calls for nationalization of corporations to take place. Buying stocks on this premise is a large leap of faith just like buying a house thinking its price would never fall in value was a moment of irrational exuberance.

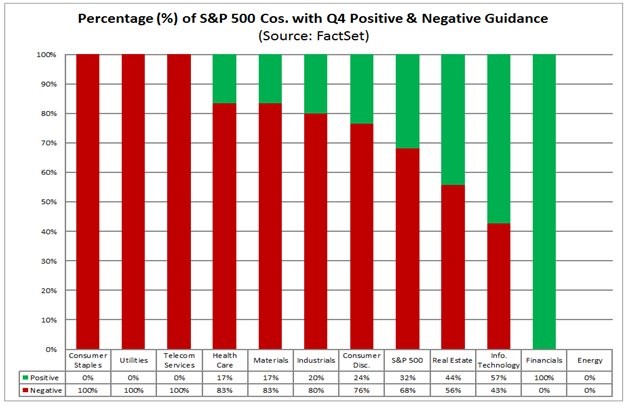

As I said, 2017 needs to be a great year for earnings growth for stocks not to fall massively. However, the guidance firms have given Wall Street for the 4th quarter aren’t great. As you can see from the chart below 68% have issued negative guidance. I’m expecting big declines in the expected growth rate of 2017 earnings to start in the next few months. If stocks rally on this news, the valuation metrics shown in the first chart will all head towards 100% making it the most expensive market ever.

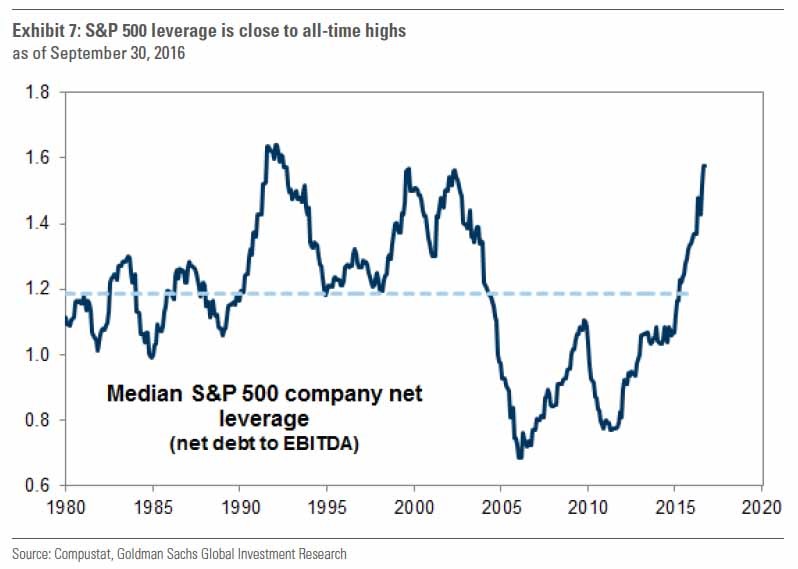

Investors aren’t the only ones levered to the Fed’s whims, betting the current situation will continue indefinitely. Corporations are also levering up their balance sheets with cheap money to buy back their stock, boost EPS, and issue big stock based compensation as executive bonuses. The chart below shows the net debt to EBITDA of the median S&P 500 company. As you can see, the leverage is near the highest point in the past 35 years. I’m expecting the leverage to get even higher as earnings fall next year due to the weak economy. Borrowing such amounts of money is short term thinking by management and ignores their fiduciary duty to work for the long term interests of shareholders.

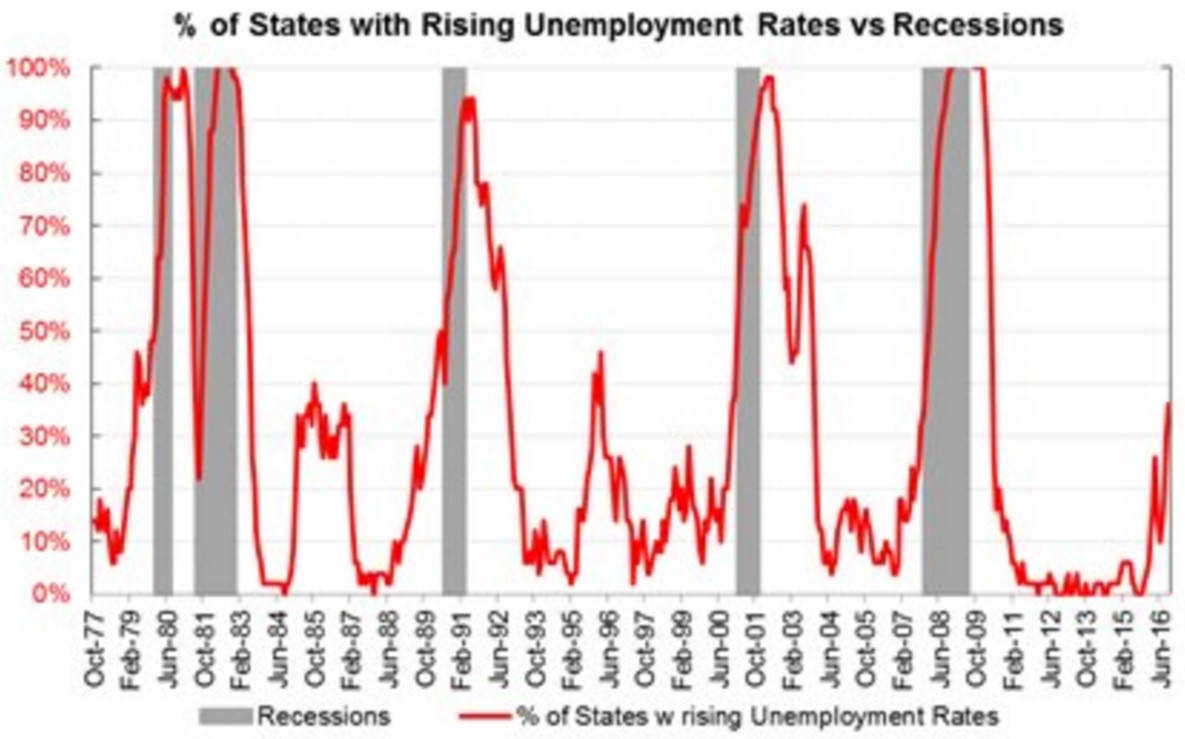

I was among the bears who though the beginning of this year was going to be the start to the end of the business cycle, but central banks were able to save the day. This cannot occur indefinitely. The chances of 2017 being the year of the big crash are heightened. One way of looking at the potential timing is the chart below. It shows the percentage of states with a rising unemployment rate. As you can see the current percentage is approaching 40%. Five of the past seven times this happened a recession followed right afterwards.

Conclusion

High leverage and high valuations have been the meme of 2016. The NASDAQ, S&P 500, Russell 2000, and the Dow have all made new highs as they ignore reality. The only index which isn’t at new highs is the NYSE. Firms are not optimistic about the future of their businesses as shown by their Q4 guidance. However, business conditions have not mattered so far as long as faith in the central banks continues. Political risk threatens to diminish central banks’ power, but the market is ignoring this risk. The chart showing state unemployment rates shows how 2017’s economy looks to be worse than 2016. It may be the year faith in central banks wanes.